Victoria Bazir

Victoria Bazir

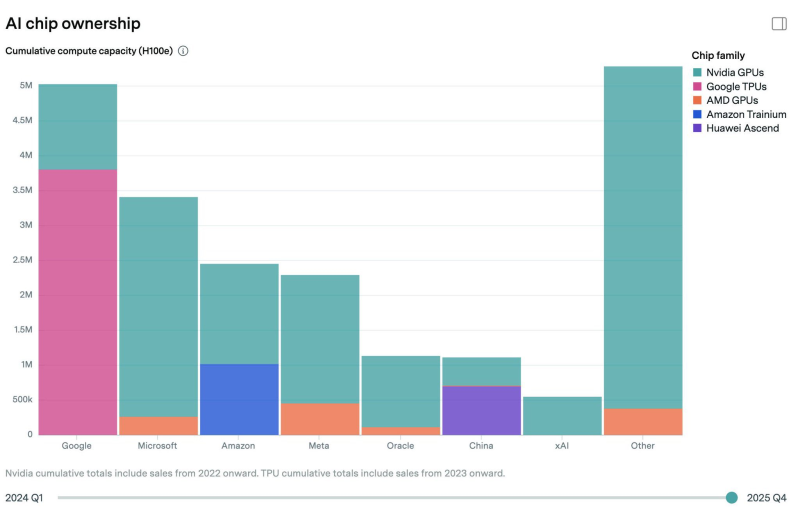

A new breakdown of global AI chip ownership suggests that the infrastructure layer behind artificial intelligence is consolidating faster than many expected, with Google and Microsoft now controlling a dominant share of large-scale AI compute capacity.

According to cumulative compute capacity estimates measured in H100-equivalent units, Google holds roughly 5 million units of AI compute capacity, slightly ahead of Microsoft.

What makes Google structurally different from most competitors is its dual-stack strategy. Unlike cloud providers that rely primarily on Nvidia hardware, Google has spent years building its own TPU ecosystem alongside Nvidia GPUs. That approach now appears to be paying off as access to advanced accelerators becomes one of the biggest bottlenecks in AI development.

Microsoft, by contrast, remains deeply tied to Nvidia infrastructure. Its estimated 3.4 million H100e units are overwhelmingly GPU-driven, reinforcing Nvidia’s position as the foundational layer of the current AI economy. Even companies aggressively investing in custom silicon have not meaningfully reduced their dependence on Nvidia hardware.

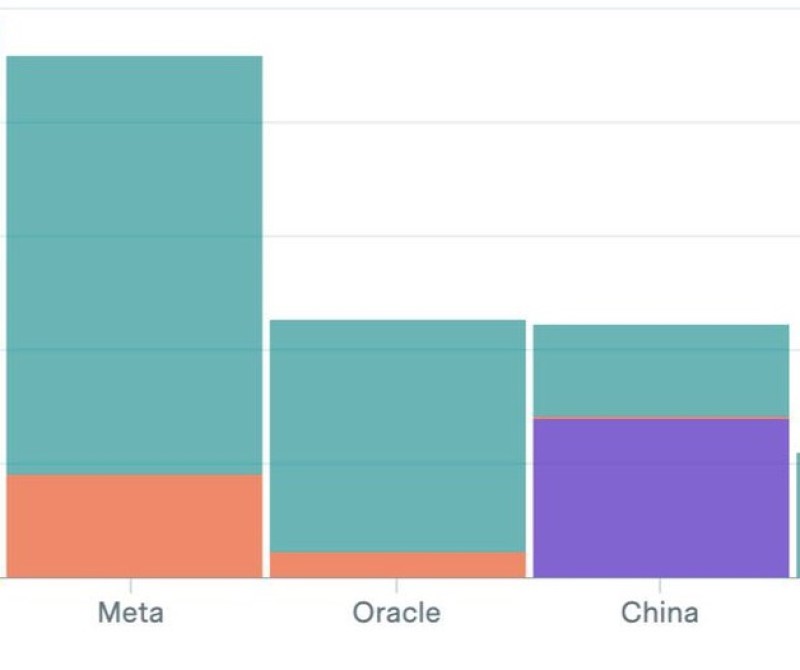

That includes Amazon, which continues expanding its Trainium program, and Meta, which is scaling infrastructure for Llama and internal AI systems while still relying heavily on Nvidia GPUs for training workloads.

China’s AI infrastructure stack increasingly appears to revolve around Huawei Ascend accelerators rather than Nvidia chips, reflecting the growing fragmentation of the global semiconductor market under export restrictions and geopolitical pressure.

The broader shift is significant because it changes what AI competition actually means.

Over the past two years, AI was often framed as a software race centered around models and applications. But frontier-scale AI is becoming increasingly constrained by ownership of compute clusters, power infrastructure and semiconductor supply chains.

Microsoft, Meta, Amazon and Google are collectively expected to spend hundreds of billions of dollars on AI-related infrastructure over the coming years, with much of that spending directed toward data centers, networking and accelerator deployment. The scale gap between large incumbents and smaller AI firms is widening rapidly.

The market is starting to resemble the early cloud computing wars of the 2010s, but with far higher concentration and geopolitical importance.

Cloud computing eventually became accessible to startups because infrastructure could be rented. Frontier AI may evolve differently. The most advanced models increasingly require compute clusters so large that only a handful of companies can realistically finance them.

Read more: The IPO Problem Nobody Wants to Model

That dynamic creates a contradiction at the center of the AI industry. AI software has become more accessible than ever, while the infrastructure needed to train state-of-the-art systems is becoming more centralized.

Nvidia remains the clearest beneficiary of that shift. The company still dominates the global AI accelerator market despite rising investments in custom chips from Google, Amazon and Huawei. At the same time, the chart highlights another emerging constraint: energy.

Several leading AI firms are already expanding into multi-gigawatt infrastructure planning as next-generation model training pushes power consumption to unprecedented levels. Compute ownership is no longer just a technology story, it is increasingly tied to electricity access, industrial policy and long-term capital deployment.

The estimates shown in the chart reflect cumulative compute capacity rather than real-time operational deployment, meaning actual active usage may differ across companies and regions. Still, the overall direction is becoming difficult to ignore. AI is no longer only a model race. It is becoming a compute ownership race.

Victoria Bazir

Victoria Bazir