Artem Voloskovets

Artem Voloskovets

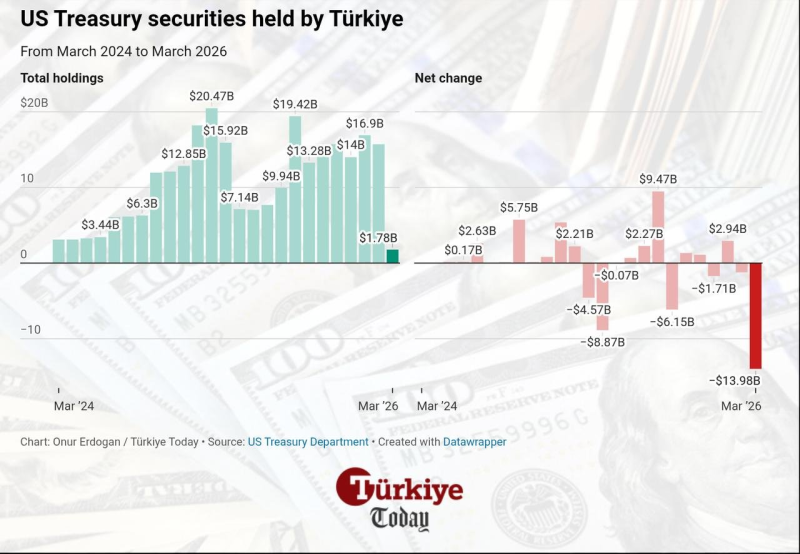

Türkiye's holdings of U.S. Treasury securities rose from roughly $2 billion in March 2024 to a peak of $20.47 billion before collapsing to just $1.78 billion by March 2026. The final move was dramatic: a $13.98 billion reduction in a single month, according to U.S. Treasury data.

U.S. Treasury Department via Türkiye Today. Turkish Treasury holdings peaked at $20.47 billion before falling to $1.78 billion in March 2026.

The selloff may look like a verdict on U.S. government debt. More likely, it reflects changing liquidity needs. The buildup occurred during a period when Türkiye was rebuilding foreign-exchange reserves and benefiting from elevated U.S. yields. Treasuries offered a liquid, dollar-denominated asset that could be accumulated quickly and sold just as easily.

The scale of the reversal suggests an operational decision rather than a gradual portfolio shift. Before the March liquidation, the country had already recorded monthly reductions of $8.87 billion and $6.15 billion.

A Liquidity Story, Not a Treasury Story

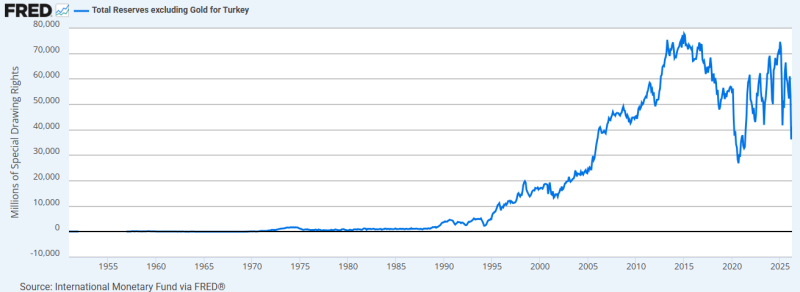

IMF via FRED. Türkiye's reserves excluding gold exceeded SDR 70 billion at their peak but have experienced significant volatility in recent years.

Reserve data provides additional context. Türkiye's foreign-exchange reserves excluding gold expanded sharply over the past two decades, eventually surpassing SDR 70 billion. More recently, however, reserves have fluctuated between roughly SDR 25 billion and SDR 70 billion, reflecting frequent adjustments in reserve management.

The timing of the Treasury liquidation is difficult to ignore. The largest monthly sale arrived after reserves had already experienced substantial swings, suggesting policymakers were prioritizing flexibility over duration exposure. For reserve managers, Treasuries are not primarily a return-generating investment. They are one of the fastest ways to access dollar liquidity without disrupting the broader reserve portfolio.

That distinction matters because it changes how Treasury flows should be interpreted. A sharp reduction in holdings does not necessarily imply a negative view on U.S. debt, Federal Reserve policy, or the dollar itself. In many cases, it simply reflects changing liquidity requirements.

The broader takeaway extends beyond Türkiye. Foreign central banks have traditionally been viewed as stable, long-term buyers of U.S. government debt. Recent flows suggest a more tactical approach. Holdings can expand during reserve accumulation cycles and contract sharply when liquidity becomes a priority.

A $14 billion sale will not move the Treasury market. What it does illustrate is how reserve management is evolving. In a world of higher rates, volatile capital flows, and recurring currency pressures, liquidity increasingly matters more than long-term positioning.

Artem Voloskovets

Artem Voloskovets