Marina Lyubimova

Marina Lyubimova

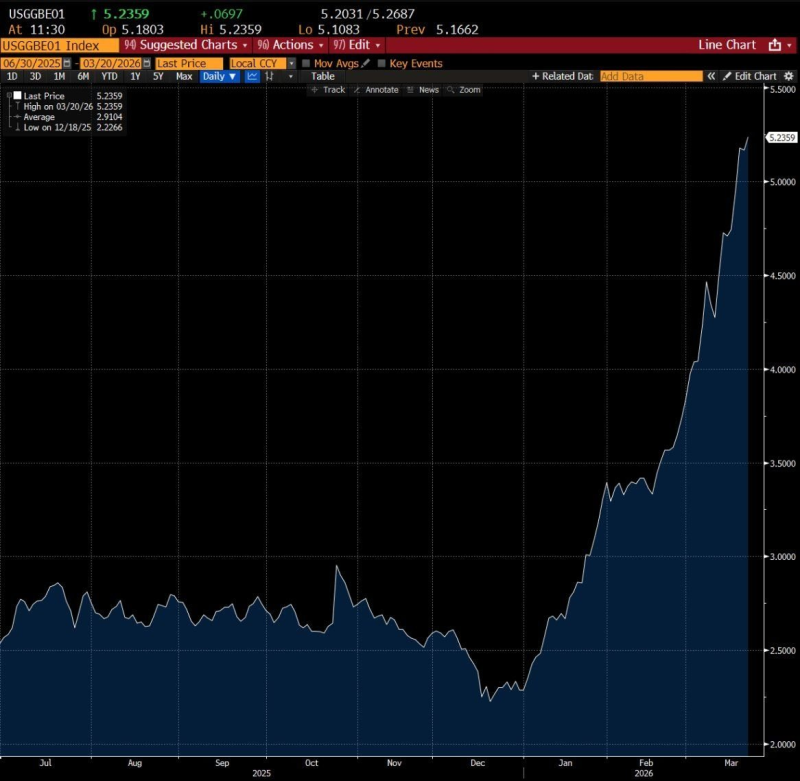

US Treasury yields have surged to around 5.23% on the 10-year note, one of the highest readings in recent years. In just three weeks, markets moved from pricing in rate cuts to factoring in potential hikes. The chart tells the story bluntly: from lows near 2.2% in late 2025 to above 5% by March 2026. That kind of repricing at that speed doesn't happen without a real shock driving it. Analysts tracking Fed rates, oil shocks, and market volatility flagged this reversal weeks before it showed up in mainstream coverage.

The trigger is energy. Oil prices are up roughly 40% since the Iran conflict began, gasoline jumped about 30% in a single month, and diesel crossed $5 per gallon for the first time since 2022. That sequence has pushed 12-month inflation expectations to 5.2%, the highest since March 2023. When energy costs move this fast, bond markets don't wait for official CPI reports. The gold price and inflation-driven market dynamics playing out right now are a direct echo of that repricing.

The Fed has responded by holding rates steady while revising its inflation projections upward. That's not a neutral move; it's a signal that cuts are off the table and the direction of travel has changed. The Fed policy shift and inflation outlook impact is already filtering into equity positioning, with rate-sensitive names under visible pressure.

The broader message from yields at 5.23% is simple: easing assumptions are gone. The trajectory in the chart suggests that as long as energy prices stay elevated, inflation expectations won't cool and the Fed won't pivot. Bond markets are not anticipating relief, they are pricing in persistence.

Marina Lyubimova

Marina Lyubimova