Marina Lyubimova

Marina Lyubimova

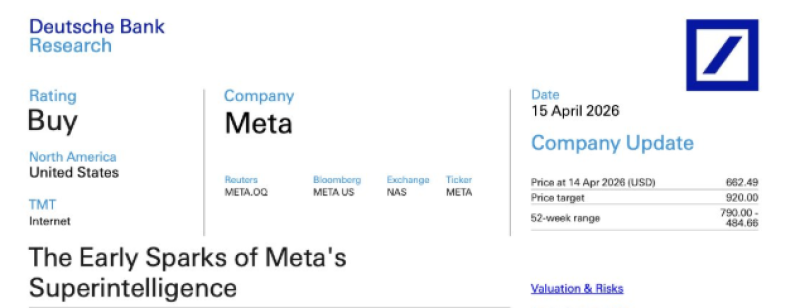

Meta Platforms is back in focus after a bullish analyst update highlighted a shift in expectations. As Damian Brik noted, Deutsche Bank reiterated a "Buy" rating on META with a $920 target - implying roughly 39% upside. The report frames this as an early-stage transition where prior investment in AI is starting to show measurable results in core business metrics.

The META Upgrade That Reframes the Narrative

The Deutsche Bank note positions Meta as moving into a new phase of its cycle. The $920 price target is tied to a valuation multiple of around 27x expected 2027 earnings, reflecting confidence in forward growth.

What stands out is the shift in focus. Instead of emphasizing cost pressures from heavy investment, the report highlights improving operating performance - signaling that the market may be underestimating the payoff from Meta's long-term AI strategy.

The shift is from cost pressure narrative to performance payoff narrative - Deutsche Bank is arguing that the market is still pricing Meta as if the AI investment hasn't started working yet, when the data suggests it has.

Meta Platforms Closes in on $1.6T Valuation with $190B Revenue Base provides the scale context for the $920 target, showing how the revenue base that supports that valuation has been building - and why a 27x 2027 earnings multiple looks more defensible against a $190 billion revenue backdrop than it would have even two years ago.

META Ad Growth Turns Higher Above Expectations

A key detail from the update is the change in advertising trends. In Q1 2026, ad spend growth reached approximately 6.0%, exceeding expectations of 5.5%. More importantly, the trajectory is pointing upward - Deutsche Bank expects ad spend growth to increase further in Q2, potentially reaching around 6.4% year over year.

This suggests a reacceleration in Meta's primary revenue engine rather than the slowdown many had anticipated heading into the year.

Ad spend growth beating at 6.0% and expected to reach 6.4% in Q2 is not stabilization - it is reacceleration, and that distinction changes how forward earnings estimates need to be modeled.

META Stock: Forward P/E Sits Near 20.5 While Twitter Thread Highlights AI Scale and Reels Growth showed what the valuation looked like when the AI thesis was still being questioned - making the current ad growth reacceleration a data-driven confirmation of what that analysis was positioning ahead of.

AI Begins to Show Through in META Results

The report attributes much of the improvement to AI-driven tools, particularly Advantage+, which are enhancing advertiser returns. As ROI improves, advertisers tend to allocate more budget - creating a feedback loop where better performance leads to increased spending that further strengthens the platform.

The note also references a broader superintelligence theme, suggesting that Meta's AI investments could drive additional monetization opportunities over time beyond the current advertising improvements.

META Stock Holds $620 Level Despite 21% Revenue Growth captured the disconnect between Meta's underlying business performance and its stock price at a lower level - a disconnect the $920 Deutsche Bank target is now arguing has become even more pronounced as AI efficiency gains begin to show up in the advertising metrics.

The key takeaway is not just the price target but the shift in narrative. Meta's growth is no longer viewed as slowing - it is stabilizing and beginning to accelerate again, supported by improving ad performance and AI efficiency gains that are starting to show up in the numbers.

Marina Lyubimova

Marina Lyubimova