Victoria Bazir

Victoria Bazir

Productivity data rarely attracts the same attention as retail sales reports. Yet over long periods, productivity often determines which companies expand margins and which spend years trying to protect them.

The latest figures from U.S. wholesale and retail industries show a clear separation emerging across the sector. Some businesses are generating significantly more output from each hour worked. Others are moving in the opposite direction despite employing millions of workers.

The Retail Categories Pulling Away From the Pack

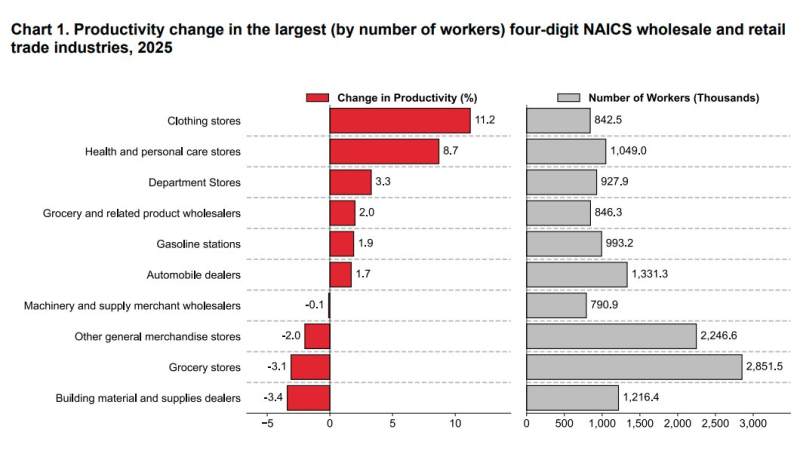

Among the largest retail industries, clothing stores posted the strongest productivity gain at 11.2%. Health and personal care stores followed with 8.7%, while department stores recorded a more modest 3.3% increase. These gains stand out because they were achieved in sectors with large employee bases and complex supply chains. Health and personal care stores alone employ more than one million workers.

Despite employing nearly 2.9 million workers, the category recorded a 3.1% decline in productivity. Building material and supplies dealers posted an even larger decline of 3.4%.

Demand is not the problem. Americans continue to spend on food, home improvement products, and everyday necessities. The challenge is that labor, transportation, and operating costs are rising faster than output. The distance between these business models is getting larger every year.

Bigger Workforces Are Not Producing Better Results

Retail used to reward scale. The latest productivity data suggests it increasingly rewards efficiency instead.

Large chains could spread costs across hundreds of locations, negotiate favorable supplier contracts, and operate with significant advantages over smaller competitors.

The latest productivity data points in a different direction. Several industries with smaller workforces are improving productivity faster than categories employing millions of workers. The number of employees matters less than the amount of output each employee generates.

That shift helps explain why productivity growth is appearing in unexpected places while some of the industry's largest employers are falling behind.

Five Retail Segments Are Leaving the Rest Behind

The strongest performers in the dataset are:

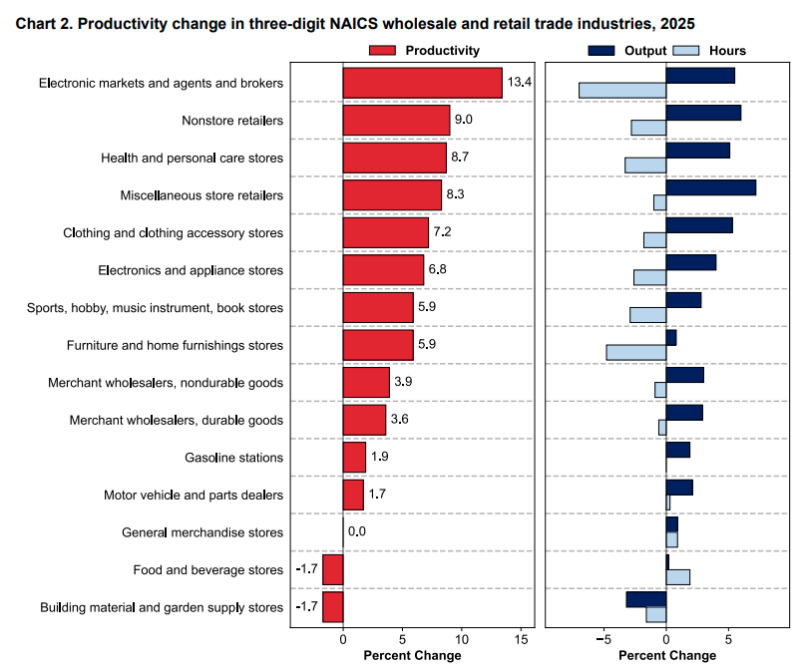

- Electronic markets, agents, and brokers: +13.4%

- Clothing stores: +11.2%

- Nonstore retailers: +9.0%

- Health and personal care stores: +8.7%

- Miscellaneous store retailers: +8.3%

Despite serving different customers, these businesses are moving in the same direction.

Output is growing faster than labor hours. Electronic marketplaces and nonstore retailers stand out in particular. Both categories benefit from business models that can process higher transaction volumes without adding employees at the same pace.

That does not automatically mean artificial intelligence is driving the gains. However, these industries have been among the most aggressive adopters of automated inventory management, digital customer acquisition, demand forecasting, and workflow optimization tools over the past several years. The productivity numbers reflect the results.

Where Productivity Is Moving Backward

The weakest readings came from industries that remain heavily dependent on physical operations.

- Grocery stores: -3.1%

- Other general merchandise stores: -2.0%

- Food and beverage stores: -1.7%

- Building material and garden supply stores: -1.7%

These businesses still rely on warehouses, transportation networks, store staff, and physical inventory movement. When labor costs rise, productivity becomes harder to improve unless output grows even faster. That creates a different set of pressures than those faced by digital-first retailers.

Why Investors Should Care

The charts are not really about retail sales. They are about which business models can grow without adding costs at the same pace. Companies that consistently increase output faster than labor expenses tend to create more room for margin expansion. Companies moving in the opposite direction often find themselves spending more simply to maintain existing performance.

The numbers point to a structural shift inside U.S. retail. Some retailers are finding ways to generate more revenue from each hour worked. Others are adding labor faster than they are adding output. The productivity gap visible today is still measured in percentages. Over time, it can become a gap in profitability, earnings growth, and market valuation.

Victoria Bazir

Victoria Bazir