Artem Voloskovets

Artem Voloskovets

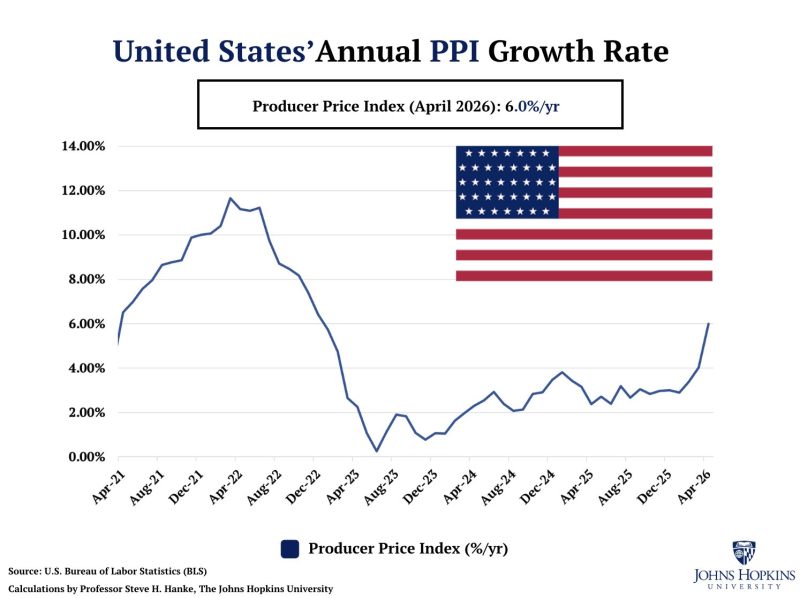

Participants in the market directed their attention toward expenditures on AI, the ability of earnings to remain steady and the belief that the period of high prices after the pandemic was decreasing. It appeared that prices for producers were under control when compared to the sudden increase in 2022.

But recent information indicates that this feeling of certainty is perhaps too early.

In recent months the Producer Price Index for all commodities rose again to a level near 280, which is a value that is historically high. Before the pandemic occurred, the index remained between 180 and 200 for many years. Even after the sharp rise in prices in 2022 ended, the prices that producers pay did not return to the levels that existed before COVID-19.

This is important because price increases for producers typically spread through the economy over a period of time. For a short time companies are able to pay those higher costs themselves. If the costs continue to rise, they eventually affect profit margins, the prices set for consumers and how companies distribute their money.

By and large, markets are still treating inflation as if it is a problem that is going away - but the next period of rising prices is likely to be different from the previous one.

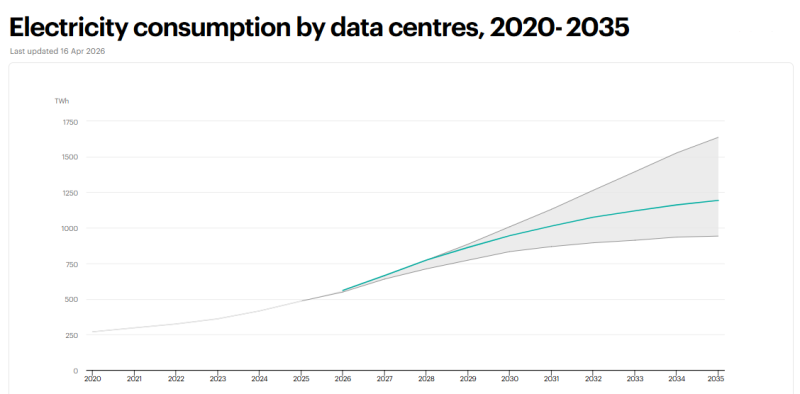

To understand this, consider that the first period happened because of government spending and problems with how goods are moved. In the future the rise in prices is likely to come from the need for physical structures that support AI.

As stated in projections by the IEA, the amount of electricity that data centers use globally is expected to grow from about 500 - 600 TWh in 2026 to about 1 200 TWh in 2035 in the standard scenario. If the growth is at the top of the projected range, the amount used is near 1 600 TWh.

There is a very large growth in the needs of industry over a time frame of less than ten years.

For AI infrastructure to work, more than software is necessary. When companies expand the capacity of data centers, they create a higher need for electricity, transformers, cooling systems, semiconductors, copper, steel and the building of power grids. And all of the areas are directly affected by the prices that producers must pay.

Due to those factors, the current period is perhaps becoming fundamentally different from the time before 2020 when prices did not rise quickly. On the stock market, investors still view AI as something that primarily makes workers more efficient - but the act of building the physical parts of the AI economy is requiring more and more physical materials.

It is a paradoxical situation where AI is perhaps able to lower prices for software while it simultaneously causes prices to rise for infrastructure.

And if the prices for producers continue to go up at the same time as the need for power in data centers, markets are likely to see that inflation is not gone. It is simply present in a different way.

Artem Voloskovets

Artem Voloskovets