Artem Voloskovets

Artem Voloskovets

Deutsche Bank is questioning that assumption. The bank recently lowered its gold outlook and outlined a downside scenario in which bullion falls to $3,800 per ounce if markets begin pricing three to four additional Fed rate hikes. Its base-case forecast remains bullish, with gold reaching $4,800 per ounce by the fourth quarter. The gap between those two outcomes says less about gold demand and more about the path of U.S. monetary policy.

For a market built on expectations of lower rates, the risk is not what the Fed has done. It is what investors may have gotten wrong.

Gold's Rally Is Built on One Assumption

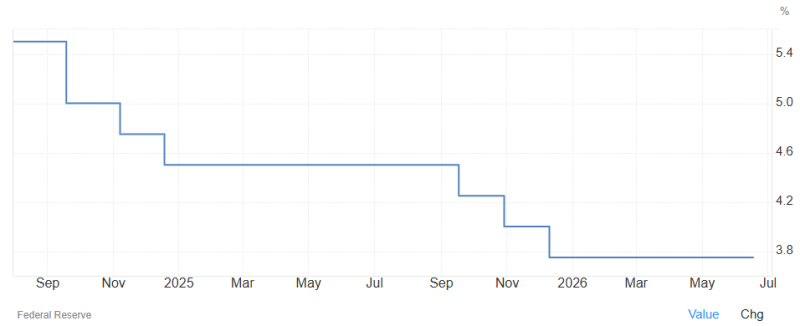

Interest-rate markets continue to anticipate a steady decline in borrowing costs over the next two years. Current pricing implies the Fed funds rate falls from roughly 5.5% in 2024 to around 3.8% by mid-2026.

Markets continue to price nearly 170 basis points of easing through 2026 despite persistent inflation risks. That expectation has become one of the strongest forces behind the gold rally.

Unlike bonds, gold generates no income. When investors expect yields to decline, the opportunity cost of holding bullion falls. As rate-cut expectations intensified, capital flowed into assets positioned to benefit from easier financial conditions, including precious metals.

The move worked because inflation gradually cooled and the Fed stepped away from additional tightening. The question now is whether that trend continues. If inflation stalls or reaccelerates, markets may need to reassess how much easing is actually ahead.

Deutsche Bank Sees a Different Rate Path

Most forecasts for gold focus on supply, jewelry demand or central-bank purchases. Deutsche Bank is focused on something else: expectations. Its latest outlook presents two distinct paths.

The first assumes the Fed remains broadly aligned with market expectations. Under that scenario, gold continues higher and reaches approximately $4,800 per ounce.

The second assumes inflation remains persistent enough to force investors to rethink the outlook for rates. If markets begin pricing three to four additional hikes, Deutsche Bank sees gold falling toward $3,800.

Deutsche Bank's outlook highlights the gap between its $4,800 base case and a $3,800 downside scenario driven by renewed Fed tightening. The forecast is less a call on gold than a challenge to one of the market's strongest convictions: that the next meaningful move from the Federal Reserve will be lower, not higher.

Investment Demand Is Losing Momentum

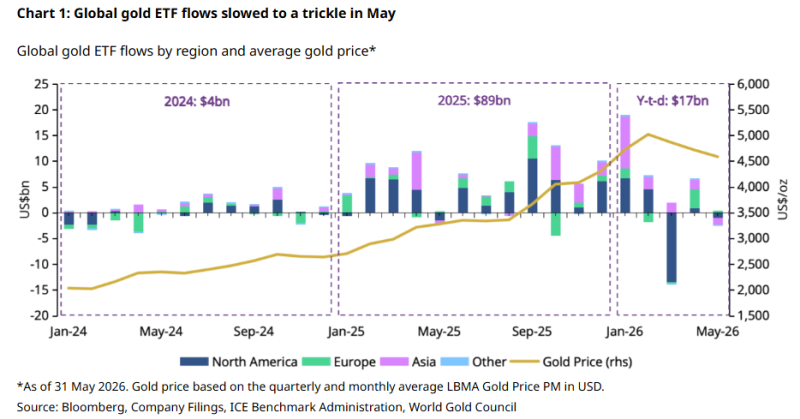

The first signs of that vulnerability are already visible in investment flows. Gold ETFs attracted enormous amounts of capital during 2025 as investors positioned for lower rates and continued uncertainty. According to World Gold Council data, net inflows reached roughly $89 billion during the year.

The pace slowed sharply in 2026. Year-to-date inflows are closer to $17 billion, even though gold remains near record highs.

Gold prices remain elevated, but ETF inflows have slowed dramatically, suggesting investor enthusiasm is fading. Prices are holding up. Investor participation is not.

That divergence does not guarantee a reversal, but it suggests fewer buyers are willing to add exposure at current levels. The rally is no longer being reinforced by the same wave of ETF demand that helped drive it higher in 2025.

One Buyer Matters More Than Ever

At the same time, physical demand is becoming less supportive. High prices have reduced buying activity in China and India, the two largest consumer markets for gold. Jewelry demand has softened, and retail buyers are showing greater sensitivity to price levels.

That leaves central banks carrying more of the burden. Official-sector purchases have become one of the market's most reliable sources of demand over the past several years as reserve managers diversified away from traditional reserve assets. Those purchases have helped offset weaker demand elsewhere and provided an important floor under prices.

The result is a market increasingly supported by a narrower set of buyers. As long as central banks remain active, that may not be a problem. But the balance becomes more fragile when ETF demand slows and consumer demand weakens at the same time.

The Scenario Markets Aren't Pricing

The Deutsche Bank downside case requires more than one thing to go wrong. Economic growth would need to remain resilient. Inflation would need to stop moving lower. Investors would need to abandon expectations for rate cuts and begin pricing a more restrictive policy path.

None of those outcomes appears to be the consensus view today. That is precisely why they matter. A repricing of Fed expectations would push Treasury yields higher, strengthen the dollar and reduce the appeal of non-yielding assets. Gold would not be reacting to weaker fundamentals. It would be reacting to a different interest-rate environment.

Where the Risk Sits

Gold remains supported by central-bank buying, geopolitical uncertainty and expectations of eventual monetary easing. Those forces have not disappeared. What has changed is the margin for error. The market has largely accepted the idea that the next chapter of Fed policy involves lower rates. Deutsche Bank is asking what happens if that assumption proves premature. For gold, the answer may matter more than ETF flows, jewelry demand or even central-bank purchases. The biggest risk is not in the metal itself. It is in the expectations that helped drive the rally in the first place.

Artem Voloskovets

Artem Voloskovets