Marina Lyubimova

Marina Lyubimova

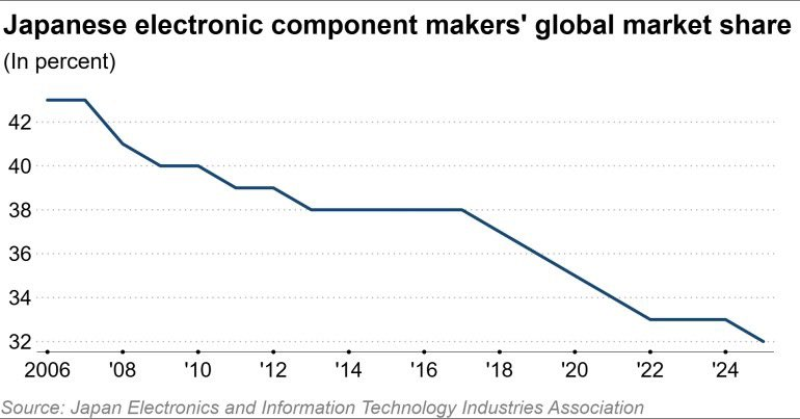

Japanese manufacturers accounted for 43% of the global electronic components market in 2006. By 2025, their share had fallen to 32%, according to data from the Japan Electronics and Information Technology Industries Association (JEITA).

The decline unfolded gradually over nearly two decades. Japan's share slipped to 38% by 2013, remained relatively stable for several years, and then entered a new phase of erosion after 2018. Since then, another six percentage points have disappeared from the country's global position.

The trend reflects a broader shift in the geography of electronics manufacturing. Taiwan strengthened its role as the center of advanced semiconductor production. South Korea expanded its presence in memory chips, displays and batteries. China moved beyond assembly work and built increasingly sophisticated domestic supply chains across multiple technology sectors.

The Market Is Growing Faster Than Japan

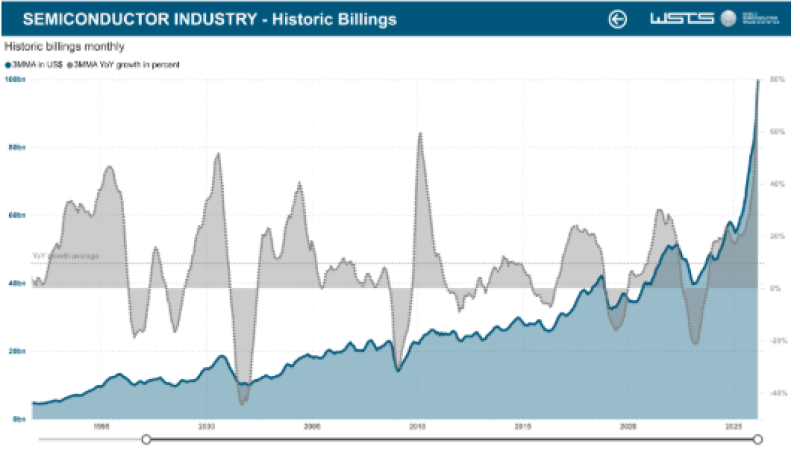

The decline in market share does not mean Japan's electronics industry is shrinking. Global semiconductor sales have expanded dramatically over the past four decades. Despite periodic downturns in 2001, 2008 and 2023, the long-term trend remains firmly upward. Demand from cloud computing, smartphones, industrial automation, electric vehicles and artificial intelligence has continued to push the industry to new records.

This distinction matters. A company or country can generate more revenue than before while still losing market share if competitors are growing faster. That is increasingly the case for Japan's electronics sector.

The industry's center of gravity has shifted toward regions that dominate semiconductor fabrication, packaging and large-scale electronics manufacturing. As new capacity has been built across Taiwan, South Korea and China, a larger share of industry growth has accumulated outside Japan.

Japan Still Controls Critical Parts of the Supply Chain

A shrinking market share does not automatically translate into weaker strategic influence. Japanese companies remain deeply embedded in global technology supply chains through products that are difficult to replace. The country maintains strong positions in semiconductor materials, precision sensors, advanced capacitors, specialty chemicals and manufacturing equipment used throughout chip production.

Many of these businesses operate in highly specialized niches where technical expertise and manufacturing know-how create substantial barriers to entry.

As a result, Japan's role has evolved from broad industry leadership toward dominance in selected high-value segments that support the wider electronics ecosystem.

Read more: Electric Ireland Raises Electricity and Gas Prices Again as Europe’s Energy Burden Persists

AI Is Accelerating the Redistribution of Growth

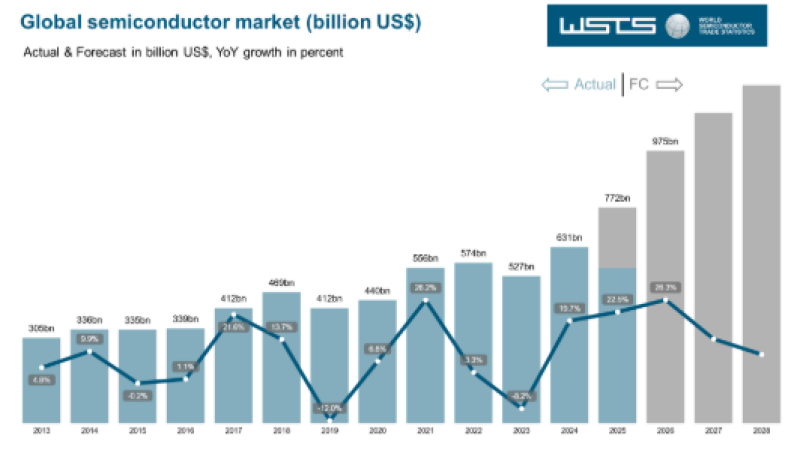

The next stage of competition may be shaped by artificial intelligence. According to forecasts from the World Semiconductor Trade Statistics organization, the global semiconductor market is expected to grow from $631 billion in 2024 to $772 billion in 2025 and approach $1 trillion by 2026. Further expansion is projected beyond that level.

Much of this growth is being driven by AI servers, data centers, advanced networking infrastructure and high-performance computing systems. These areas require enormous volumes of chips, memory, power-management systems and specialized components.

The challenge for Japan is not whether demand exists. Demand is expanding rapidly. The challenge is capturing a meaningful share of the industry's fastest-growing segments while competitors continue to scale manufacturing capacity and investment.

A Different Kind of Leadership

The JEITA data suggests Japan is no longer the dominant force it was at the beginning of the century. Yet the country's influence on the global electronics industry remains significant.

The more important question is not whether Japan's share has fallen from 43% to 32%. It is whether Japanese companies can convert their strength in critical components and materials into a larger role in the AI-driven investment cycle now reshaping the semiconductor industry.

The answer will determine whether Japan's position stabilizes in the years ahead or whether the shift toward Taiwan, South Korea and China continues.

Marina Lyubimova

Marina Lyubimova