Victoria Bazir

Victoria Bazir

Wall Street is raising expectations for NVIDIA again ahead of its May 20 earnings report, but the bigger question for markets may no longer be whether AI demand is strong - it’s whether Nvidia can continue outperforming expectations at the scale investors now assume.

Wall Street Is Raising the Bar Again

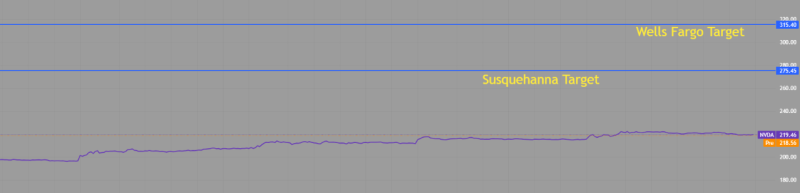

Susquehanna International Group analyst Christopher Rolland raised his Nvidia price target to $275 from $250 while maintaining a Positive rating, citing accelerating AI infrastructure spending among hyperscale cloud companies. Meanwhile, Wells Fargo lifted its target even further to $315 from $265, reinforcing Wall Street’s increasingly aggressive outlook on Nvidia’s AI dominance.

The chart shows how dramatically expectations around Nvidia have expanded ahead of earnings. Analysts are no longer projecting incremental upside — they are increasingly pricing Nvidia as the central infrastructure company powering the global AI expansion cycle.

The forecasts reflect how dramatically expectations around AI computing have expanded over the past year.

Rolland estimates Nvidia’s Blackwell and Rubin platforms could collectively generate around $1 trillion in revenue by 2027 - a figure that would place Nvidia among the most economically influential technology platforms in modern history. Demand for AI networking hardware and gaming GPUs also remains strong, suggesting Nvidia’s ecosystem advantage is expanding beyond data-center accelerators alone.

But as expectations rise, so does the difficulty of sustaining the narrative.

Nvidia Is Becoming the AI Market Itself

The second chart highlights Nvidia’s growing influence over the broader technology trade. NVDA shares have increasingly moved alongside the Nasdaq, reinforcing the idea that Nvidia is no longer behaving like a typical semiconductor stock - it is becoming one of the market’s primary AI sentiment indicators.

That dynamic creates unusually high stakes for upcoming earnings guidance.

If Nvidia delivers another major beat alongside stronger Blackwell production updates, markets could interpret it as confirmation that the AI spending boom is still accelerating. In that scenario, semiconductor stocks, AI infrastructure suppliers, and broader tech indices could extend their rally sharply higher.

However, the risks are also evolving.

Rolland warned that margins could face pressure later as Rubin launches, highlighting a growing concern across the semiconductor industry: maintaining profitability while rapidly scaling increasingly complex AI hardware systems. Nvidia also continues facing export restrictions tied to China, one of the world’s largest semiconductor markets.

The broader issue may be valuation sensitivity.

Nvidia has become one of the most important macro assets in global markets, with its earnings increasingly influencing sentiment across semiconductors, AI startups, cloud providers, and even the broader Nasdaq. That means future market reactions may depend less on whether Nvidia grows - and more on whether growth remains strong enough to justify the scale of optimism already embedded in the stock.

In many ways, Nvidia is no longer being evaluated as a chip company alone. Markets are increasingly treating it as the central infrastructure provider for the AI economy itself. The next earnings report may therefore become more than a company event - it could serve as a critical stress test for the entire AI trade.

Victoria Bazir

Victoria Bazir