Marina Lyubimova

Marina Lyubimova

WTI climbed back toward $92 a barrel after reversing earlier losses this week. The move itself was not unusual. What stands out is how often the same pattern has appeared in recent weeks: prices fall, sellers gain momentum, and then buyers step in before the decline can go much further.

The explanation is becoming harder to ignore.

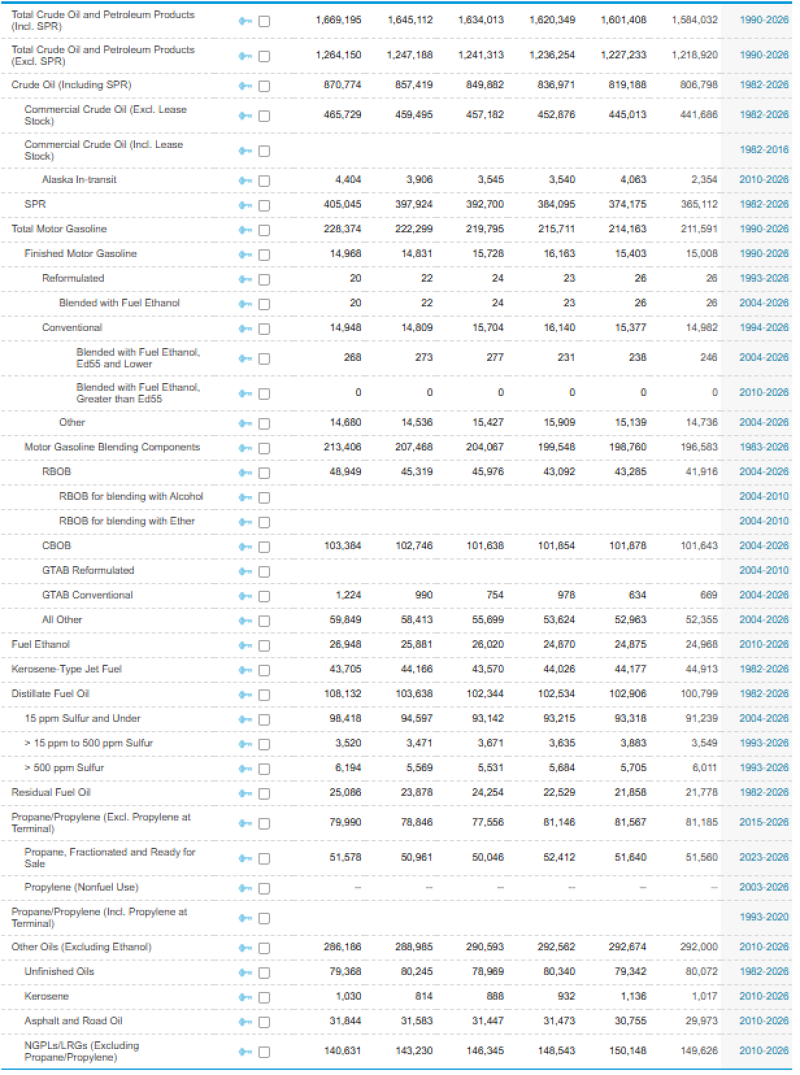

While much of the market remains focused on interest rates and growth concerns, the supply side continues to tighten. Recent U.S. petroleum data show commercial crude inventories falling from 465.7 million barrels to 441.7 million barrels. Total crude inventories, including the Strategic Petroleum Reserve, dropped from 870.8 million barrels to 806.8 million barrels.

A decline of 24 million barrels in commercial stocks and more than 64 million barrels in total inventories is difficult to dismiss as background noise. These are the barrels that help cushion the market during disruptions. As inventories shrink, the margin for error shrinks with them.

That helps explain why downside moves have struggled to gain traction. Price action tells the same story. WTI traded above $104 in May before falling toward the $88-89 range during the recent correction. The selloff looked convincing at the time. It did not last. Buyers returned below $90, lifting crude back to around $93 within days.

If traders believed a sharp slowdown was about to hit fuel demand, those rebounds would likely be weaker. Instead, each drop is being treated as a temporary dislocation rather than the start of a broader decline.

The market is effectively balancing two competing realities. On one side are concerns about growth, manufacturing activity, and the impact of high interest rates. On the other is a physical oil market that continues to draw down inventories. Neither side has fully taken control, which is why crude remains trapped between fears of weaker demand and evidence of tightening supply.

The result is a market that refuses to behave like one preparing for a major downturn. WTI is still well below its recent highs, suggesting traders are not ready to price in a supply-driven rally. At the same time, shrinking inventories are making it increasingly difficult to justify a sustained move lower.

That tension has become the defining feature of the oil market. The latest rebound toward $92 is less important than what happened before it. Commercial crude stocks have fallen by roughly 24 million barrels, total inventories have dropped by more than 64 million barrels, and every move toward $90 continues to attract buyers.

Marina Lyubimova

Marina Lyubimova