Eseandre Mordi

Eseandre Mordi

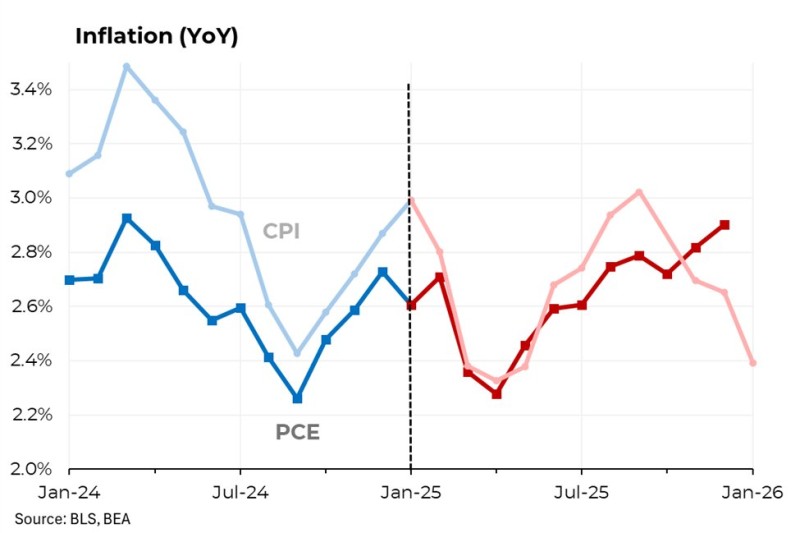

Inflation has been one of the most debated economic topics in the U.S. for the past few years. But here's what the actual data shows, as noted by economist Steven Rattner: when Donald Trump returned to the White House, price growth was already cooling. It wasn't a crisis moment, it was a slow-down in progress.

CPI Hit 3.4% in Early 2024, Then Eased Into the Transition

According to the chart tracking year-over-year Consumer Price Index and Personal Consumption Expenditures, CPI peaked above 3.4% in early 2024 before gradually easing through mid-year and stabilizing near 3.0% by January 2025. This trend has been covered in depth in US inflation climbs toward 3% as price pressures reignite, which tracks how price pressures shifted through that period.

PCE, the Federal Reserve's preferred inflation measure, followed a slightly softer path, dropping to around 2.3% in mid-2024 before climbing back toward the upper 2% range heading into 2025. The gap between the two gauges has become a recurring theme in macro analysis, explored further in Inflation gap widens: CPI and PCE track below 2.7% BLS data.

Inflation during the transition period was elevated but moderating, not at record levels.

What the 2025-2026 Projections Actually Show

Looking ahead, the chart's projections suggest moderate fluctuations rather than a dramatic resurgence. CPI is expected to briefly tick above 3% before trending lower again into early 2026, while PCE stays comparatively contained throughout. Whether that holds will depend heavily on Fed policy, as outlined in Inflation holds above Fed target as CPI and PCE flatten.

The broader picture: inflation was above the Fed's 2% target when Trump took office, but it was moving in the right direction. The data doesn't support a narrative of runaway prices at the point of the transition. It points to an economy still working through a cooling cycle, with the final stretch proving stubbornly slow.

Eseandre Mordi

Eseandre Mordi