Marina Lyubimova

Marina Lyubimova

The upgrade arrives at a time when GM is reporting record revenue, yet still trades at a fraction of the valuation assigned to several global automotive peers.

GM shares have risen more than fivefold since the 2020 selloff, when the stock briefly traded below $15. Even after that rally, Citi argues the market is still undervaluing the company. A move to $131 would push the stock beyond every major peak seen since GM returned to public markets and would represent a new high-water mark for investor expectations.

Record Revenue, Modest Valuation

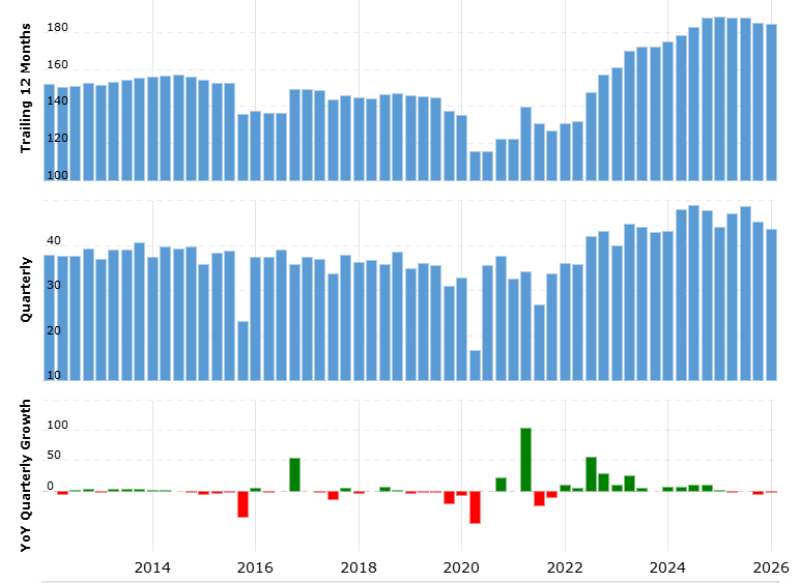

The revenue picture looks very different from the one investors saw a few years ago.

GM now generates more than $180 billion in trailing twelve-month revenue, the highest level in the company's history. Quarterly sales have remained above $40 billion for several consecutive quarters despite concerns about slowing vehicle demand and elevated borrowing costs.

The chart also highlights how quickly the company recovered after the 2020 downturn. Annual revenue has climbed steadily since then, while quarterly results have remained remarkably consistent for a business operating in a cyclical industry. That stability is one reason some analysts believe the stock's valuation does not fully reflect the company's earnings power.

Revenue Is Not the Issue. Valuation Is.

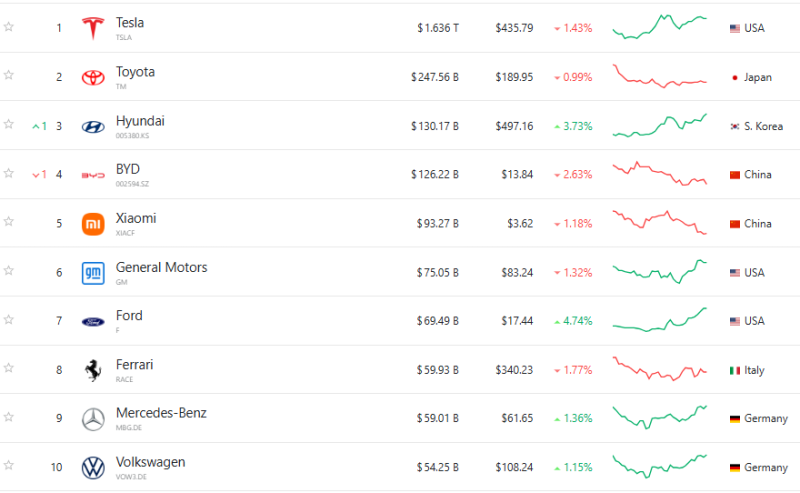

Despite generating more than $180 billion in annual sales, GM remains only the sixth-largest automaker globally by market capitalization.

Current market data values Tesla at roughly $1.6 trillion. Toyota carries a market capitalization near $248 billion, while Hyundai and BYD are both worth more than $125 billion. GM, by comparison, is valued at approximately $75 billion.

The gap between revenue and valuation continues to divide investors. Bulls argue that GM's cash flow, profitability, and shareholder-return programs justify a higher multiple. Bears remain focused on long-term competition in electric vehicles and slower industry growth. Citi's new target suggests the bank believes the valuation discount has become too large.

Citi Is More Bullish Than the Consensus

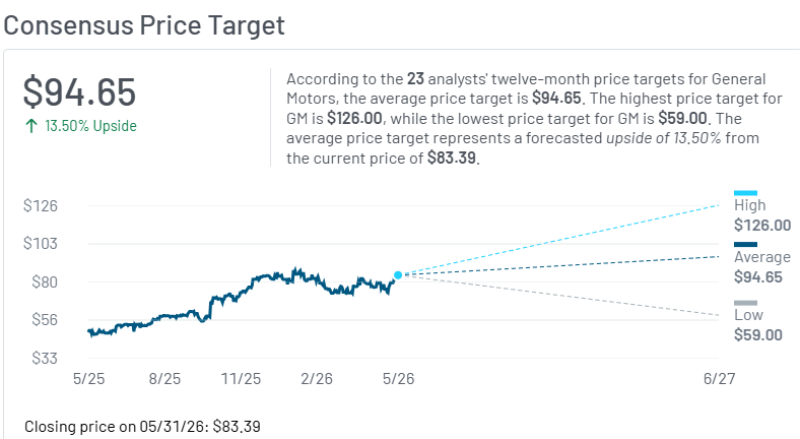

The most important number in Citi's note may not be $131 itself. It is where that target sits relative to the rest of Wall Street.

Current analyst forecasts show:

| Metric | Value |

| Current Share Price | ~$83 |

| Average Analyst Target | $94.65 |

| Highest Published Target | $126 |

| Lowest Published Target | $59 |

| Citi New Target | $131 |

Citi's forecast now stands above every major analyst target currently tracked for GM. That makes the bank one of the most optimistic voices covering the stock and suggests expectations for stronger earnings, higher free cash flow, or a broader rerating of the company's valuation.

What Would Need to Happen for GM to Reach $131?

A $131 share price would require more than stable vehicle sales. Investors would need to see continued strength in GM's North American truck and SUV business, resilient margins, and evidence that newer initiatives such as software services and electric vehicles can contribute to profitability without eroding returns from the core business.

The market would also need to become more comfortable assigning a higher valuation multiple to the company.

Citi's call is effectively a bet that investors will start valuing GM on earnings and cash flow rather than on concerns surrounding the EV transition. With revenue at record levels and the stock still trading far below many global automotive peers, the bank sees room for a significant rerating.

Marina Lyubimova

Marina Lyubimova