Artem Voloskovets

Artem Voloskovets

Investors treated Asian equities as one of the clearest expressions of global growth. When liquidity expanded, capital flowed into exporters, industrial supply chains, banks, and consumer giants across the region. But a different pattern has quietly emerged beneath the surface of the post-pandemic market cycle - one where Asia increasingly behaves like the first casualty of rising US yields.

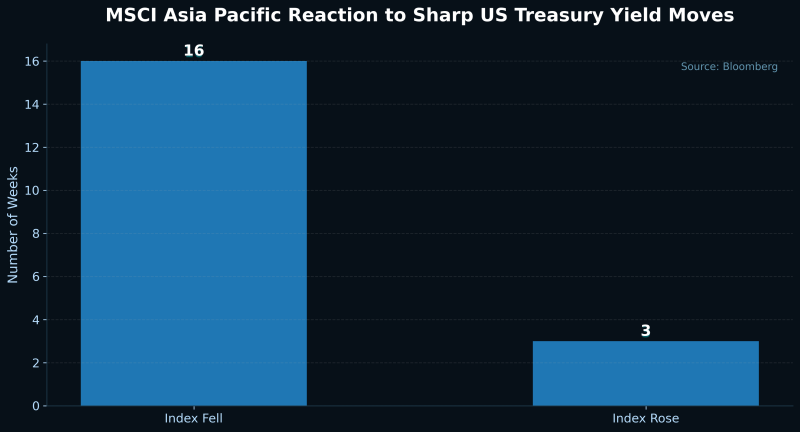

Bloomberg data highlights just how consistent that relationship has become. Over the past five years, the MSCI Asia Pacific Index declined in 16 out of 19 weeks when the US 10-year Treasury yield climbed by at least 20 basis points. The average weekly decline: 1.6%. That statistic is less about volatility than about dependency.

Asian markets sit at the intersection of nearly every major macro force dominating the current cycle: dollar liquidity, energy imports, Chinese growth expectations, and global manufacturing flows.

When Treasury yields spike aggressively, pressure tends to arrive everywhere at once. Financing conditions tighten. The dollar strengthens. Emerging-market currencies weaken. Foreign capital starts repricing risk exposure globally rather than locally. And Asia feels that repricing faster than most regions.

What makes the current environment more complicated is that rising yields are no longer being interpreted purely through the lens of inflation fear. Increasingly, markets are treating higher Treasury yields as evidence that the US economy can sustain restrictive financial conditions longer than expected. That shifts the psychological meaning of rates moves.

A few years ago, surging yields implied overheating and an eventual policy reversal. Today, they increasingly suggest resilience - and resilience in the US often comes at the expense of liquidity-sensitive international equities.

That dynamic leaves Asian markets in an unusually fragile position. Investors searching for safety during bond-market repricings tend to consolidate around dollar-denominated assets, particularly US Treasuries and large-cap American equities. The stronger the yield shock becomes, the harder it is for international markets to compete for capital.

The result is a market increasingly trapped between two forces:

- dependence on global growth

- vulnerability to tighter dollar liquidity

That combination becomes especially unstable during sharp bond-market repricings.

There is also a structural layer beneath the data. Many Asian economies remain highly sensitive to imported energy costs and external financing conditions. Rising Treasury yields tend to ripple outward through currency markets, sovereign debt spreads, and funding costs long before they fully impact US equities. The speed of transmission matters. Asian stocks often react not to recession itself, but to the tightening of financial conditions preceding it.

This is why weeks like these matter beyond short-term market performance. The relationship between Treasury yields and Asian equities is becoming less cyclical and more systemic. As long as global capital remains concentrated around dollar liquidity and US assets, Asia may continue absorbing the shockwaves of every major repricing in the bond market.

Artem Voloskovets

Artem Voloskovets