Marina Lyubimova

Marina Lyubimova

In reality, the approval highlights a broader shift taking place across global finance. Governments and financial regulators are increasingly focused on modernizing cross-border payment infrastructure. Dubai's decision suggests that blockchain-based settlement networks are becoming part of that conversation.

The development matters less because of XRP itself and more because of the problem Ripple is trying to solve.

Cross-Border Payments Still Have a Cost Problem

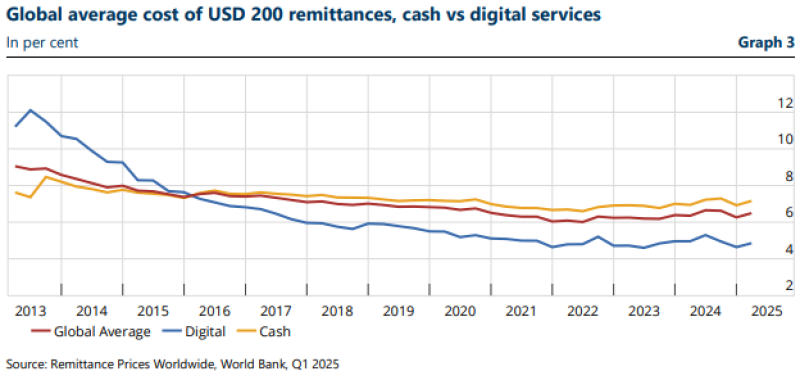

International transfers have become cheaper over the last decade, but progress has been gradual.

World Bank data shows that the average cost of sending a $200 remittance has fallen from more than 8% in 2013 to roughly 6% in 2025. Digital providers achieved the largest gains. Their average fee dropped from approximately 11% to below 5% during the same period. The decline is significant, but the market remains far from frictionless.

For households, these costs reduce the amount of money received abroad. For businesses, international payments often involve multiple intermediaries, settlement delays, foreign-exchange costs, and trapped liquidity. Most of the infrastructure supporting global payments was built decades ago. While interfaces have improved, the underlying architecture has changed far more slowly. This gap creates an opportunity for alternative payment networks.

Why DIFC Matters

Dubai's role in global finance extends beyond digital assets. The emirate sits between major trade and capital corridors linking Europe, Asia, Africa, and the Middle East. Companies operating across these regions require efficient settlement, treasury management, and access to international liquidity.

For Dubai, improving financial infrastructure is an economic objective rather than a technology experiment. That strategy explains why the UAE has introduced regulatory frameworks covering digital assets, tokenization, stablecoins, and blockchain-based financial services.

Ripple's authorization should be viewed in this context. The company is not entering a speculative retail market. It is gaining access to a regulated financial ecosystem designed around cross-border activity.

What The Approval Signals

The immediate impact of the license is straightforward: Ripple can offer regulated blockchain-powered payment services within DIFC. The longer-term implication is more important.

Financial regulators historically move cautiously when introducing new infrastructure. Before institutions adopt a new system at scale, regulators typically establish legal frameworks, licensing requirements, and supervisory standards. Dubai's approval indicates that blockchain payment networks are increasingly being evaluated as financial infrastructure rather than purely crypto products.

That distinction changes the adoption pathway. Instead of competing for retail users, providers such as Ripple can compete for payment companies, banks, treasury operations, and institutional clients.

Beyond XRP

The market often evaluates Ripple developments through the lens of XRP. The larger opportunity sits elsewhere.

Cross-border payments represent a multi-trillion-dollar industry where efficiency gains can translate into meaningful economic value. Faster settlement, lower transaction costs, and improved liquidity management are priorities for financial institutions regardless of their view on digital assets.

As a result, the key question is not whether a regulatory approval influences short-term token performance. The more relevant question is whether regulated financial institutions become comfortable using blockchain-based infrastructure for real economic activity. That process tends to unfold slowly, but once adoption begins, it is usually driven by operational benefits rather than market narratives.

Competition Is Shifting Toward Infrastructure

Several financial centers are pursuing similar strategies. Singapore continues expanding tokenization initiatives. Hong Kong is building frameworks for digital asset services. Abu Dhabi is investing heavily in financial technology infrastructure. The competition is increasingly focused on attracting payment networks, settlement providers, tokenization platforms, and digital asset infrastructure rather than simply hosting crypto exchanges.

Dubai's approval of Ripple fits into this broader trend. The development does not transform global payments overnight. It does, however, provide another indication that regulators are beginning to integrate blockchain-based infrastructure into the financial system rather than treating it as a parallel market.

Conclusion

Ripple's authorization in DIFC is less important as a crypto headline than as a signal of where financial infrastructure is evolving. Cross-border payments remain expensive despite years of digitization. Governments, regulators, and financial institutions continue searching for more efficient ways to move money across jurisdictions.

Dubai's decision suggests that blockchain-based payment networks are increasingly being considered part of that solution. For Ripple, the approval is not simply market access. It is a foothold inside one of the regions where the future architecture of global payments is being built.

Marina Lyubimova

Marina Lyubimova