Artem Voloskovets

Artem Voloskovets

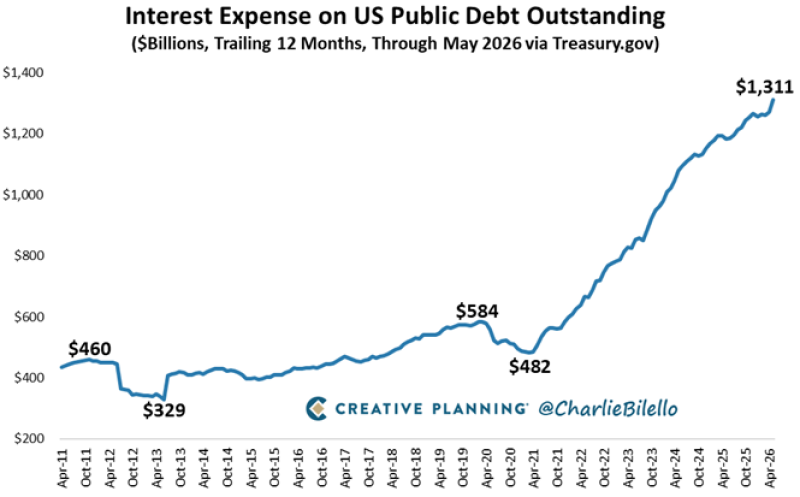

Treasury data shows annual interest expenses on federal debt reached approximately $1.31 trillion through May 2026. Unlike spending on infrastructure, healthcare, or defense, this money does not create new assets or services. It covers the cost of past borrowing.

The rise has been so rapid that interest payments are becoming one of the largest budget items in Washington.

From $329 Billion to $1.31 Trillion

For most of the previous decade, federal interest expenses fluctuated near the $400 billion mark. Despite a growing debt load, borrowing remained relatively cheap. Treasury securities issued after the 2008 financial crisis carried historically low yields, allowing the government to expand debt without seeing a proportional rise in financing costs. That relationship broke down after 2022.

The chart shows how quickly the trend accelerated:

- $329 billion in 2013;

- about $460 billion before the pandemic;

- a temporary peak near $584 billion in 2020;

- a decline toward $482 billion;

- a surge to $1.31 trillion by May 2026.

The increase reflects refinancing rather than a sudden borrowing spree. As older debt matures, it is replaced with securities carrying significantly higher interest rates than those issued during the era of near-zero rates.

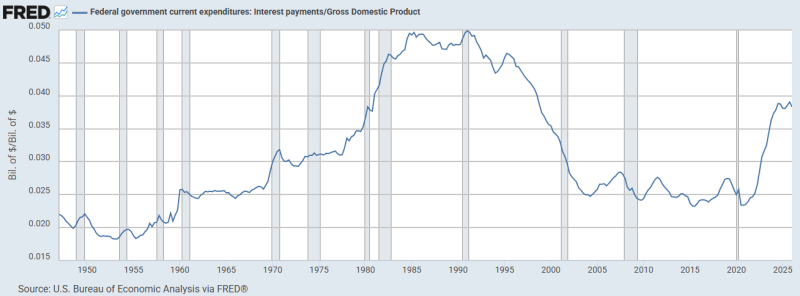

The Number Looks Different Relative to the Economy

A trillion-dollar interest bill is striking, but the figure becomes more useful when compared with economic output.

Measured against GDP, federal interest payments currently account for roughly 3.8% of the economy. That level is elevated by post-2008 standards, yet it remains below the highs recorded during the 1980s and early 1990s, when the ratio approached 5%.

The comparison changes the interpretation of the first chart. The United States is paying more interest than ever in nominal dollars, but the burden has not yet exceeded previous historical peaks once economic growth is taken into account.

The economy has expanded substantially over the last four decades. As a result, larger dollar figures do not automatically translate into a heavier economic load.

Why Interest Costs Keep Rising Even Without New Spending

A common misconception is that interest expenses rise only when governments dramatically increase borrowing. In reality, the existing debt stock plays an equally important role. Much of the federal debt issued during the low-rate years is now reaching maturity. Every time that debt is rolled over, the Treasury must refinance at prevailing market rates. When rates were close to zero, refinancing lowered financing costs. Today, refinancing often produces the opposite result. This explains why interest expenses continue climbing even during periods when borrowing growth slows.

A Budget Item That Is Getting Harder to Ignore

Interest payments were once a relatively modest part of federal spending. That is no longer the case. As debt-servicing costs approach the scale of major government programs, they leave policymakers with fewer options. Every dollar allocated to interest is a dollar unavailable for other priorities without additional borrowing.

The issue is not that the United States faces an immediate funding crisis. Treasury securities remain among the most sought-after financial assets in the world, and demand for government debt remains strong. The challenge is mathematical rather than political. A larger debt base combined with higher interest rates creates expenses that grow automatically, regardless of policy goals.

The Trend Behind the Headlines

The first chart captures the speed of the increase. The second provides the context. Together, they show that the discussion around federal debt is gradually shifting. The focus is moving away from the size of the debt itself and toward the cost of carrying it.

For more than a decade, exceptionally low rates allowed Washington to borrow with limited consequences for annual financing costs.

That period has ended. The most important debt statistic in the coming years may not be how much the United States owes, but how much it spends to keep that debt in place.

Artem Voloskovets

Artem Voloskovets