Artem Voloskovets

Artem Voloskovets

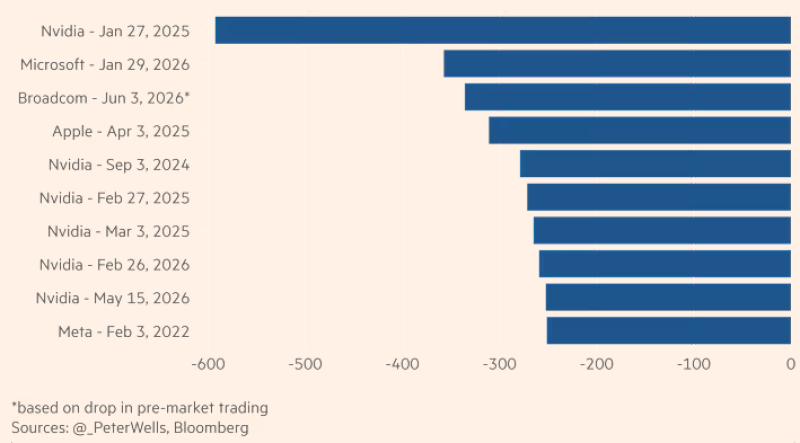

Broadcom shares fell as much as 15% during Thursday's session, one of the sharpest single-day declines among major semiconductor companies this year.

On the surface, the selloff makes little sense. Broadcom reported first-quarter revenue of $19.3 billion, up 29% year-over-year. Adjusted EBITDA margin reached 68%, management projected roughly $22 billion in second-quarter revenue, and the company authorized a new $10 billion share repurchase program.

Those are the numbers of a company benefiting from one of the strongest investment cycles in technology. Yet the stock still dropped. The explanation may be simple: the market was pricing in something even bigger.

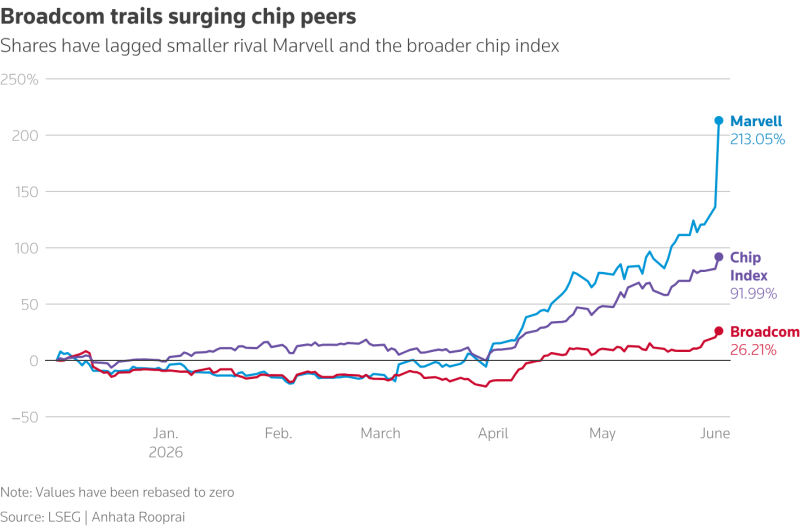

Broadcom's year-to-date performance has lagged both Marvell and the broader semiconductor sector despite its central role in AI infrastructure.

The Problem Was Never the Quarter

Broadcom's results were objectively strong. Revenue growth remained close to 30%, profitability stayed among the highest in the semiconductor industry, and management continued to point toward expanding demand from AI-related customers.

The issue is that Broadcom is no longer being judged on traditional metrics alone. Over the past two years, AI infrastructure has become one of the market's most crowded trades. Companies tied to data centers, networking, advanced chips, and cloud computing have attracted enormous amounts of capital, pushing valuations higher across the sector.

Once that happens, investors stop asking whether growth exists. They start asking whether growth is accelerating fast enough.

Marvell's Shadow Is Getting Bigger

One clue can be found in relative performance. Before the latest selloff, Broadcom shares had gained roughly 26.2% year-to-date. In most years, that would rank among the stronger performers in technology. This year looks different. The broader semiconductor index advanced nearly 92%, while Marvell surged more than 213%.

The comparison matters because markets rarely value companies in isolation. Capital constantly moves toward the stories perceived to have the strongest future upside.

Broadcom remains a major AI infrastructure supplier, but parts of the market appear increasingly focused on companies viewed as offering a steeper growth trajectory.

Why Broadcom Doesn't Fit the Typical AI Story

While Broadcom is often grouped together with other AI winners, its business model is different:

- A significant portion of revenue comes from networking infrastructure rather than AI accelerators.

- The company generates substantial cash flow from mature enterprise and software businesses.

- Growth is tied to long-term customer deployments rather than short-term demand spikes.

- Broadcom is deeply linked to data-center spending but less exposed to consumer-facing AI products.

Those characteristics create a highly profitable business. They do not necessarily create the kind of explosive narrative investors have rewarded elsewhere in the sector.

A $19 Billion Quarter Wasn't Enough

The market reaction becomes easier to understand when Broadcom's numbers are placed next to expectations.

Key Figures From Broadcom's Latest Quarter

| Metric | Latest Result | Why It Matters |

| Revenue | $19.3 billion | Demand remains strong across Broadcom's core businesses |

| Revenue Growth | +29% YoY | Far above the growth rate of most large technology companies |

| Q2 Revenue Guidance | $22 billion | Points to continued expansion |

| Adjusted EBITDA Margin | 68% | Among the strongest profitability profiles in semiconductors |

| Share Buyback Program | $10 billion | Reflects substantial cash generation |

Broadcom continues to deliver strong revenue growth and industry-leading margins despite the stock's sharp decline. Figures like these would have been enough to drive shares higher. For Broadcom, they were measured against expectations built during one of the most powerful AI rallies in market history.

What Was the Market Really Pricing In?

The selloff suggests traders were not focused on what Broadcom achieved. They were focused on what comes next.

Several questions appear to be driving sentiment:

- Can AI-related revenue accelerate beyond current levels?

- Will hyperscale cloud providers continue increasing capital expenditures at the current pace?

- Can Broadcom capture a larger share of custom AI silicon demand?

- Is networking infrastructure becoming a bigger bottleneck in the AI buildout?

- Are other companies better positioned for the next phase of AI spending?

Those questions matter because semiconductor valuations increasingly depend on future growth rather than current results. A company can deliver an excellent quarter and still face pressure if the market expected something extraordinary.

The Real Takeaway

Broadcom's quarterly report did not reveal a weakness in the business. It revealed how much optimism had already been embedded in the stock. A company growing revenue by 29%, guiding for another 47% increase, maintaining margins near 70%, and authorizing a $10 billion buyback would normally dominate the narrative. Instead, the market focused on whether those numbers were enough to justify expectations that had been building for months.

That is what Thursday's selloff was really about. The lesson extends far beyond Broadcom. In today's AI market, strong results are often treated as the starting point rather than the destination. The companies attracting the most capital are those perceived to be one step ahead of expectations.

The challenge is no longer proving that AI is driving growth. The challenge is proving that growth can continue to outpace what the market has already priced in.

Artem Voloskovets

Artem Voloskovets