Marina Lyubimova

Marina Lyubimova

European defense contractors traded like cyclical industrial companies tied to temporary geopolitical crises. That framework is changing. Defense is increasingly being priced as permanent industrial policy tied to security, manufacturing capacity, aerospace independence and supply-chain control.

The company combines aerospace systems, military electronics, helicopters, cybersecurity, radar infrastructure and sovereign defense technologies. As Europe pushes toward strategic autonomy, markets are starting to value companies like Leonardo less as contractors and more as long-duration infrastructure assets.

Markets Are Starting to Treat Defense Like Infrastructure

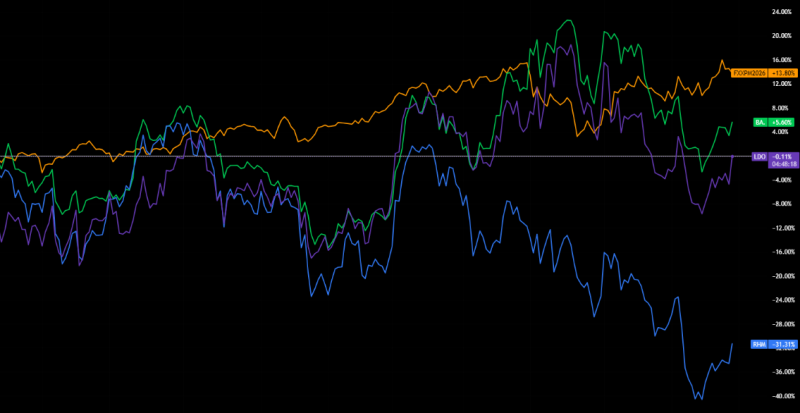

The rerating is no longer isolated to one company. Europe’s broader defense sector has started separating sharply from traditional industrial benchmarks as investors reposition around long-duration security spending and sovereign manufacturing capacity.

Rheinmetall dramatically outperformed broader European industrial stocks over the past two years as markets repriced military procurement visibility and strategic industrial capacity. Leonardo and BAE Systems also significantly diverged from the broader industrial sector, reflecting growing investor demand for companies tied to Europe’s rearmament and infrastructure rebuilding cycle.

The divergence matters because markets are no longer pricing European defense companies as cyclical manufacturers reacting to temporary geopolitical shocks. Instead, investors increasingly view sovereign aerospace systems, cybersecurity infrastructure, radar networks and domestic manufacturing capacity as strategic assets supported by multi-year political spending commitments. That dynamic changes valuation behavior entirely.

Defense order books begin behaving less like cyclical industrial demand and more like infrastructure pipelines backed by government priorities.

Europe Is Moving From Efficiency to Sovereignty

Europe spent decades optimizing for globalization, outsourced manufacturing and supply-chain efficiency. Markets are now rewarding domestic production, industrial resilience and strategic control instead. That shift extends far beyond defense spending itself. Europe’s sovereignty push increasingly overlaps with semiconductor access, cyber infrastructure, satellite systems, aerospace independence and energy resilience.

Europe’s Strategic Sovereignty Trade

| Strategic Layer | Why Markets Care |

| Defense Manufacturing | Multi-year procurement visibility |

| Aerospace Systems | European strategic independence |

| Cybersecurity Infrastructure | Digital sovereignty and resilience |

| Satellite & Radar Systems | Communications and surveillance |

| Industrial Capacity | Domestic production and supply-chain resilience |

Strategic Autonomy Is More Expensive Than Globalization

Rebuilding sovereign industrial capacity requires permanently higher capital spending, duplicated infrastructure and domestic manufacturing subsidies. Markets may still be underestimating how inflationary that transition could become. But companies positioned near the center of Europe’s industrial rebuilding cycle may continue benefiting from the repricing. The previous market cycle rewarded scalability and efficiency. The next one may increasingly reward resilience, sovereignty and industrial control.

Marina Lyubimova

Marina Lyubimova