Usman Salis

Usman Salis

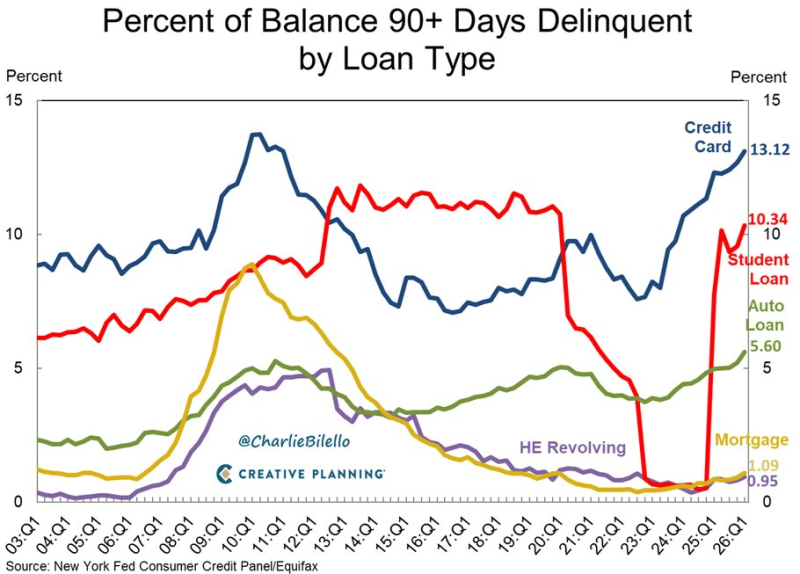

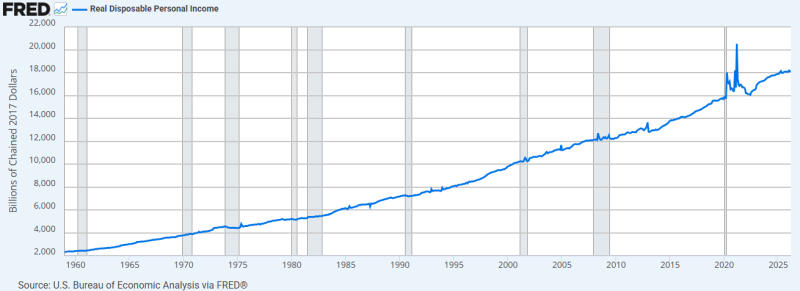

The latest data from the New York Fed reveal a striking disconnect in the U.S. economy. The share of credit card balances that are 90 days or more delinquent has climbed to 13.12%, the highest level on the chart and above both pre-pandemic and post-pandemic norms. At the same time, real disposable personal income has continued to rise, approaching record levels. If Americans are earning more than ever, why are more borrowers falling behind on their credit card payments?

Borrowing Costs Have Reached Multi-Decade Highs

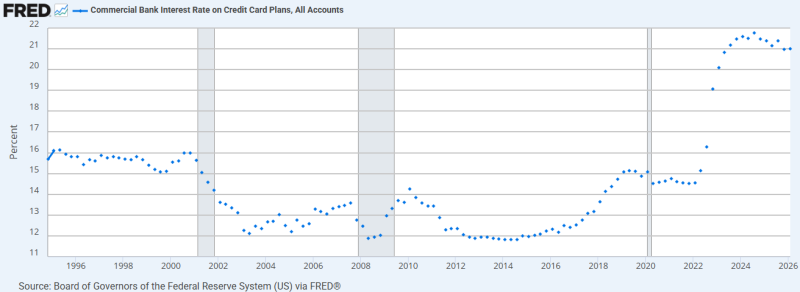

Part of the answer lies in the cost of borrowing. The average interest rate charged on credit card accounts has climbed dramatically over the past decade, rising from roughly 12% in 2014–2015 to more than 21% in 2024. Although rates have eased slightly, they remain near 20.8%, close to the highest level in the history of the series.

For borrowers carrying revolving balances, higher rates translate directly into larger monthly interest charges. As financing costs increased, servicing debt became more expensive even for households whose incomes were still growing. The acceleration in delinquencies closely follows the period when credit card rates moved above 20%, suggesting that borrowing costs have become a significant source of financial pressure.

Americans Are Carrying More Debt Than Ever

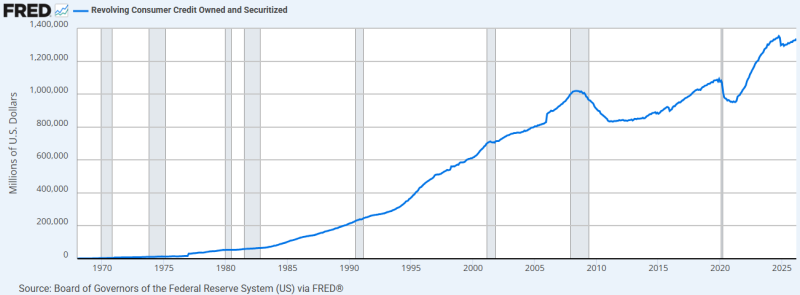

Rising rates are only part of the story. Americans are also carrying more debt than ever before. Revolving consumer credit outstanding has expanded to nearly $1.3 trillion, up sharply from pandemic-era levels and well above previous peaks.

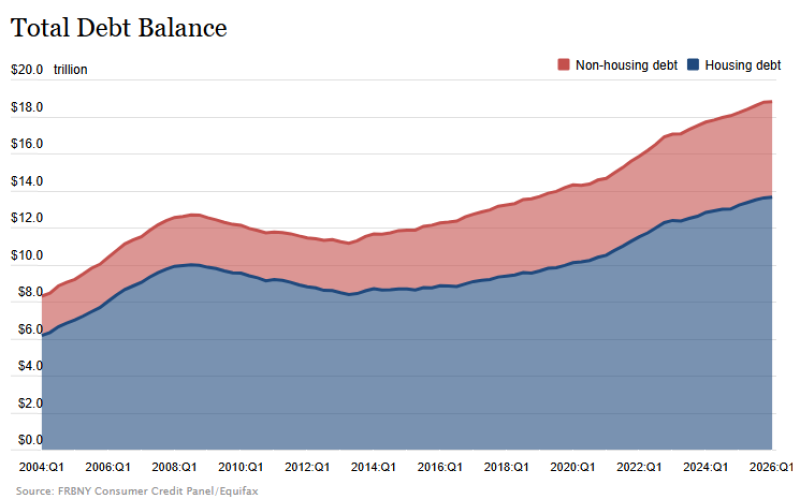

The broader household balance sheet tells a similar story. Total U.S. household debt recently reached approximately $18.2 trillion, including about $13.2 trillion in housing-related debt and roughly $5 trillion in non-housing obligations such as credit cards, auto loans, and student debt.

This combination of larger balances and higher interest rates means many households are facing significantly higher debt-servicing costs than they were just a few years ago. While income has increased, a growing share of that income is being absorbed by interest payments and other financial obligations.

Rising Income Does Not Mean Equal Financial Strength

Real disposable personal income continues to trend upward and recently approached $18 trillion in inflation-adjusted annualized terms.

The contrast between income growth and rising delinquencies suggests that the problem is not a lack of income at the aggregate level, but the uneven impact of debt costs across households. Consumers who rely heavily on variable-rate borrowing are far more exposed to higher interest expenses than homeowners locked into low fixed-rate mortgages.

This Is Not a Repeat of the 2008 Housing Crisis

That distinction is visible in the delinquency data. Mortgage delinquency rates remain near 1.09%, while home-equity revolving credit delinquencies stand at 0.95%. In contrast, credit card delinquencies have exceeded 13%, student loan delinquencies have reached 10.34%, and auto loan delinquencies have climbed to 5.60%.

Unlike the 2008 financial crisis, when mortgage defaults were the primary source of stress, today's weakness is concentrated in unsecured consumer credit. The data suggest that record household income alone is no longer enough to offset the effects of record debt balances and historically high credit card rates. As borrowing costs remain elevated, the gap between income growth and debt-servicing costs may continue to shape the outlook for U.S. consumers and the broader credit market.

Usman Salis

Usman Salis