Marina Lyubimova

Marina Lyubimova

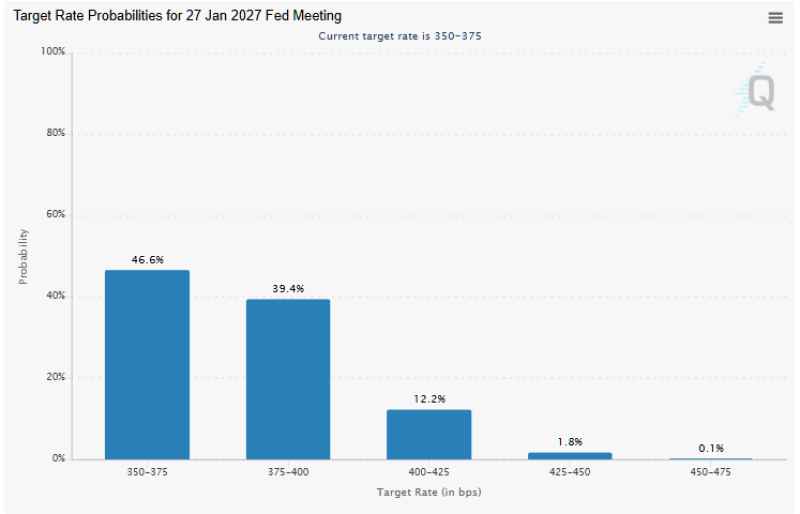

FedWatch probabilities tied to the January 2027 meeting now show only a 46.6% chance that rates remain in the current 350–375 bps range. Another 39.4% points to 375–400 bps, while higher ranges above 4% are also gaining probability.

That shift matters because rate expectations drive valuations across equities, bonds, and growth assets. For years, markets assumed restrictive policy would eventually give way to lower rates and renewed liquidity. Current pricing suggests confidence in that outcome is fading.

One reason is the resilience of the U.S. economy. Labor markets remain stable, fiscal spending continues to support demand, and AI infrastructure investment has introduced a new source of capital intensity into the system. The AI cycle is becoming increasingly relevant to macro markets because it extends far beyond software. It requires semiconductors, power infrastructure, cooling systems, grid upgrades, and large-scale data-center construction — all areas associated with sustained industrial spending.

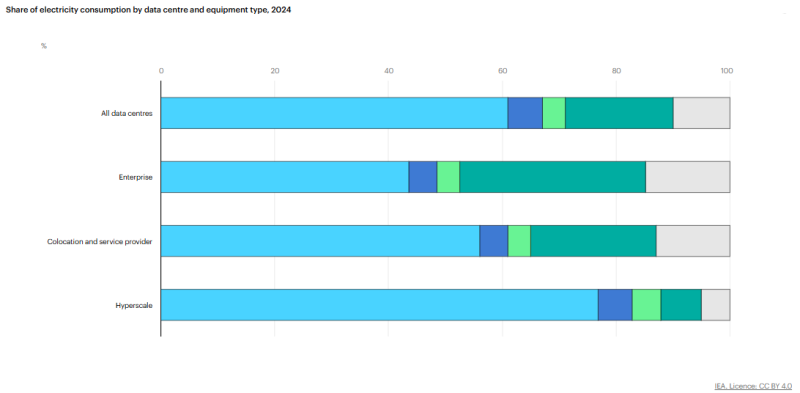

The repricing is also tied to rising electricity demand from hyperscale AI infrastructure.

Hyperscale facilities already account for the largest share of data-center electricity usage. That matters because continued AI expansion implies ongoing spending across energy and infrastructure markets.

Three themes are now converging:

- AI infrastructure spending remains elevated

- Energy demand tied to hyperscale computing continues to rise

- Rates markets are becoming less confident about rapid policy easing

This helps explain why markets are slowly abandoning the assumption of a quick return to the low-rate environment that defined the 2010s. Another important detail is the asymmetry in current Fed pricing. Markets assign virtually no probability to rate cuts below current levels by January 2027. The dominant concern is no longer recession. It is inflation remaining high enough to prevent normalization.

That creates pressure on sectors dependent on cheap capital and higher equity multiples. Ironically, the same AI-driven investment boom fueling market optimism may also be contributing to the macro conditions keeping rates elevated. The Fed may not explicitly frame policy around AI infrastructure. Markets increasingly do.

Marina Lyubimova

Marina Lyubimova