Sergey Diakov

Sergey Diakov

The dominant narrative around sub-Saharan Africa has been remarkably consistent for years: rising debt, weak currencies, IMF dependence, and chronic fiscal fragility. The IMF’s latest fiscal balance data complicates that picture.

Africa Already Went Through Fiscal Adjustment

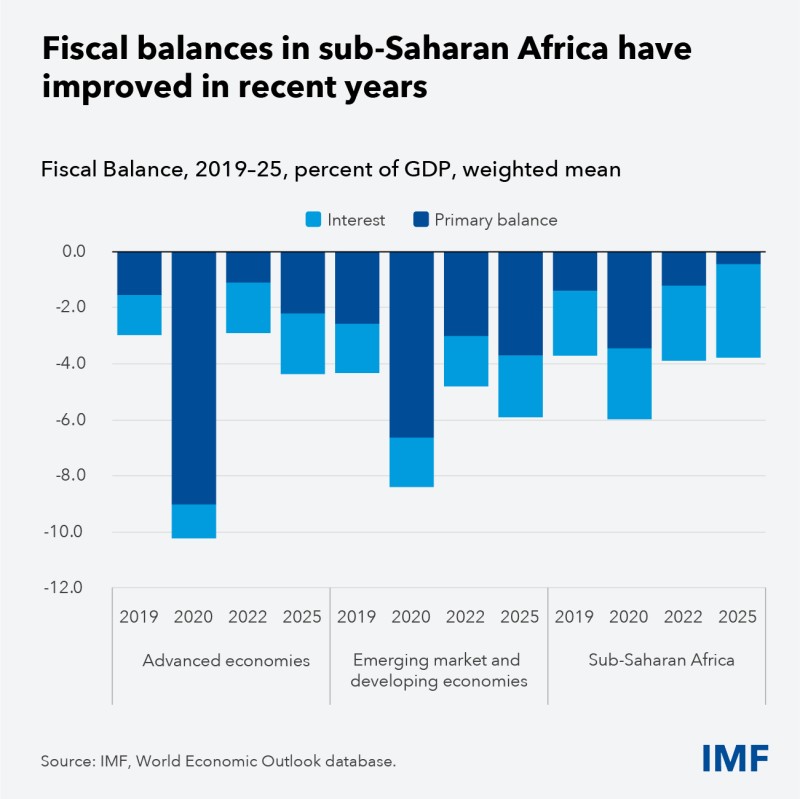

Sub-Saharan Africa’s fiscal balance has improved significantly since 2020, outperforming broader emerging market trends.

The chart shows something markets rarely focus on: fiscal deterioration in sub-Saharan Africa has slowed materially since the pandemic shock. The region’s weighted fiscal deficit narrowed from roughly 6% of GDP in 2020 to below 4% by 2025. Primary balances government budgets excluding debt servicing costs, also improved noticeably.

Direction matters more than absolute numbers. Many governments across the region are now running tighter fiscal policy despite elevated borrowing costs and difficult financing conditions. That is not the profile of a fiscal system still moving deeper into instability.

The adjustment was painful. Several economies went through IMF restructuring programs, subsidy cuts, spending reductions, currency devaluations, and tighter fiscal policy. But it forced discipline earlier.

Developed Markets Are Still Running Large Deficits

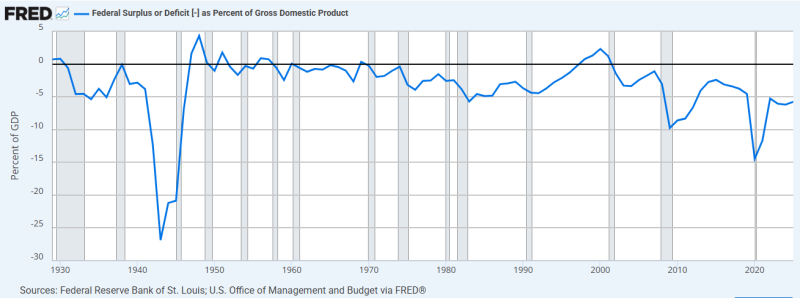

The U.S. continues running structurally large fiscal deficits years after the pandemic-era stimulus cycle.

The contrast with developed markets is becoming harder to ignore. The U.S. deficit surged to roughly 15% of GDP during the 2020 shock and remains historically elevated years later. Even after the recovery cycle, federal deficits continue running far deeper than pre-pandemic norms.

That matters because developed markets are still treated as fiscally stable by default, even while debt servicing costs continue rising. Several African economies already absorbed the adjustment cycle that developed markets may still be postponing.

That does not suddenly make sub-Saharan Africa low risk. Debt sustainability remains fragile in several countries, refinancing pressure is still significant, and political instability continues to matter. But the fiscal trajectory is no longer uniformly deteriorating.

The Risk Narrative Is Starting to Flip

This matters more than many investors realize because global capital flows are beginning to shift around infrastructure, energy security, commodities, and sovereign debt risk. Frontier economies tied to metals, agriculture, logistics, and energy production are becoming strategically more important inside that system.

That creates a dynamic markets are still slow to price: some frontier economies may enter the next decade fiscally leaner than parts of the developed world. The assumption was simple: developed markets stabilize, frontier markets adjust. The charts increasingly suggest both sides of that equation are changing at the same time.

Sergey Diakov

Sergey Diakov