Marina Lyubimova

Marina Lyubimova

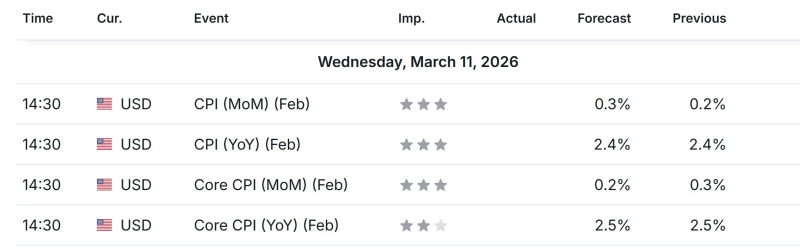

The U.S. dollar and global financial markets are bracing for the February Consumer Price Index report, due at 8:30 AM ET. Traders are watching closely for any signals on inflation direction and what it might mean for Fed policy. Consensus forecasts point to relatively stable readings compared with January's numbers.

Headline CPI month over month is expected to rise 0.3% in February, slightly above the prior 0.2% reading. Year over year, headline inflation is forecast to hold at 2.4%, suggesting price pressures may be stabilizing after years of elevated readings. Official CPI figures have remained near this level even as alternative data sources tell a different story.

Inflation readings near 2.4% suggest that overall price pressures may be stabilizing - but the gap between official data and real-time trackers continues to raise questions.

Core CPI, which strips out volatile food and energy prices, is expected at 0.2% month over month, down from 0.3% previously - a modest sign of easing. Annually, core CPI is forecast at 2.5%, flat versus the prior report. Real-time trackers have repeatedly shown inflation cooling well below official BLS figures, with some placing it closer to 0.94%.

Inflation data consistently ranks among the most market-moving macroeconomic releases. CPI shifts ripple through interest rate expectations, bond yields, currency markets, and equity valuations. The debate around official versus alternative readings remains live, with the gap between CPI and Truflation data reaching 200 basis points at certain points. As February numbers land, markets will parse both headline and core prints for clues on whether inflation is easing, holding, or turning back up.

Marina Lyubimova

Marina Lyubimova