Sergey Diakov

Sergey Diakov

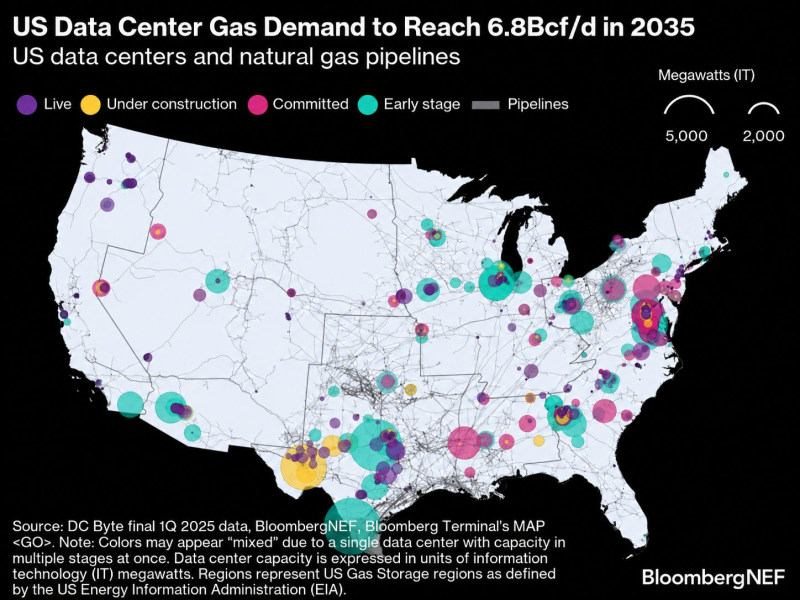

According to BloombergNEF, U.S. data centers could consume as much as 6.8 billion cubic feet of natural gas per day by 2035, reflecting the extraordinary power requirements emerging from AI infrastructure buildouts. The figure highlights a shift that is becoming increasingly difficult to ignore: the AI economy is no longer defined solely by software, models, or GPUs. It is becoming a major source of industrial energy demand.

BloombergNEF, DC Byte, Bloomberg Terminal MAP. U.S. data-center gas demand could reach 6.8 Bcf/d by 2035 as AI capacity expands across major infrastructure corridors.

The map reveals more than a concentration of data centers. It reveals a concentration of energy access. Northern Virginia remains the dominant hub, but major clusters are also emerging across Texas, the Gulf Coast, the Midwest, and parts of the Southeast. Many of the largest projects either sit directly on top of existing natural gas pipeline networks or are being developed in regions with abundant gas infrastructure.

That pattern is unlikely to be accidental. A decade ago, data-center developers prioritized fiber connectivity, tax incentives, and real estate costs. Today, access to reliable electricity increasingly determines where large AI campuses can be built. In some regions, securing power has become more challenging than securing land.

Following the Pipelines

The relationship between AI infrastructure and natural gas is becoming increasingly direct. Utilities across the United States are struggling to accommodate rapidly growing power demand from hyperscale facilities. While renewable generation continues to expand, large AI campuses require dispatchable power that can operate continuously regardless of weather conditions.

Natural gas remains one of the fastest ways to deliver that capacity. The overlap between pipeline networks and future data-center development suggests energy availability is beginning to shape the geography of AI investment. Companies are not simply choosing locations with internet access. They are choosing locations capable of supplying hundreds or even thousands of megawatts of electricity.

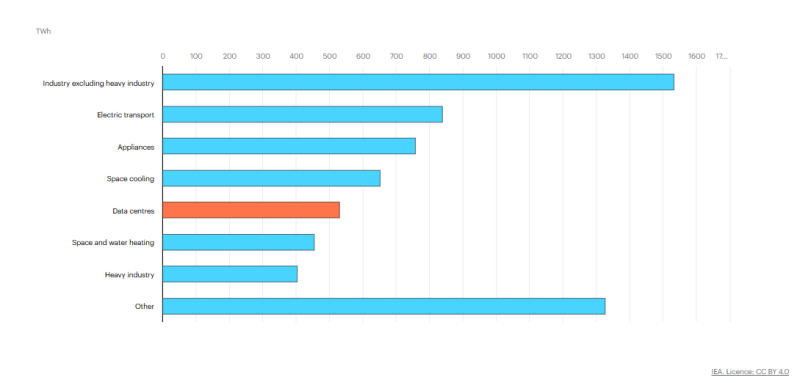

International Energy Agency (IEA). Data centres are projected to contribute roughly 520 TWh of additional electricity demand by 2030, exceeding projected growth from heavy industry (~400 TWh) and space-and-water heating (~450 TWh). Only industrial electrification (~1,530 TWh), electric transport (~840 TWh), appliances (~760 TWh), and space cooling (~650 TWh) contribute more.

The scale of that demand is often underestimated. According to the IEA, data centres are expected to add roughly 520 TWh of electricity consumption by 2030—more than heavy industry and residential heating. In other words, AI infrastructure is no longer a niche load on the grid. It is becoming one of the largest new sources of electricity demand in the global economy.

That comparison helps explain why energy has become a strategic issue for AI developers. The challenge is no longer limited to procuring GPUs or expanding cloud capacity. Every new generation of AI models ultimately translates into additional electricity demand, pulling utilities, grid operators, and energy producers into the center of the AI investment cycle.

The Bottleneck Is Moving

AI discussions revolved around chip shortages. Nvidia's GPUs, advanced packaging capacity, and HBM memory dominated conversations about supply constraints.

Those challenges remain important. But they are increasingly being joined by another question: where will the electricity come from?

Unlike semiconductor production, energy infrastructure cannot be scaled overnight. New power plants require permitting, financing, and construction. Transmission upgrades often take years. Interconnection queues continue to grow across large parts of the country. As AI campuses evolve from hundreds of megawatts to gigawatt-scale projects, electricity becomes a strategic input rather than a background utility expense.

- Projected U.S. data-centre gas demand (2035): 6.8 Bcf/d

- Additional global data-centre electricity demand (2030): ~520 TWh

- Largest U.S. data-centre hubs: Northern Virginia, Texas, Midwest, Southeast

- Key infrastructure link: Natural gas pipeline networks

- Emerging constraint: Reliable large-scale power availability

The first phase of the AI boom rewarded companies that built better models. The next phase may reward companies capable of delivering reliable power at scale.

The most important takeaway from the map is not the location of today's data centers. It is the direction of future investment. AI infrastructure is increasingly clustering around energy systems rather than technology ecosystems. The industry spent years treating compute as the scarce resource. Over the next decade, power may prove even harder to find.

Sergey Diakov

Sergey Diakov