Victoria Bazir

Victoria Bazir

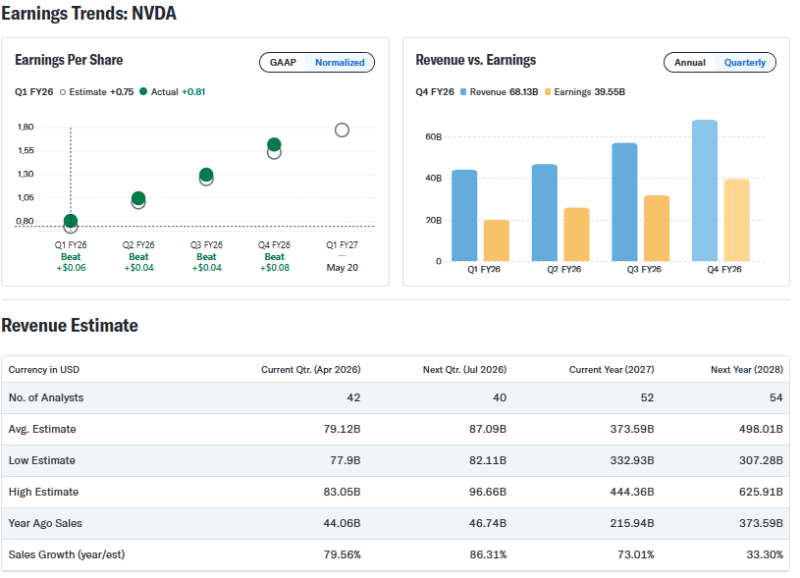

Nvidia reports earnings tonight with Wall Street expecting roughly $79.1 billion in quarterly revenue and nearly 80% year-over-year growth. Under normal circumstances, those numbers would dominate the market narrative for weeks. Instead, investors are focused on a different question: how much growth is already priced in?

The company is no longer viewed as a semiconductor stock riding a strong cycle. Nvidia has become the core infrastructure supplier behind hyperscaler expansion, datacenter buildouts and large-scale AI deployment. At roughly $5.5 trillion in valuation, the company is increasingly being priced as permanent infrastructure rather than cyclical technology.

The Market Now Expects Acceleration

Wall Street currently projects Nvidia revenue reaching nearly $374 billion for FY2027 and approaching $500 billion by FY2028. Consensus for the current quarter ranges between $77.9 billion and $83.05 billion, signaling that analysts see unusually strong demand visibility despite the company’s scale.

Nvidia has also beaten normalized EPS estimates for four consecutive quarters while quarterly revenue expanded from roughly $43 billion in Q1 FY26 to more than $68 billion by Q4 FY26.

That consistency changed market psychology. Investors are no longer rewarding Nvidia for simply outperforming estimates. The market now expects continuous acceleration. The risk is not a collapse in demand. The risk is that growth begins normalizing while positioning still assumes exponential expansion.

Key areas investors will watch tonight:

- Blackwell deployment commentary

- Gross margin trends

- Hyperscaler infrastructure spending

- Supply constraints and delivery timelines

- Forward revenue guidance

One Earnings Report Now Moves the Entire Trade

Nvidia now represents close to 8% of the S&P 500, giving a single earnings report unusual influence over passive index flows, momentum positioning and broader sentiment surrounding the infrastructure trade. A weak reaction would likely extend far beyond semiconductor stocks.

The market already assumes demand exists.

What matters tonight is whether Nvidia can still grow fast enough to justify expectations that increasingly resemble macroeconomic projections rather than normal corporate forecasts. For much of the market, Nvidia is no longer just a company. It has become the benchmark for whether the infrastructure boom still has momentum.

Victoria Bazir

Victoria Bazir