Artem Voloskovets

Artem Voloskovets

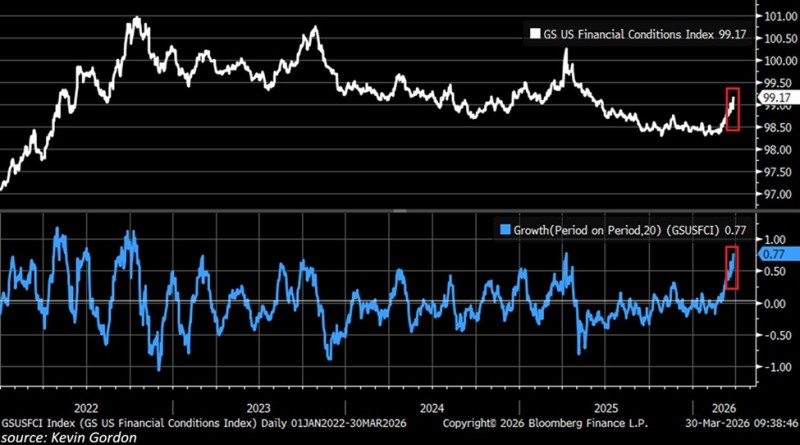

Financial conditions in the U.S. are tightening fast, and markets are starting to feel it. The GS US Financial Conditions Index has climbed to 99.17, its highest reading since June 2025, a shift that The Kobeissi Letter flagged as a meaningful turn in the macro environment, one that historically tends to precede stress across the S&P 500 and SPY.

This is not a slow drift higher. The move has been sharp, and the speed at which it developed is what makes it stand out from the broader trend.

The Acceleration Behind the SPY Pressure Is What Stands Out

Through much of 2024 and into early 2025, the index held a relatively stable range. Then came the spike. What followed was a rapid climb that has now pushed the index to levels not seen in nearly a year.

The 20-day growth rate tells the same story in sharper terms, surging to approximately +0.77. That marks the fastest tightening pace since March-April 2025 and the second-fastest since the 2022 Federal Reserve tightening cycle. That kind of acceleration does not suggest gradual adjustment. It points to a rapid shift in liquidity conditions playing out across weeks, not months.

This marks the fastest tightening pace since March-April 2025 and the second-fastest since the 2022 Fed tightening cycle.

A Clear Reversal From SPY-Friendly Conditions Earlier in 2026

Earlier this year, the index had dipped to its lowest level since May 2025. At that point, conditions were relatively accommodative, and markets reflected that. The current move is a direct reversal of that trend, not a continuation of it.

That shift aligns with what is being priced across rates markets. As covered in the analysis of Fed rate cuts dropping to 0% probability through March 2027, markets are increasingly treating prolonged tight liquidity as the base case rather than a tail risk.

Earlier in 2026, the index had declined to its lowest level since May 2025. The current move represents a clear reversal from that trend.

SPY Financial Conditions: The Structure Points to More, Not Less

The index is not spiking in isolation. It is moving higher after a period of consolidation, a pattern that tends to reflect a genuine transition into a more restrictive regime rather than a temporary blip that corrects quickly.

Historically, this kind of sustained rise in financial conditions results from multiple pressures building at once. Currency moves, rate expectations, and credit spreads rarely tighten in isolation. As detailed in the breakdown of USD movements and financial conditions, macro forces across asset classes tend to move together, and what is happening now fits that pattern.

The absence of any slowdown in the upward move reinforces the idea that conditions are still tightening, not stabilizing. For markets, that means the adjustment period is likely still ongoing.

The index itself is now pushing higher after a period of consolidation, suggesting a transition into a more restrictive phase rather than a temporary spike.

Asset-level patterns are picking up on this as well. Recent price action in names like IREN stock weakness across timeframes shows how tightening environments can coincide with weakening momentum and reduced follow-through, even in assets that had been holding up.

With the GS US Financial Conditions Index now at its tightest level in months, and accelerating at one of the fastest paces in recent years, the current setup leaves limited room for complacency. Markets appear to still be in the middle of adjusting, not at the end of it.

Artem Voloskovets

Artem Voloskovets