Marina Lyubimova

Marina Lyubimova

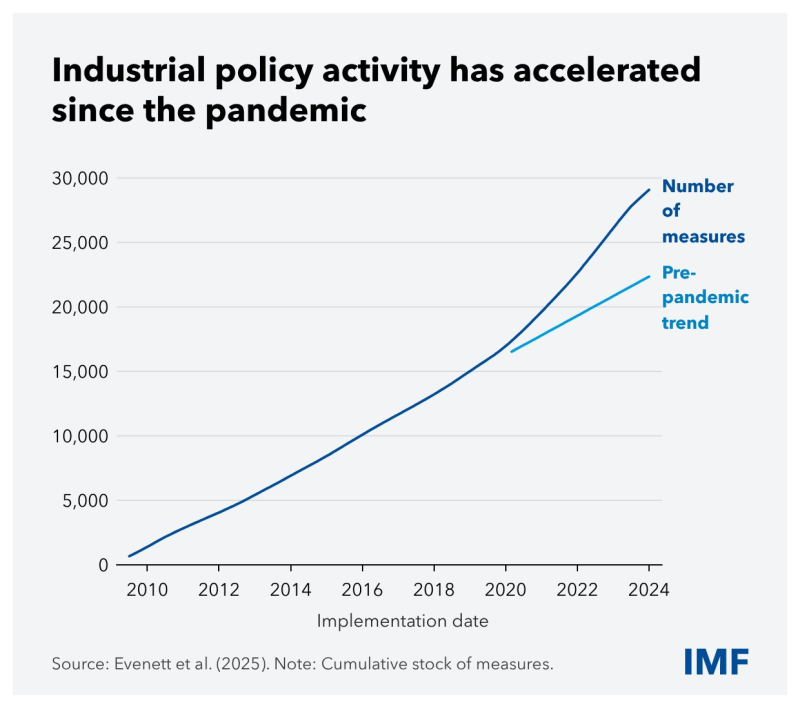

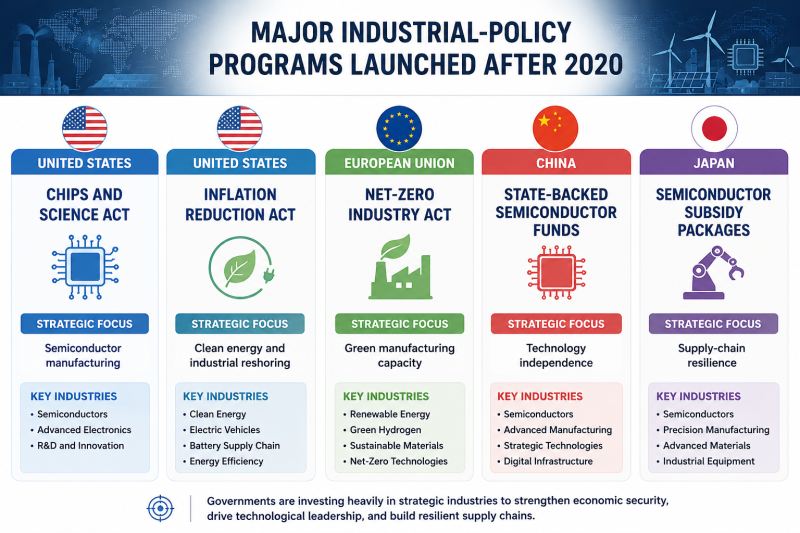

The post-pandemic economy is being reshaped by a force that barely existed in mainstream market discussions a decade ago: industrial policy. New IMF data shows governments worldwide dramatically accelerating market interventions after 2020, pushing the cumulative number of industrial-policy measures close to 30,000 by 2024 — far above the trajectory that existed before the pandemic.

The scale of the shift suggests this is no longer a temporary reaction to supply-chain chaos or inflation shocks. It increasingly looks like a structural transition away from globalization-era economics and toward state-guided competition between major powers.

Markets operated under the assumption that capital allocation would remain primarily driven by efficiency, global trade integration, and private-sector investment. The latest policy data suggests governments are now playing a far more direct role in determining where factories are built, where chips are manufactured, which industries receive financing, and which supply chains are considered strategically important.

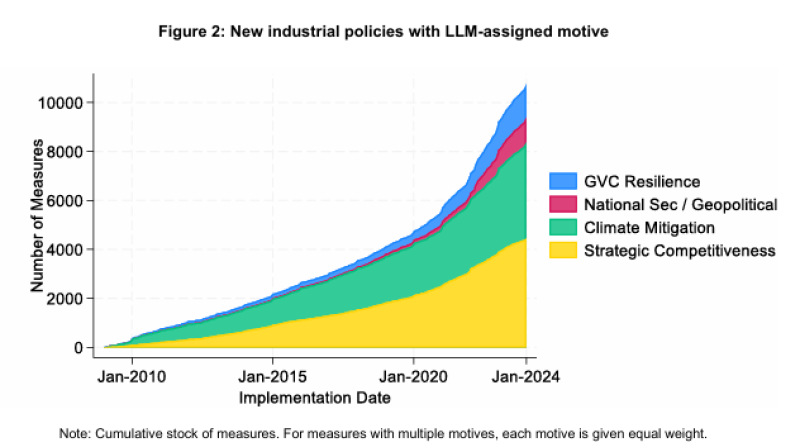

The change is especially visible in the motivations behind new industrial-policy measures.

Strategic competitiveness and climate mitigation account for the largest share of interventions globally, while geopolitical and supply-chain resilience motives have accelerated sharply since 2020.

The current wave of industrial policy is not simply about decarbonization. It is increasingly tied to national security, technological sovereignty, and geopolitical rivalry. Governments are intervening to secure semiconductor manufacturing, critical minerals, energy infrastructure, AI compute capacity, battery supply chains, and advanced industrial capabilities that are now viewed as strategic assets rather than ordinary commercial sectors.

The AI boom is reinforcing the trend. As artificial intelligence infrastructure becomes more energy-intensive and hardware-dependent, countries are racing to secure domestic access to chips, data-center capacity, power systems, and advanced manufacturing ecosystems. That has turned industrial policy into an increasingly important driver of long-term capital allocation.

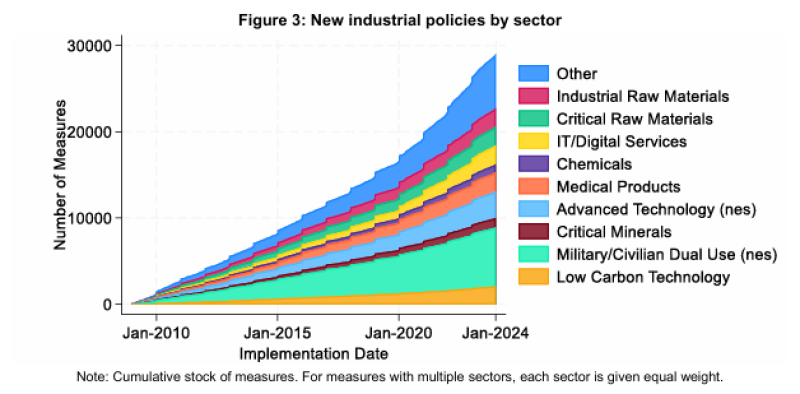

The sector breakdown of new policy measures reflects that transition clearly.

The largest concentration of measures is now tied to military and civilian dual-use technologies, advanced technology sectors, low-carbon systems, critical raw materials, and digital infrastructure. In practice, that means industrial policy is no longer confined to traditional manufacturing support. It now directly overlaps with AI infrastructure, defense technology, energy resilience, and strategic resource competition.

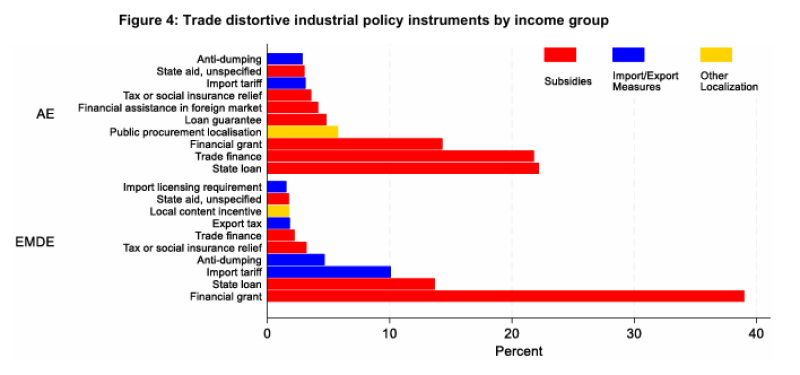

The way governments intervene is also changing.

Advanced economies are relying heavily on subsidies, trade finance, and state-backed lending programs, while emerging markets continue to use grants, tariffs, import restrictions, and localization tools more aggressively.

The result is a global economy increasingly shaped not only by interest rates and monetary policy, but by subsidy regimes, export controls, procurement rules, and geopolitical priorities. That shift is already visible in financial markets.

Semiconductors, defense contractors, grid infrastructure firms, nuclear-energy suppliers, industrial automation companies, and critical-minerals producers have all become direct beneficiaries of state-backed investment cycles. At the same time, sectors dependent on frictionless global trade are facing rising regulatory fragmentation and geopolitical risk.

The broader implication is that industrial policy is no longer operating at the margins of the global economy. It is becoming one of the main mechanisms through which governments compete for technological leadership, economic security, and geopolitical influence. Markets spent two decades pricing globalization. They are now learning how to price strategic-state capitalism.

Marina Lyubimova

Marina Lyubimova