Eseandre Mordi

Eseandre Mordi

Institutions in Japan previously purchased US Treasuries with high frequency - this activity is currently decreasing.

By the latest data from the Ministry of Finance in Japan, investors are selling US sovereign debt at the fastest rate since 2022. For the most recent quarter, net selling is approximately ¥5 trillion after multiple years of generally positive purchases.

As the domestic bond market in Japan begins to provide returns that were largely unavailable during the period of expansive monetary policy, this change occurs.

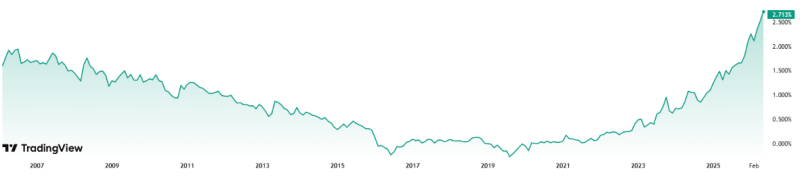

In Japan, the yield for 10-year government bonds is approximately 2.7%, which is the highest value in nearly twenty years. During the years from 2016 - 2022, yields were frequently near zero percent because of the yield curve control policy of the Bank of Japan.

To generate income, pension funds, insurers and banks in Japan are no longer required to use foreign bonds.

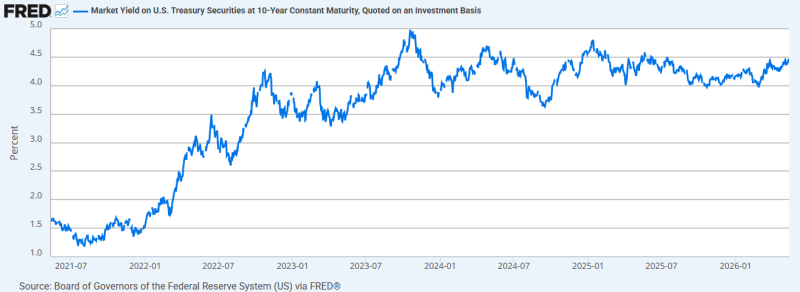

At the same time yields in the US are at high levels.

On the US 10-year Treasury, the yield is above 4.3% and is near the top of its range since 2023. Under standard market conditions, this level is likely to attract buyers from other countries. But the costs to hedge against currency fluctuations lower the benefits of purchasing Treasuries for those in Japan. And the difference between “safe yield abroad” and “safe yield at home” is now smaller.

There is a structural issue for markets involving Treasuries.

For many years Japan is a primary source of external funding for the debt of the US government. If capital from Japan remains in the domestic market, the US is more reliant on internal buyers and a reduced group of international participants while the issuance of debt increases.

It is true that the chart by itself is not an indicator of a crisis for Treasuries. But it shows that a consistent source of support for US debt markets is no longer certain.

Eseandre Mordi

Eseandre Mordi