Alex Dudov

Alex Dudov

The latest Producer Price Index report delivered another major inflation surprise - but is this just a temporary energy spike, or the beginning of a broader inflation wave across the U.S. economy?

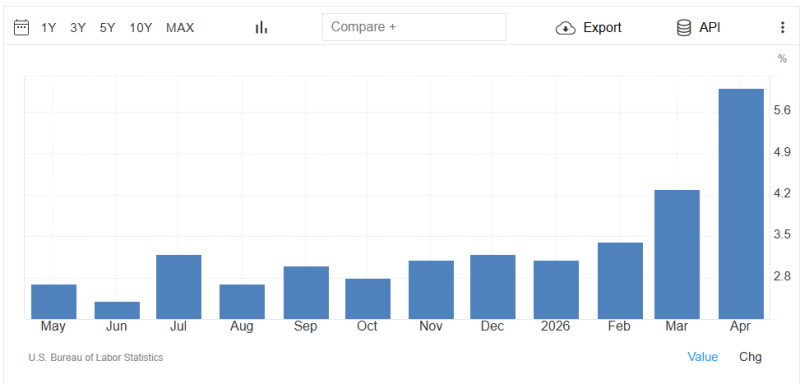

PPI inflation jumped to 6.0% year-over-year, well above the 4.9% estimate and sharply higher than the previous 4.0% reading. Core PPI, which excludes food and energy, also surged to 5.2% against expectations of 4.3%.

The chart shows inflation pressures accelerating rapidly over recent months, with April marking the strongest producer inflation print in years. For markets that were still hoping inflation was cooling, the report delivered a major shock.

Is the Iran Energy Shock Spreading Beyond Oil?

For weeks, investors hoped geopolitical tensions in the Middle East would remain largely isolated to crude oil prices. But the latest producer inflation data suggests the impact is now moving deeper into the broader economic pipeline. Higher transportation costs, manufacturing inputs, industrial materials, and logistics expenses are increasingly feeding into producer prices across multiple sectors.

That creates a much bigger problem for the Federal Reserve.

If inflation spreads beyond energy and becomes embedded in wider production chains, the Fed may be forced to keep interest rates elevated far longer than markets expected.

Did Yesterday’s CPI Report Already Warn About This?

Yes - and that is why today’s PPI release is creating additional concern.

Yesterday’s hotter-than-expected CPI report already raised fears that inflation was beginning to reaccelerate. The new PPI data reinforces that narrative from the producer side of the economy. Together, the two reports suggest inflation pressures may no longer be cooling fast enough for policymakers to justify rate cuts anytime soon.

In fact, traders are now rapidly reducing expectations for any late-2026 Federal Reserve easing cycle.

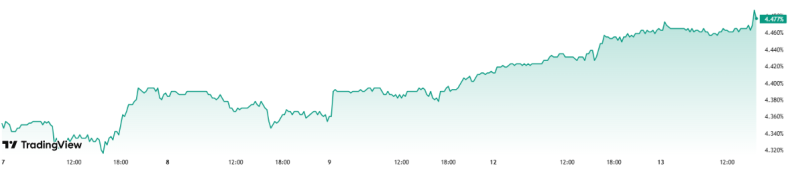

Why Are Treasury Yields Moving Higher?

Bond markets are reacting aggressively to the inflation data.

The U.S. 10-year Treasury yield continues pushing higher as investors price in a more hawkish Federal Reserve path. Rising yields signal that markets increasingly expect:

- higher-for-longer interest rates

- delayed Fed cuts

- tighter financial conditions

- persistent inflation risks

That environment creates immediate pressure for equities, especially growth and technology stocks that rely heavily on future earnings expectations.

The Nasdaq remains particularly vulnerable because long-duration assets tend to suffer most when discount rates rise rapidly. Meanwhile, the U.S. dollar is strengthening as widening rate differentials attract global capital flows into dollar-denominated assets.

Could Gold Benefit From This Environment?

Ironically, yes.

Although rising yields often pressure gold in the short term, stagflation fears can create strong safe-haven demand. Investors may increasingly look toward gold as protection against persistent inflation and slowing growth simultaneously. That “stagflation trade” is becoming more visible after back-to-back hot inflation reports.

Is the Fed Losing Control of the Inflation Narrative?

That may be the biggest question markets are beginning to ask. For months, investors believed inflation was steadily moving lower toward the Fed’s target. But consecutive hot CPI and PPI prints now challenge that assumption directly.

If geopolitical energy shocks continue spreading through the broader economy, markets may need to completely reprice expectations for:

- interest rates

- equity valuations

- Treasury yields

- dollar strength

- risk assets globally

And if that happens, today’s inflation surprise may end up looking less like a temporary spike - and more like the beginning of a second inflation wave.

Alex Dudov

Alex Dudov