Marina Lyubimova

Marina Lyubimova

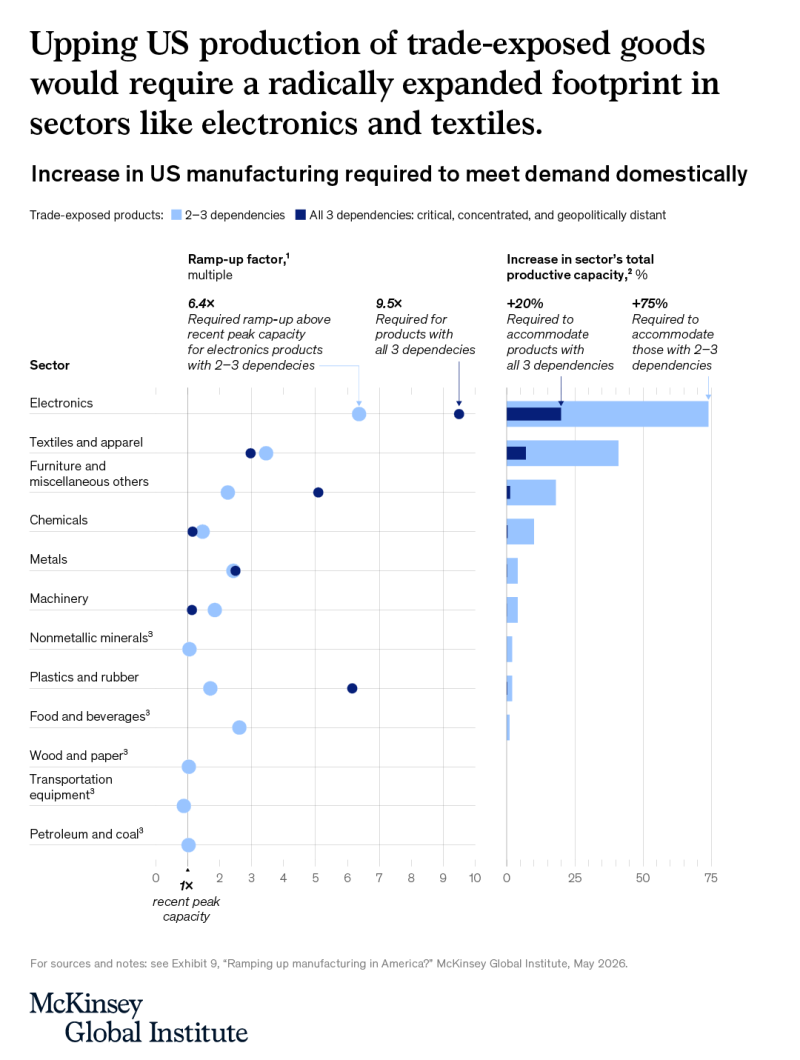

Bringing manufacturing back to the United States has become a central objective of industrial policy. A new study from McKinsey Global Institute suggests the challenge is not demand, but the scale of capacity required to replace foreign supply chains.

Electronics Is the Biggest Challenge

Electronics stands out by a wide margin. Chart to McKinsey shows domestic production capacity would need to increase by roughly 75% to replace products sourced through trade-dependent supply chains. For the most strategically sensitive categories, required output approaches 10 times recent peak capacity.

The obstacle is not simply building factories. Electronics manufacturing depends on supplier networks, semiconductor infrastructure, specialized equipment, and skilled labor that took decades to develop across Asia.

Textiles Face an Economic Reality

Textiles and apparel rank second in required expansion, with capacity needing to grow by roughly 40%.

Unlike electronics, the challenge is not technological complexity but economics. Production shifted overseas largely because of labor costs, making large-scale reshoring difficult without automation or higher consumer prices.

The Gap Between Policy and Reality

The chart highlights a mismatch between political goals and industrial capacity. Recent policies such as tariffs, export controls, and semiconductor subsidies aim to reduce reliance on foreign supply chains. Yet expanding output by several multiples requires more than incentives. It requires power infrastructure, transportation networks, supplier ecosystems, and a larger industrial workforce. The bottleneck is capacity.

Why Some Industries Face Bigger Obstacles

| Sector | Primary Constraint |

| Electronics | Semiconductor ecosystem and specialized suppliers |

| Textiles | Labor costs and global competition |

| Machinery | Skilled workforce shortages |

| Chemicals | Energy demand and permitting |

| Transportation Equipment | Complex supplier networks |

Investor Takeaway

The biggest beneficiaries of reshoring may not be manufacturers themselves. Factory construction firms, industrial automation providers, electrical equipment suppliers, logistics companies, and semiconductor equipment makers could benefit from a long-term industrial investment cycle.

The data points to a broader conclusion: rebuilding American manufacturing is less a trade issue than an infrastructure challenge. In sectors such as electronics, the gap between current capacity and policy ambitions remains substantial.

Marina Lyubimova

Marina Lyubimova