Saad Ullah

Saad Ullah

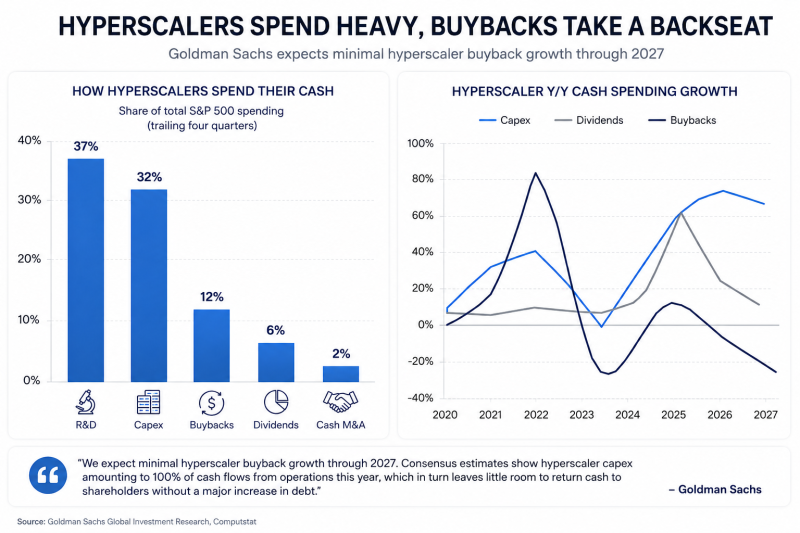

According to a Goldman Sachs note cited by Yahoo Finance’s Brian Sozzi, hyperscaler companies are on track to spend virtually all of their operating cash flow on capital expenditures this year, leaving little room for stock buybacks through at least 2027.

“We expect minimal hyperscaler buyback growth through 2027,” Goldman Sachs analysts said. “Consensus estimates show hyperscaler capex amounting to 100% of cash flows from operations this year, which in turn leaves little room to return cash to shareholders without a major increase in debt.”

A Goldman Sachs chart reinforces the scale of the shift. Over the past four quarters, hyperscalers’ spending has been heavily concentrated in R&D and capex, which accounted for 37% and 32% of total S&P 500 spending, respectively. By comparison, buybacks represented only 12%, dividends 6%, and cash M&A just 2%.

The second chart shows why buyback growth may remain under pressure. Hyperscaler capex growth has accelerated sharply and is projected to stay elevated into 2026–2027, while buyback growth has weakened after a brief rebound in 2024. Dividend growth has also started to moderate from recent highs.

The data highlights the enormous financial pressure created by the AI infrastructure race. Microsoft, Amazon, Meta, and Alphabet are pouring unprecedented amounts of money into data centers, AI chips, networking infrastructure, and cloud expansion to support generative AI products and enterprise demand.

The report suggests that Wall Street may need to reset expectations around future buyback growth, one of the key drivers behind Big Tech stock performance over the past decade. Instead of aggressively repurchasing shares, hyperscalers appear to be prioritizing infrastructure dominance and long-term AI positioning.

Saad Ullah

Saad Ullah