Artem Voloskovets

Artem Voloskovets

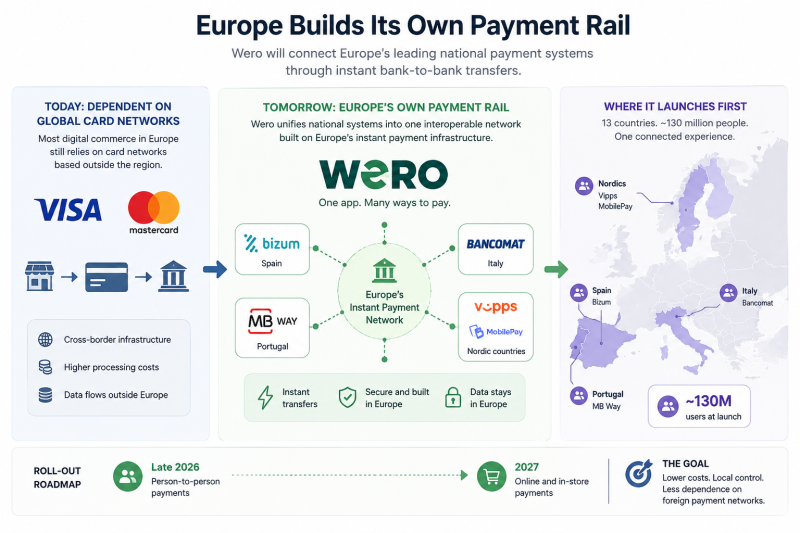

Europe is turning fragmented national payment apps into a single interoperable network. The new system connects Wero with local services including Bizum in Spain, Bancomat in Italy, MB Way in Portugal, and Vipps and MobilePay in Nordic countries. Around 130 million people are expected to gain access during the first rollout in late 2026.

The key change happens underneath the apps themselves. Instead of routing transactions through traditional card infrastructure, the system moves money instantly from one bank account to another using Europe’s own fast-payment rails. Consumers keep using familiar local apps while cross-border payments become easier inside a unified network.

That creates a direct alternative to the dominance of Visa and Mastercard in European digital commerce. The first phase focuses on peer-to-peer transfers in 2026. Online and in-store payments arrive in 2027. Europe’s goal is straightforward: reduce payment processing costs, keep transaction data inside the region, and rely less on foreign-controlled financial infrastructure.

This is not a full replacement for Visa or Mastercard. International travel, global commerce, subscriptions, and many retail systems still depend heavily on card networks. But Europe does not need to remove them entirely for the project to matter.

If bank-to-bank transfers become fast enough and widely accepted enough, a meaningful share of domestic payment volume could gradually move away from traditional card rails. The real shift is structural: Europe is starting to treat payment infrastructure the same way it now treats semiconductors, cloud computing, and AI - as a sovereignty issue rather than just a technology service.

Artem Voloskovets

Artem Voloskovets