Eseandre Mordi

Eseandre Mordi

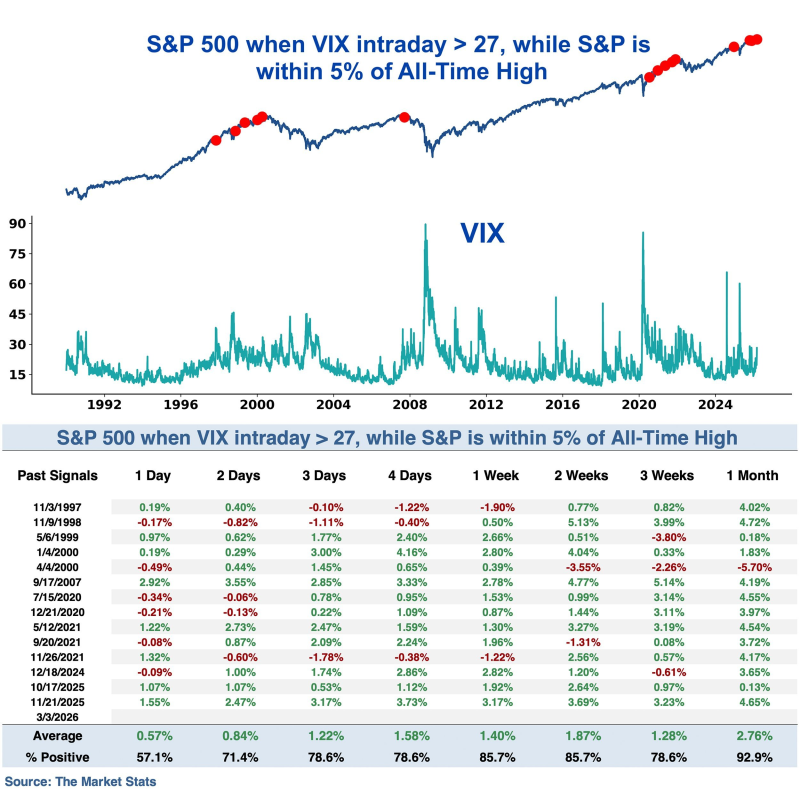

A rare market signal is back on the radar. The VIX volatility index recently spiked above 27 intraday while the S&P 500 stayed within 5% of its all-time high — an unusual combination that has only shown up a handful of times over the past few decades. Data compiled by The Market Stats makes the current setup worth watching, given how rarely these two conditions align at the same time.

Looking back at historical charts, each of these VIX spikes near record price levels is clearly marked on the long-term S&P 500 chart. What stands out is that the S&P 500 was higher one week later in 12 out of 14 instances — suggesting that volatility surges without a real price breakdown tend to be short-lived stress events rather than early warnings of a bigger selloff.

The numbers get even more compelling over a slightly longer window. The S&P 500 was higher one month later in 13 out of 14 cases, a 92.9% positive hit rate. Average returns across time frames were consistently positive: +0.57% after one day, +1.40% after one week, and +2.76% after one month. This kind of pattern points to a market where sharp spikes in fear or hedging demand reflect temporary pressure, not a lasting change in trend.

Market analysts continue to track the relationship between VIX spikes and S&P 500 performance closely. When volatility jumps without a meaningful drop in equity prices, it often signals short-term anxiety while the broader trend stays intact. Broader participation data and volatility patterns have historically gone hand in hand with ongoing strength in the index, even when temporary turbulence shows up along the way.

Eseandre Mordi

Eseandre Mordi