Eseandre Mordi

Eseandre Mordi

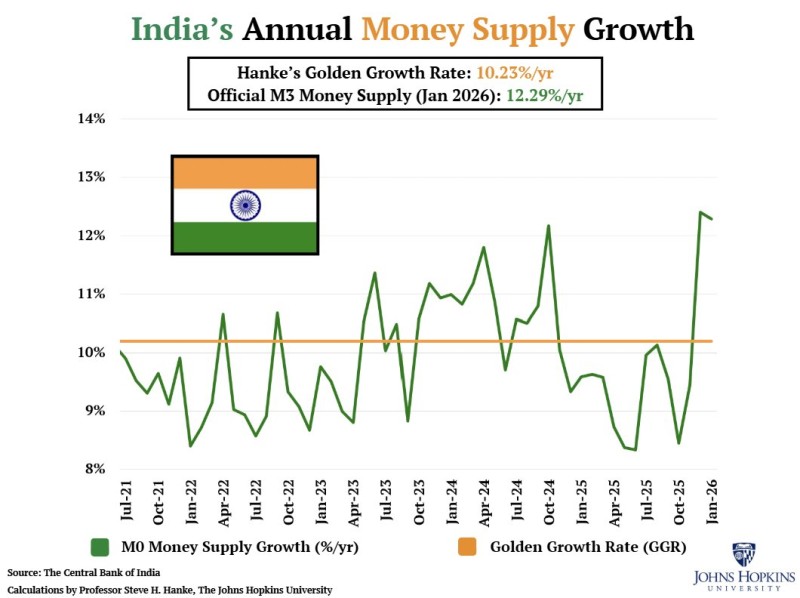

When money supply grows faster than it should, inflation tends to follow. That's the core argument economist Steve Hanke has been making for years, and India's latest figures are giving him more data to work with. In January 2026, India's M3 money supply expanded at 12.29% annually, well above Hanke's Golden Growth Rate of roughly 10.23%, while inflation climbed to 2.75% year over year. The numbers are hard to ignore.

Money Supply Running Hot Above the Golden Rate

According to data shared by Steve Hanke, India's M3 reading for January 2026 came in at 12.29%, clearly above the 10.23% Golden Growth Rate he uses as a benchmark for keeping inflation in check near India's 4% annual target. Looking back to mid-2021, money supply growth has swung between roughly 8% and above 12%, but the latest surge stands out as one of the stronger readings in that stretch. The gap between actual money growth and the Golden Growth Rate is widening, and that's exactly what Hanke points to when making his case.

You can see this dynamic playing out in broader regional context too. Similar patterns have emerged in coverage of India money supply and inflation alignment, as well as in cases like Hungary inflation linked to monetary growth trends, where liquidity expansion preceded significant price pressure.

What 2.75% Inflation Really Signals

At 2.75%, India's inflation still sits below the official 4% target, which might seem reassuring on the surface. But Hanke's framework doesn't focus on where inflation is today, it focuses on where monetary conditions point tomorrow.

The inflation story equals a money supply story.

Steve HankeIf money supply keeps running above the Golden Growth Rate, the pressure on prices tends to build over time, even if current readings look contained.

It's worth noting that this isn't just an India story. US money supply falling below its golden rate benchmark has driven a very different conversation about disinflationary trends, illustrating just how closely monetary growth tracks inflation outcomes across economies.

For India, the INR and broader currency dynamics add another layer to watch. Sustained M3 growth above the benchmark doesn't guarantee an inflation spike, but it does mean the margin for comfort is narrowing, and that's the story embedded in January's 12.29% figure.

Eseandre Mordi

Eseandre Mordi