Artem Voloskovets

Artem Voloskovets

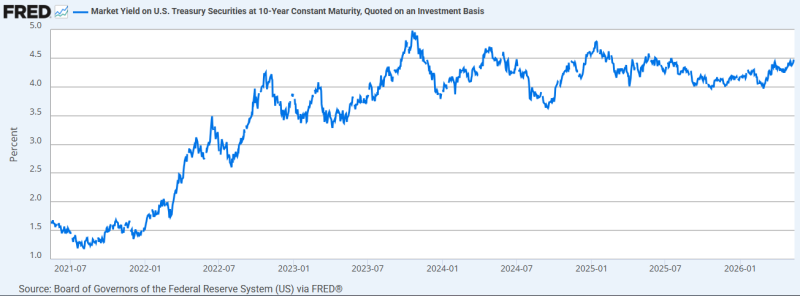

The U.S. 10-year Treasury is back above 4.6%. UK 30-year yields are approaching multi-decade highs. Japanese government bond yields are climbing again after years of aggressive Bank of Japan suppression. Europe and Canada are moving higher as well.

This is no longer a local inflation story. It is becoming a global repricing of sovereign debt. That matters because bond markets sit underneath the entire financial system. Stocks, mortgages, venture capital, commercial real estate, corporate debt, and government spending all price off sovereign yields. When yields rise globally and simultaneously, stress spreads everywhere.

Markets are starting to focus on debt supply, not inflation

Higher yields were explained by inflation and central bank tightening. Now markets are beginning to focus on something else:

Who is going to buy the massive amount of debt governments need to issue?

That question is becoming more important because nearly every major economy now faces the same pressures:

- structurally high deficits;

- rising military spending;

- aging populations;

- energy transition costs;

- expensive refinancing cycles.

Governments need trillions in new borrowing at the same time liquidity is becoming tighter and more expensive. This is starting to look structural rather than cyclical.

Japan is one of the biggest risks

Japan matters more than most investors realize. For decades, ultra-low Japanese yields pushed domestic capital into global markets. Japanese institutions became major buyers of foreign bonds because domestic returns were close to zero. Now Japanese yields are rising again. Even small moves matter because they can trigger large capital reallocations. If Japanese investors can earn more at home, part of that overseas capital eventually returns to Japan.

That creates pressure across global debt markets:

- weaker demand for U.S. Treasuries;

- tighter global liquidity;

- higher refinancing costs;

- more fragile leveraged trades.

Markets spent years adapting to a world flooded with Japanese capital searching for yield. Very few systems are prepared for the reverse.

Higher yields are colliding with debt-heavy economies

The biggest problem is not simply that borrowing costs are higher. Modern economies became dependent on cheap money. Governments, corporations, real estate markets, and private equity all expanded during a decade of near-zero rates. Large parts of the financial system were built around the assumption that refinancing would remain manageable. That assumption is breaking down.

Commercial real estate is already struggling with refinancing pressure. Venture capital has slowed because capital is no longer effectively free. Private equity firms are finding it harder to exit deals financed during the low-rate era. Governments face the same issue.

As yields rise, debt servicing costs rise with them. That creates a dangerous feedback loop:

| Problem | Effect |

| Higher deficits | More debt issuance |

| More issuance | Higher yields |

| Higher yields | Rising refinancing costs |

| Rising refinancing costs | Larger deficits |

At some point, markets stop pricing growth and start pricing debt sustainability itself.

Bond markets are becoming the main macro story again

For years, equities dominated market attention. AI stocks, crypto, and mega-cap tech pulled focus away from fixed income. That is starting to change.

When sovereign yields move aggressively higher:

- growth valuations compress;

- refinancing risk increases;

- speculative capital disappears;

- weak balance sheets get exposed.

This is why rising yields eventually become an economy-wide problem rather than just a bond-market story. The transition from cheap capital to expensive capital forces markets to reprice risk across every sector simultaneously.

Liquidity is weaker than markets assume

The current system was built during an era of heavy central bank support and low volatility. Many institutional strategies still assume relatively stable bond markets. That becomes dangerous when sovereign yields move sharply across multiple regions at once.

Financial stress rarely begins where investors expect. It usually appears inside:

- leveraged trades;

- collateral markets;

- pension structures;

- shadow banking systems;

- funding markets.

The UK pension crisis in 2022 already showed how quickly sovereign yield volatility can destabilize supposedly conservative institutions. The difference now is scale. This is no longer isolated volatility, it is happening globally.

This is becoming a structural transition

Several long-term forces are now colliding simultaneously:

- deglobalization;

- persistent fiscal spending;

- geopolitical fragmentation;

- industrial policy;

- AI infrastructure spending;

- energy transition investment.

All of them require enormous amounts of capital. All of them increase debt issuance pressure and all of them are emerging after more than a decade of artificially suppressed rates. That combination may define the next decade of markets more than AI hype or equity narratives themselves. Because underneath every major financial story sits the same question:

What happens when the price of money stays structurally higher for years instead of months?

Artem Voloskovets

Artem Voloskovets