Victoria Bazir

Victoria Bazir

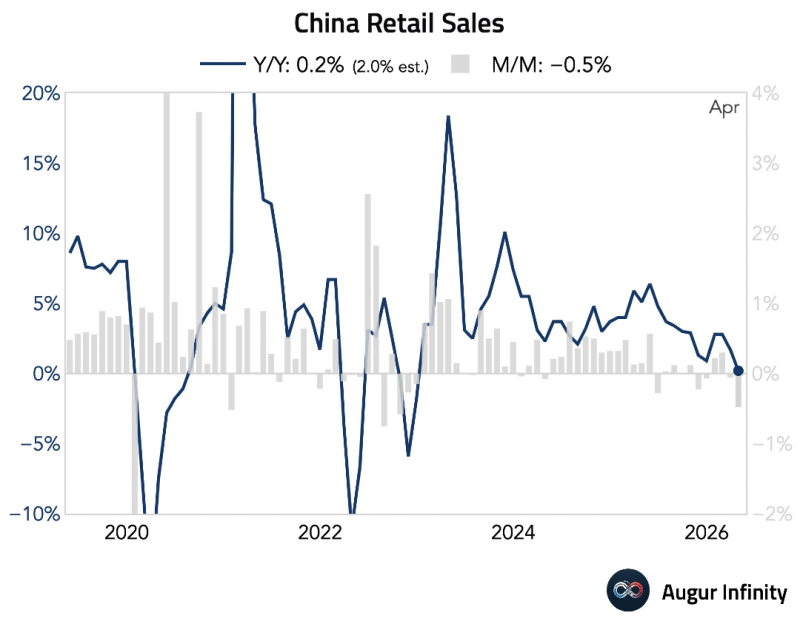

Retail sales rose only 0.2% year-over-year versus expectations of 2%. On a monthly basis, sales posted their sharpest decline since late 2022.

China retail sales growth slowed to 0.2% year-over-year, while monthly sales saw their sharpest decline since late 2022. This no longer looks like a temporary slowdown caused by uneven reopening effects or weak sentiment after the pandemic. Chinese consumers are still behaving defensively despite years of stimulus, policy support, and repeated expectations of recovery. That is becoming a structural problem.

China’s recovery still lacks real consumer confidence

In a normal recovery cycle, households gradually increase discretionary spending as confidence improves. Consumption usually stabilizes before the broader economy fully recovers. That dynamic is missing in China.

Consumers continue saving aggressively and spending selectively. Demand remains weak even while Beijing tries to support growth through industrial policy, infrastructure spending, and targeted stimulus measures. The issue is no longer simply weaker retail activity, it is weak confidence.

That matters because China is trying to shift away from an economy heavily dependent on:

- real estate;

- exports;

- infrastructure investment;

- debt-fueled growth.

A sustainable transition requires stronger domestic consumption. So far, that transition is not happening fast enough.

The property market is still driving consumer behavior

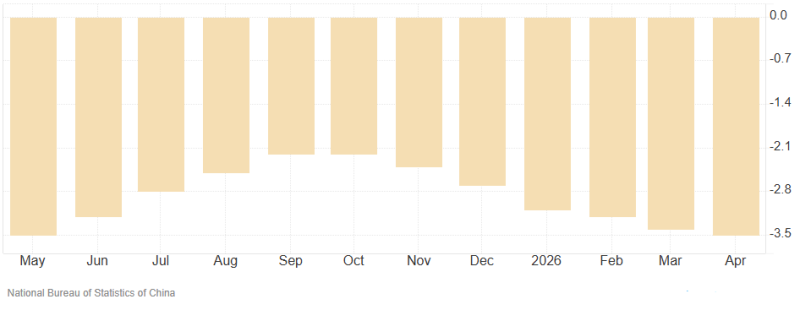

China’s retail slowdown cannot really be separated from the property market. For years, rising home prices supported household confidence and consumer spending. Real estate became the primary store of wealth for large parts of the population. That model is weakening. Housing demand remains soft, developers are still under pressure, and property prices continue falling across much of the market.

Chinese residential property prices continue declining, reinforcing pressure on household confidence and consumer spending. This second chart explains part of the retail weakness. Consumers do not spend aggressively when they feel less wealthy.

That creates a difficult cycle:

- weaker property prices reduce confidence;

- weaker confidence hurts spending;

- weaker spending slows business activity;

- slower activity pressures income growth again.

At some point, temporary caution becomes long-term behavior.

Markets may still be underestimating the global impact

China’s consumer slowdown is not only a domestic issue. Global markets spent two decades adapting to China as a major source of demand. Commodities, luxury brands, tourism, industrial equipment, semiconductors, and global manufacturing chains all became tied to Chinese consumption growth.

If Chinese households remain structurally cautious, several assumptions begin to break:

- global growth forecasts become harder to sustain;

- commodity demand weakens;

- luxury spending slows;

- multinational earnings expectations become less reliable.

This matters even more in a world already dealing with:

- higher interest rates;

- tighter liquidity;

- rising debt costs;

- weaker trade growth;

- geopolitical fragmentation.

Investors assumed China would eventually stabilize global growth during periods of weakness. That assumption is becoming less certain.

The bigger risk is deflation psychology

The biggest danger is not slower retail growth alone. It is the possibility that weak consumption becomes psychologically embedded. When consumers expect weak growth, uncertain income, and falling prices, they delay spending. Businesses then become more cautious with hiring and investment. Demand weakens further. That cycle becomes difficult to reverse once expectations change. Japan spent decades struggling with versions of this problem.

China’s economy is different, but markets are increasingly paying attention to the risk of prolonged consumer stagnation rather than a short-term slowdown. That is why this retail sales report matters beyond a single economic release. The issue is no longer whether China’s recovery is slower than expected. The issue is whether the country is entering a much longer transition away from the growth model that defined the last two decades.

Victoria Bazir

Victoria Bazir