Marina Lyubimova

Marina Lyubimova

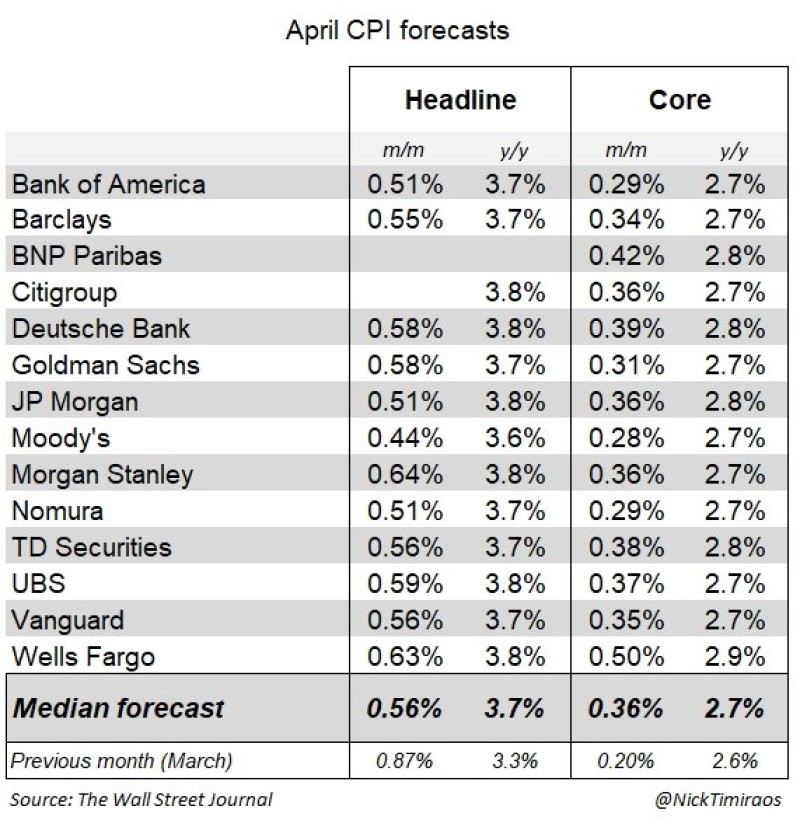

Wall Street banks are converging around a hotter-than-expected U.S. inflation print for April, with median forecasts now pointing to headline CPI rising 0.56% month-over-month and 3.7% year-over-year, according to a compilation published by The Wall Street Journal.

The data shows that nearly every major institution expects inflation pressure to remain elevated despite the Federal Reserve’s restrictive policy stance. Forecasts from firms including Bank of America, Goldman Sachs, Deutsche Bank, UBS, and Morgan Stanley all project headline CPI near 3.7–3.8% annually, while core CPI estimates mostly cluster around 2.7–2.8%.

The biggest concern for markets may be the monthly acceleration. March headline CPI came in at 0.87% m/m, and while April is expected to cool slightly, a 0.56% reading would still remain far above the pace consistent with the Fed’s long-term 2% inflation target.

Several banks are also forecasting sticky core inflation. Wells Fargo sees core CPI at 0.50% m/m, significantly above consensus, while BNP Paribas and Deutsche Bank expect annual core inflation to hold near 2.8%. That suggests underlying price pressures in services, housing, and consumer demand have not fully eased.

The forecasts arrive at a critical moment for risk assets. U.S. equities, Bitcoin, and gold have recently rallied on expectations that the Federal Reserve could begin cutting rates later this year. However, another firm inflation report could delay those expectations and strengthen the U.S. dollar while pressuring rate-sensitive sectors.

Treasury yields may become the key market signal following the CPI release. A higher-than-expected print could trigger renewed volatility across stocks and crypto markets as traders reassess the timing of potential Fed easing.

The median forecast now effectively sets a high-stakes benchmark for markets: if inflation exceeds even these elevated expectations, the narrative of imminent rate cuts could weaken rapidly.

Marina Lyubimova

Marina Lyubimova