Marina Lyubimova

Marina Lyubimova

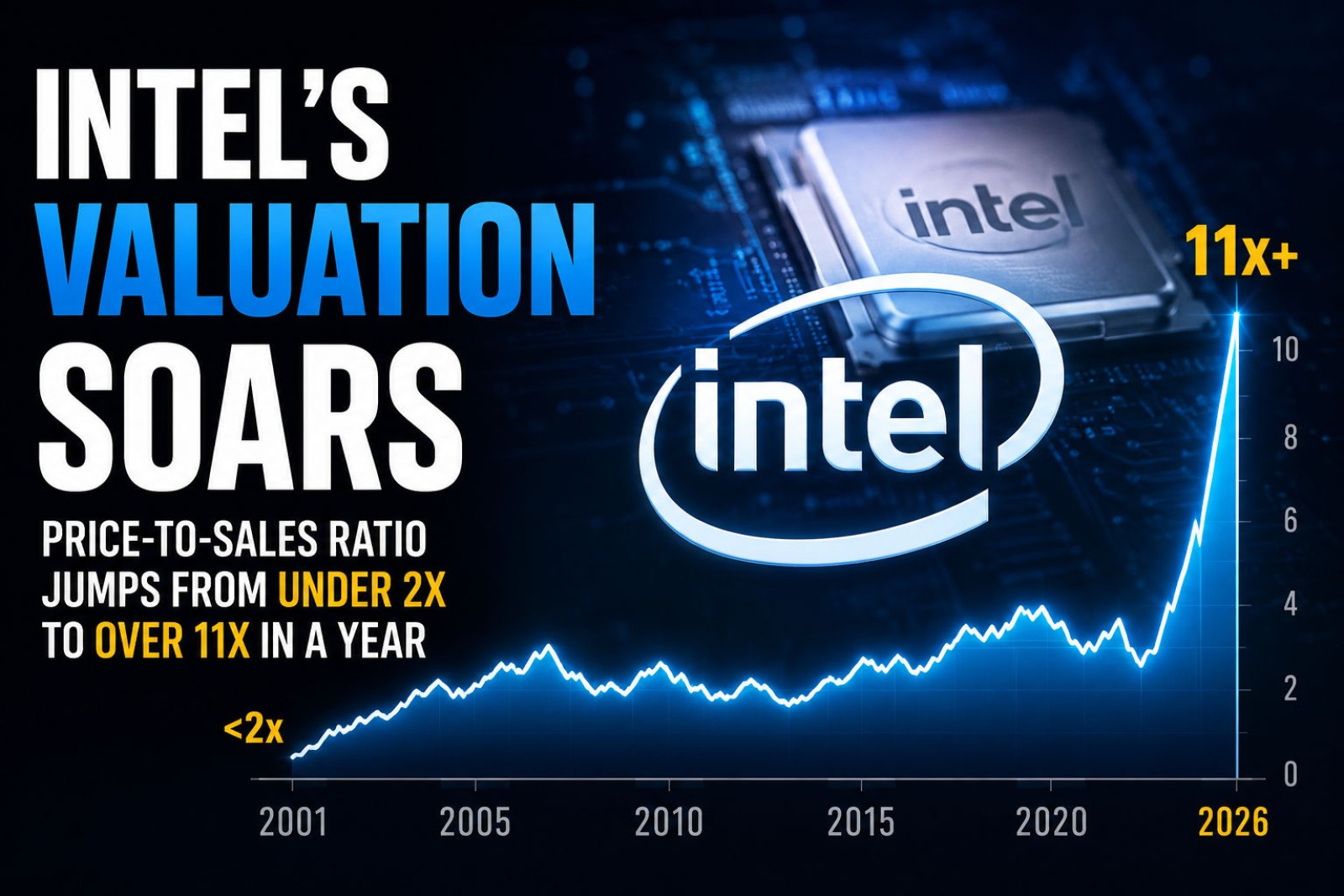

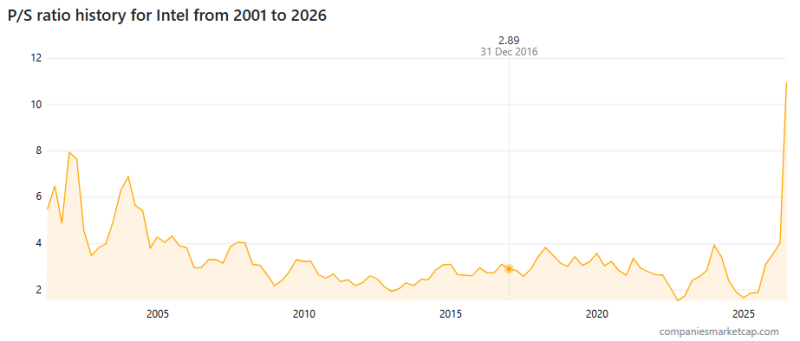

According to historical market data, the company's price-to-sales (P/S) ratio has climbed from below 2x in early 2025 to more than 11x in mid-2026. The move places Intel at its highest sales multiple in at least 25 years.

The significance of the shift becomes clearer when viewed in historical context. For most of the past two decades, Intel traded within a relatively stable valuation range despite multiple semiconductor cycles, product launches, and changes in industry leadership.

Intel Breaks Out of Its Historical Valuation Range

For much of the 2000s, 2010s, and early 2020s, Intel's P/S ratio generally fluctuated between 2x and 4x. Even during periods of strong demand for PCs, servers, and data-center hardware, the company rarely sustained a significantly higher valuation.

That pattern changed dramatically over the past year.

The chart shows a valuation profile that remained relatively consistent for decades before breaking sharply higher in 2026. At more than 11x sales, Intel is trading at a multiple well above previous peaks and far outside its historical range.

The move is particularly notable because it occurred without a comparable increase in revenue.

Market Value Has Grown Much Faster Than Sales

While Intel's business has stabilized and sentiment around the company has improved, the expansion in valuation has been driven primarily by the stock price. Over the past year, Intel shares climbed from roughly $25–30 to more than $120, pushing the company's market capitalization sharply higher.

The stock's rise has significantly outpaced changes in revenue, resulting in a much higher valuation being assigned to each dollar of sales.

Historically, such moves tend to occur when markets begin pricing in a different long-term outlook rather than current operating results.

Three Factors Behind the Re-Rating

Several developments have contributed to the change in perception.

1. AI Infrastructure

Artificial intelligence remains the dominant theme across the semiconductor industry. Although Nvidia continues to lead the market, investors increasingly view Intel as a potential participant in the broader AI infrastructure buildout through data-center products, advanced packaging technologies, and future accelerator offerings.

2. Intel Foundry

The company's manufacturing strategy has become another important part of the story. Intel Foundry aims to position the company as a contract chip manufacturer serving external customers, creating a business model that extends beyond Intel's traditional processor franchise.

If successful, the initiative could open new revenue streams and strengthen Intel's role within the global semiconductor supply chain.

3. Advanced Manufacturing

Progress on Intel's manufacturing roadmap has also improved sentiment. Recent developments surrounding the company's 18A process technology have reinforced expectations that Intel could regain competitiveness in advanced chip production after several years of execution challenges.

What a P/S Ratio Above 11x Usually Means

A valuation above 10x sales is typically associated with companies expected to deliver substantial future growth.

For Intel, the current multiple suggests that the market is placing greater emphasis on future opportunities than on present-day financial performance. Whether those expectations prove accurate will depend on the company's ability to expand its manufacturing business, execute its technology roadmap, and capture a meaningful share of AI-related demand.

For now, the valuation itself provides a useful signal: the market is assigning Intel a role that differs markedly from the one it held for most of the past two decades.

A Different Intel Than the Market Knew Before

Intel's P/S ratio has risen from below 2x to more than 11x within roughly a year, making it one of the most significant valuation expansions among large semiconductor companies in recent memory.

The historical charts suggest that investors are no longer viewing Intel solely through the lens of its legacy PC and server businesses. Instead, the company is increasingly being evaluated against opportunities tied to AI infrastructure, semiconductor manufacturing, and long-term strategic positioning.

Whether that shift ultimately proves justified remains to be seen. The re-rating itself, however, is already one of the most striking developments in the semiconductor sector this year.

Marina Lyubimova

Marina Lyubimova