Sergey Diakov

Sergey Diakov

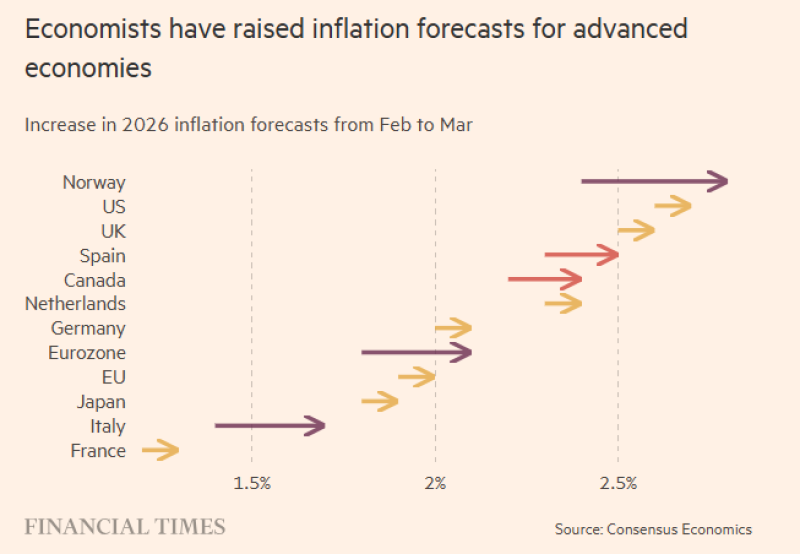

⬤ Economists are revising inflation forecasts upward across several developed economies, signaling renewed concern about stubborn price pressures. The latest projections put U.S. inflation at 2.7%, up from a prior estimate of 2.6%. The UK's forecast has moved to 2.6% from 2.5%, while the Eurozone now sits at 2.1%, revised up from 2.0%. These shifts reflect a broader reassessment of macroeconomic conditions heading into mid-2026, with U.S. Inflation Outlook: Truflation Sees Slightly Softer Data Ahead of Official CPI already flagging signs of a more persistent inflation backdrop.

⬤ Among the countries tracked, Norway holds the highest 2026 inflation projection, followed by the U.S. and the UK. Spain and Canada also show notable upward revisions. Germany, the Netherlands, and the broader Eurozone cluster near the middle of the range, while Japan, Italy, and France remain at the lower end. France carries the lowest inflation estimate of all economies presented in the March update.

Higher energy costs tend to affect transportation, manufacturing, and electricity expenses, which then feed into broader consumer prices.

⬤ A key driver behind the revisions is the recent uptick in oil and energy prices. Energy costs ripple through supply chains quickly, pushing up transport, manufacturing, and utility bills before hitting household budgets. The scale of that volatility was on full display when WTI Crude Oil Crashes 12% After Strategic Reserve Shock, illustrating how fast energy-market swings can reshape economic forecasts.

⬤ Persistent inflation matters because it directly shapes central bank decisions on interest rates and, in turn, the performance of equities, currencies, and commodities like gold. Analysts and investors track these forecast shifts closely as early indicators of monetary policy pivots. Earlier reporting on EU Inflation Holds at 2% Target in August 2025 shows how even marginal deviations from target levels draw significant market attention and portfolio reallocation.

Sergey Diakov

Sergey Diakov