Victoria Bazir

Victoria Bazir

The survey indicates that institutional adoption is entering a more mature phase. Portfolio exposure continues to expand, but investment decisions are increasingly shaped by custody, regulation, operational controls, and product structure instead of market volatility alone.

Institutional participation is no longer the question

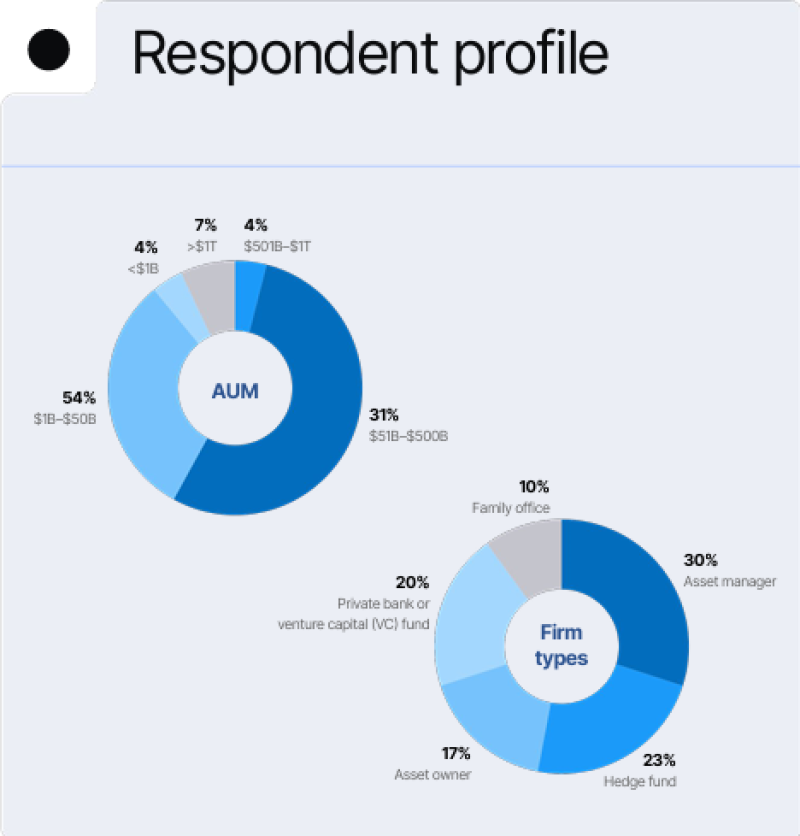

The survey represents the views of large institutional investors rather than crypto-native participants. More than half of respondents manage $1–50 billion in assets, while 31% oversee portfolios between $50 billion and $500 billion. Another 7% represent organizations with more than $1 trillion under management.

The respondent mix is equally representative of traditional finance. Asset managers account for 30% of participants, hedge funds 23%, private banks and venture capital firms 20%, asset owners 17%, and family offices 10%.

This profile matters because it frames the rest of the survey. The discussion is no longer whether institutions are entering crypto markets. The respondents are already active participants. The remaining question is how institutional capital will be deployed over the coming years.

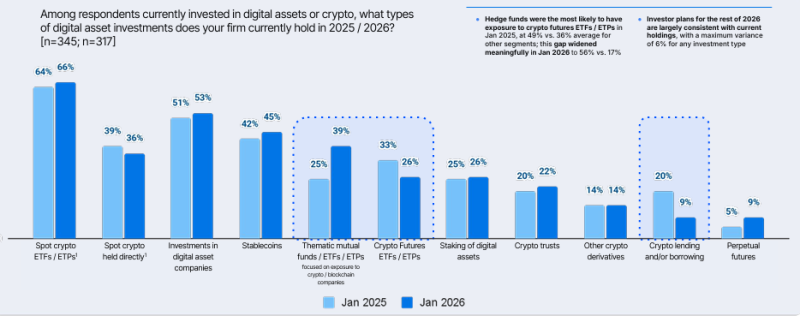

Exposure is becoming more selective

Portfolio allocations show a clear preference for investment vehicles that integrate easily into existing institutional workflows. Spot crypto ETFs remain the most widely held product, increasing from 64% to 66% year over year. Exposure to digital asset companies also edged higher, from 51% to 53%, while stablecoin adoption increased from 42% to 45%. The strongest growth occurred in thematic crypto mutual funds and ETFs, where participation rose from 25% to 39%.

Other segments moved in the opposite direction. Direct ownership of cryptocurrencies declined from 39% to 36%. Crypto futures fell from 33% to 26%, while crypto lending dropped sharply from 20% to 9%. Viewed together, these figures point to a broader shift in institutional preferences. Rather than increasing operational complexity through direct ownership, investors are favoring regulated products that fit established compliance, custody and reporting frameworks.

For many institutions, the preferred way to own crypto is increasingly through familiar financial infrastructure rather than through native blockchain tools.

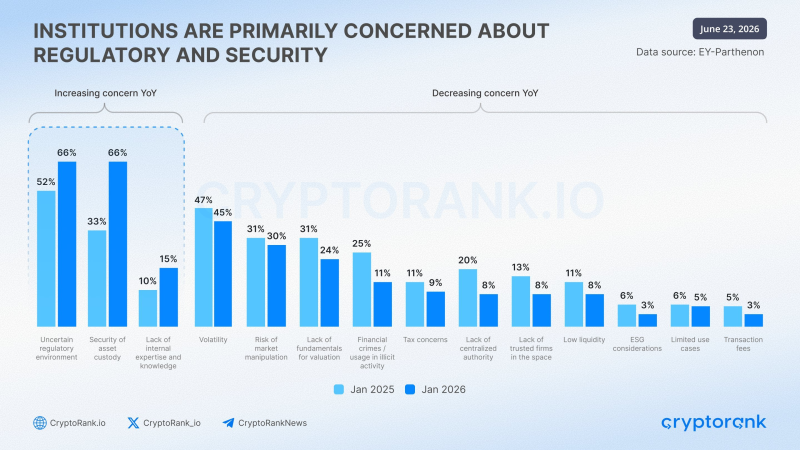

Risk priorities have changed

The survey also highlights a significant change in how institutions assess risk. Volatility, once the defining institutional concern, has become relatively stable, declining slightly from 47% to 45%. Concerns about financial crime fell from 25% to 11%. The perceived absence of centralized oversight declined from 20% to 8%, while liquidity, transaction fees and tax-related issues all became less prominent.

The fastest-growing concerns are different. Regulatory uncertainty increased from 52% to 66%, while concern over asset custody security rose from 33% to 66%, making both the highest-ranked issues in the survey. This suggests institutional investors are shifting their attention away from the behavior of crypto assets themselves and toward the infrastructure supporting those assets. Market risk is becoming easier to price. Operational risk is becoming harder to ignore.

Capital is beginning to reward infrastructure

The three charts describe the same structural transition from different perspectives. Institutions are maintaining or expanding digital asset exposure, but they increasingly prefer investment products supported by regulated intermediaries, institutional custodians and standardized operational processes.

That preference changes where value may accumulate across the industry. Demand is likely to extend beyond cryptocurrencies themselves toward businesses providing the infrastructure required by institutional investors. ETF issuers, custody providers, tokenization platforms, stablecoin networks, institutional exchanges and compliance technology all benefit from the same long-term trend: digital assets becoming part of conventional portfolio management.

As adoption matures, infrastructure becomes a larger determinant of capital allocation than the underlying technology alone.

The next phase of institutional adoption

Earlier cycles were largely defined by access. The current cycle is increasingly defined by implementation. Institutional investors already have multiple ways to gain exposure to digital assets. Their competitive advantage now depends on selecting products and service providers that satisfy governance standards, regulatory requirements and operational controls.

The survey suggests that the next stage of industry growth will be driven less by expanding interest in crypto and more by improving the financial infrastructure surrounding it. In that environment, the strongest competitive positions may belong not only to the issuers of digital assets, but also to the companies that make institutional participation predictable, compliant and scalable.

Victoria Bazir

Victoria Bazir