Victoria Bazir

Victoria Bazir

The U.S. economy may no longer simply be experiencing an AI boom. It may already be structurally dependent on one.

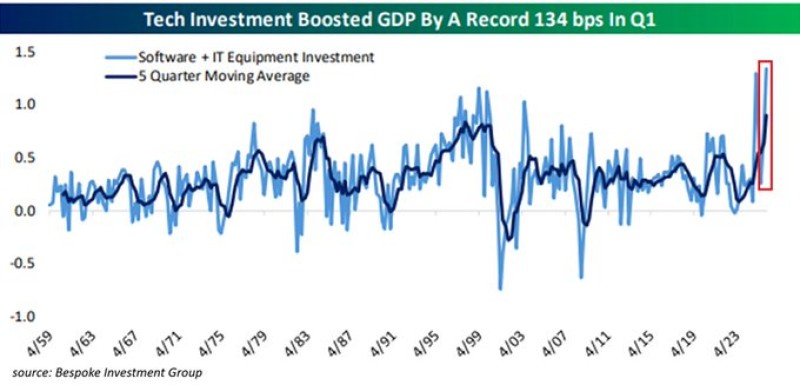

According to new investment data tied to Q1 2026 GDP growth, AI-related technology spending contributed roughly 134 basis points to total U.S. economic expansion. With headline GDP growth coming in at 2.0%, that means nearly 67% of all growth last quarter came from a single category: AI-driven tech investment.

Caption: AI-related technology investment contributed roughly 134 basis points to total U.S. GDP growth in Q1 2026, according to Bespoke Investment Group.

Without that spending surge, overall U.S. economic growth would have been close to flat. That changes the entire conversation around artificial intelligence and the economy.

For years, analysts treated AI as a future productivity story - something that might eventually reshape labor markets, enterprise software, and corporate margins over time. But the latest numbers suggest AI may already be functioning as an immediate macroeconomic engine supporting capital expenditure, infrastructure expansion, and corporate investment activity across the United States.

The implications are enormous.

If AI infrastructure spending continues accelerating, sectors tied to semiconductors, cloud computing, energy, networking, and data centers could become increasingly dominant drivers of economic growth. Companies connected to the AI supply chain may effectively operate as macroeconomic assets rather than simply technology stocks.

That may also explain why markets continue rewarding firms linked to AI infrastructure even during periods of broader economic uncertainty. But the dependence introduces a new risk.

If the U.S. economy increasingly relies on AI-related capital expenditure to maintain growth, any slowdown in AI investment cycles could have consequences far beyond the technology sector itself. Delays in hyperscaler spending, weaker enterprise AI adoption, regulatory pressure, or declining returns on AI infrastructure could begin affecting GDP growth directly rather than indirectly.

In other words, the economy may now be partially synchronized with the AI investment cycle.

That creates a paradox for policymakers.

On one hand, AI investment is helping sustain growth, productivity expectations, and corporate expansion. On the other hand, the concentration of economic momentum inside one sector increases systemic vulnerability if that cycle weakens. The chart may therefore represent more than a temporary investment spike.

It could mark the beginning of a new economic era where AI infrastructure becomes as economically important as housing, consumer spending, or industrial production once were for previous generations of growth.

The most important question now may not be whether AI changes the economy. It may be whether the economy can continue growing at the same pace without it.

Victoria Bazir

Victoria Bazir