Eseandre Mordi

Eseandre Mordi

Japan's leadership is drawing a line on rate hikes, and currency markets are paying attention. The yen slipped after Prime Minister Takaichi warned that higher yields, combined with Japan's existing debt load, could cause interest expenses to surge, making a case for keeping rates structurally low even if inflation continues running hot. The remarks were flagged by Jeroen Blokland and quickly moved into broader macro discussions around USD/JPY.

Japan's Debt Math: Why 10% of GDP in Interest Costs Is on the Table

The core concern is fiscal, not just monetary. At current yield levels and debt volumes, Japan's interest costs could climb toward 10% of GDP within the next decade. That number reframes the entire rate debate: aggressive tightening would mechanically increase debt servicing, potentially forcing greater reliance on monetary support to fund government obligations. In that environment, yen weakness is not a surprise, it is a logical market response to the limits of policy normalization. Earlier analysis already pointed in this direction, with JPY tracks Japan's inflation miss as M2 money growth sits at just 1.56% showing how macro data has been quietly undermining the yen's recovery narrative.

If policymakers lean toward low rates alongside higher inflation to manage financing pressure, the Japanese yen can remain sensitive to credibility and fiscal concerns.

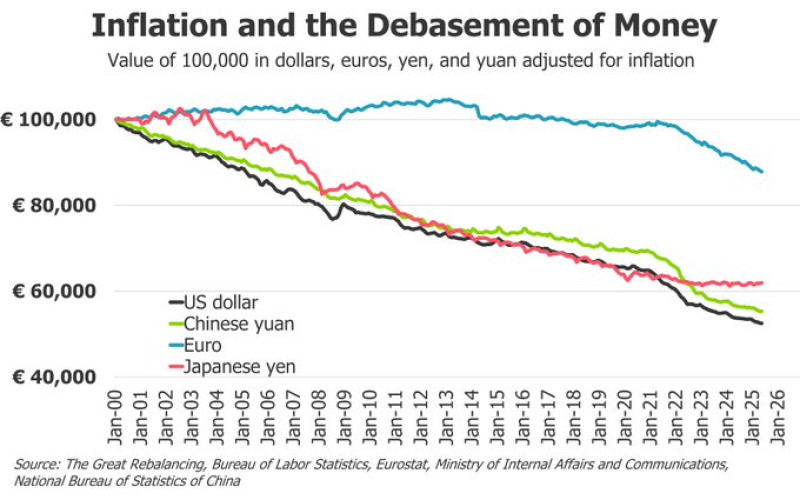

Fiat Purchasing Power and What the USD/JPY Chart Is Really Showing

Longer-term context adds another layer. A comparison of inflation-adjusted value across four major currencies, the US dollar, euro, Japanese yen, and Chinese yuan, shows all four lines trending lower over time. Purchasing power erodes across the board, but the yen and dollar show sharper declines in later years, while the euro holds relatively higher for longer. It is a reminder that this is not just a Japan story. Sustained inflation and policy choices carry real costs in any currency, and the yen is simply making those costs visible faster than most. Markets tracking the BOJ's next move have already priced in caution, as covered in USD/JPY watches BOJ March pause odds as "no change" hits 94%.

What this episode ultimately highlights is that currency performance cannot be separated from debt sustainability and confidence in monetary frameworks. As long as Tokyo's fiscal math constrains rate policy, the yen stays vulnerable. The broader picture is laid out in JPY forecast: trade-weighted index eyes new 2025 lows, where the structural pressure on the yen is tracked through its trade-weighted performance heading into the rest of 2025.

Eseandre Mordi

Eseandre Mordi