Peter Smith

Peter Smith

Taiwan Semiconductor Manufacturing is drawing fresh attention after a wave of insider buying surfaced this week. According to analysis shared by Qualtrim, insiders picked up nearly $400,000 worth of TSMC stock within a single week - a move that stands out not because the company is struggling, but precisely because it isn't.

The timing matters. This buying activity coincides with one of the stronger stretches in TSMC's financial history, raising the obvious question: what do insiders see that the broader market might be underpricing?

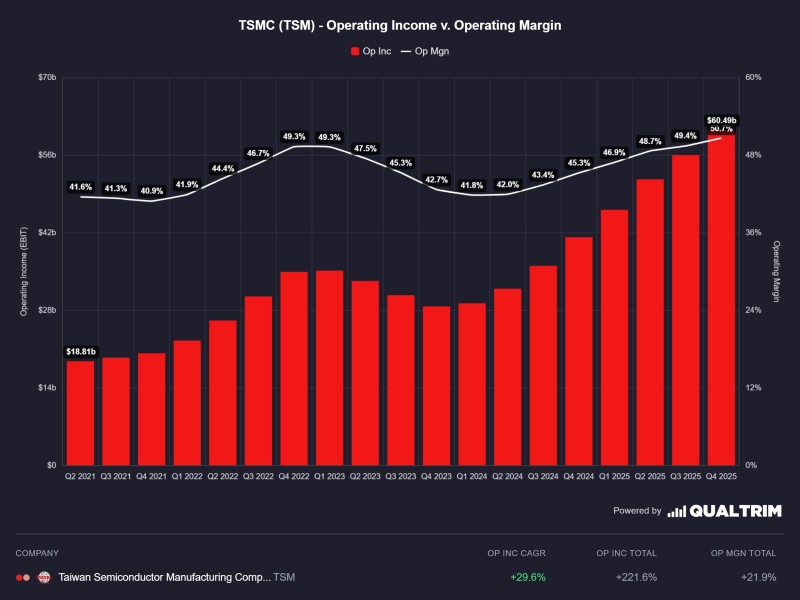

TSM Stock: Operating Income Climbs From $18.8B to Over $60B

The numbers behind TSMC's recent run are hard to ignore. Operating income has grown steadily from roughly $18.8 billion in 2021 to over $60 billion by late 2025. There was a visible soft patch through 2023 - the kind of cycle the semiconductor industry goes through periodically - but the underlying trend never broke. Growth resumed in 2024 and picked up speed heading into 2025.

This trajectory reflects something deeper than a single product cycle. TSMC's January revenue jumped 37% to $12.7B, underlining that demand for advanced chips keeps pulling the company forward regardless of macro noise.

The insider accumulation happened during a period of already strong performance - not as a bet on recovery, but as a signal of continued conviction.

TSMC Margins Recover Toward 50% as Efficiency Improves

Margins tell an equally interesting story. After peaking in the high-40% range, operating margins slipped through 2023 before clawing back and trending toward approximately 50% by 2025. That recovery pattern - dip, stabilize, then push higher - is typical of a business with genuine pricing power and operational discipline.

TSMC crushed Q4 2025 with 62.3% gross margins, confirming that profitability is not just recovering but reaching new levels. When income rises and margins expand simultaneously, it usually means growth is becoming more efficient rather than just more expensive.

Rising income alongside expanding margins points to a business that is scaling without losing its grip on profitability.

Insider Buying Aligns With TSMC's 25% Annual Growth Outlook

The insider activity becomes more interesting when viewed against TSMC's longer-term positioning. The company has projected 25% annual revenue growth through 2029, driven almost entirely by AI chip demand. That is not a speculative target - it is backed by existing customer commitments from the biggest names in AI infrastructure.

Key signals from the current data:

- Operating income reaching new highs above $60B

- Margins rebounding and trending toward 50%

- No visible deterioration in profitability fundamentals

- Insider accumulation of nearly $400,000 in a single week

TSMC projects 25% annual revenue growth through 2029 on AI chip demand - and insiders appear to be positioning accordingly, not waiting for a dip that may not arrive.

When insiders buy during strength rather than weakness, it tends to reflect a view that the current run has further to go.

For TSM stock, the picture that emerges is a company operating near peak financial performance, with internal confidence now visibly backing the uptrend.

Peter Smith

Peter Smith