Usman Salis

Usman Salis

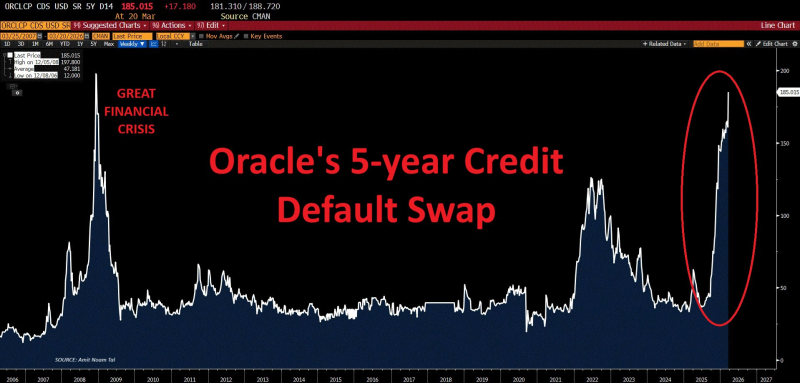

Oracle's credit risk has moved into uncharted territory, with its 5-year credit default swaps reaching the highest level on record and moving above the peak seen during the 2008 financial crisis. As Global Markets Investor highlighted, the cost of insuring Oracle's debt has risen sharply, reflecting intensified positioning in credit markets.

The Break Above Oracle's Historic 2008 CDS Ceiling

The chart shows Oracle's CDS history stretching back to 2006, with the previous major high formed during the Great Financial Crisis reaching roughly 197.8 basis points. The latest reading sits near 198.18 basis points - putting the current move marginally but decisively above the prior peak.

The latest surge pushes Oracle's 5-year CDS into the 185-200 basis point range, marking a clear breakout above every major historical stress zone on the chart. This is not a routine fluctuation - it is a decisive move into a new range after years of trading far below crisis-era levels.

Once a CDS series breaks above its crisis-era high, historical comparisons become less useful - the market is in fresh price-discovery territory with no obvious ceiling above.

Oracle's CDS Hits 16-Year High at 1.28% as $105B Debt Sparks Market Concern captured the earlier stage of this repricing, when the move was still being framed as a multi-year high rather than an all-time record.

A Vertical Oracle CDS Move Since Mid-2025

One of the most striking features of the chart is the pace of the rise. Oracle's CDS remained relatively subdued for much of the post-2009 period, then saw temporary spikes in 2022 and 2023 before easing. That changed dramatically in 2025, when spreads began climbing almost vertically into early 2026.

The cost of insuring Oracle's default risk has quadrupled since mid-2025 - and the chart supports that direction. The move from a relatively low base to nearly 200 basis points in a short period signals aggressive repricing rather than a gradual adjustment.

ORCL CDS Spread Doubles to 120+ Basis Points as AI-Driven Credit Risk Surges documented the earlier doubling phase, showing how the acceleration in spread widening has been compounding rather than stabilizing.

Oracle Becomes the Market's AI Credit Risk Proxy

The CDS move is not framed solely as a company-specific event. It reflects how investors are using Oracle's debt and derivatives liquidity to express a broader view on leverage tied to the AI buildout. Oracle's large bond footprint in the Bloomberg US high-grade corporate bond index and its liquid investment-grade CDS market help explain why flows are concentrating in this name.

In effect, Oracle is functioning as a high-profile pressure point for credit investors who want exposure to AI-related debt risk without leaving the investment-grade universe.

Oracle is no longer just another large-cap technology credit - in the CDS market, it has become a focal point for how investors are pricing the risks of debt-heavy AI expansion.

Oracle's Credit Insurance Hits $105B as Protection Costs Triple Since June puts a dollar figure on the scale of that protection demand, showing just how much capital is now being deployed to hedge against Oracle's credit risk specifically.

With the chart now above the 2008 benchmark, the signal is less about a single spike and more about how far credit sentiment has shifted - and what that shift says about how markets are pricing the broader risks of debt-driven AI expansion.

Usman Salis

Usman Salis