Sergey Diakov

Sergey Diakov

Switzerland's latest inflation data is quietly confirming one of the most consistent relationships in macroeconomics: when money supply grows at a steady, controlled pace, prices tend to follow suit. With inflation sitting at just 0.3% year-over-year and M3 expanding at 5.0%, the country finds itself precisely inside a historically balanced monetary zone. Economist Steve Hanke has been among those tracking this alignment closely, noting that Switzerland now fits the framework almost perfectly.

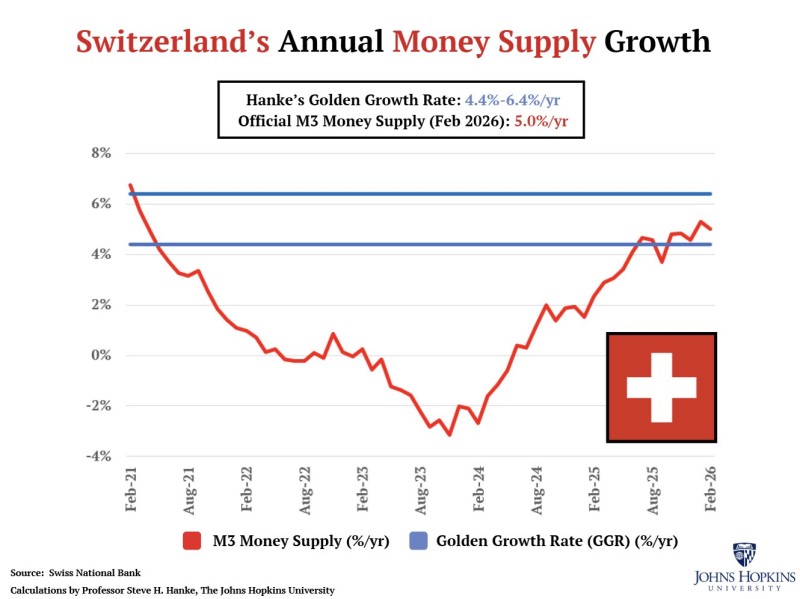

Switzerland's M3 Lands in the Golden Growth Rate Band

Switzerland's current M3 growth rate of 5.0% falls squarely within what Hanke calls the "Golden Growth Rate" - a band stretching from 4.4% to 6.4%.

This corridor has long been associated with durable price stability and maps closely onto the Swiss National Bank's official inflation target of 0%-2%.

The relationship between money supply and price stability is not theoretical here - it is directly observable in the numbers.

Inflation at 0.3% sits comfortably inside that target range, which is exactly what the monetary framework would predict when liquidity expands at a controlled, measured pace. The alignment is not coincidental - it reflects a disciplined monetary trajectory playing out in real time. For a broader read on global liquidity dynamics, see Global M1 Surges $25 Trillion Since 2020 as China Takes Over One-Third.

Switzerland's Money Supply Completes a Full Monetary Cycle

The broader picture tells the story of a full monetary cycle working itself through the system. M3 growth started above 6% in 2021, then declined steadily through 2022 and into 2023, eventually turning negative. That contraction phase reduced liquidity meaningfully across the economy.

By early 2024, the structure shifted - growth rebounded from negative levels and began forming a steady uptrend that has continued into 2026.

The recovery progressed through 2025 and into early 2026, ultimately bringing M3 back to approximately 5%. What makes this significant is not the movement itself, but where it stabilizes. The reading does not overshoot the upper boundary of 6.4%, nor does it fall below the 4.4% floor. It settles directly within the optimal corridor - the kind of precision that monetary frameworks are designed to produce but rarely deliver so cleanly. A comparable dynamic can be seen in India's Money Supply Growth Signals Inflation Under Control.

The Signal Hidden in Switzerland's Inflation Stability

What this chart does not show is equally important. There is no erratic expansion, no excessive tightening, no sharp reversals. Instead, it reflects a gradual return to equilibrium after a period of meaningful contraction. The upper and lower bounds of the Golden Growth Rate act as a clear structural framework, and Switzerland's current trajectory sits neatly between them.

Analyses across comparable economies consistently show that controlled money supply growth supports low inflation over time. Switzerland's current positioning reinforces that pattern, with liquidity conditions that are neither too loose nor too restrictive. For historical context on how Switzerland arrived at this point, see Switzerland's Money Supply Returns to Optimal Growth.

When money supply growth remains within a stable range, inflation tends to follow - and Switzerland's latest data suggests that balance has been restored.

The takeaway is both simple and powerful. The Swiss case is not a theoretical model - it is a live demonstration of monetary stability working as intended. For now, the numbers suggest that balance has been restored and, perhaps more importantly, maintained.

Sergey Diakov

Sergey Diakov