Marina Lyubimova

Marina Lyubimova

The February-March selloff felt dramatic in real time. It also fits a pattern that has historically rewarded investors willing to buy into weakness.

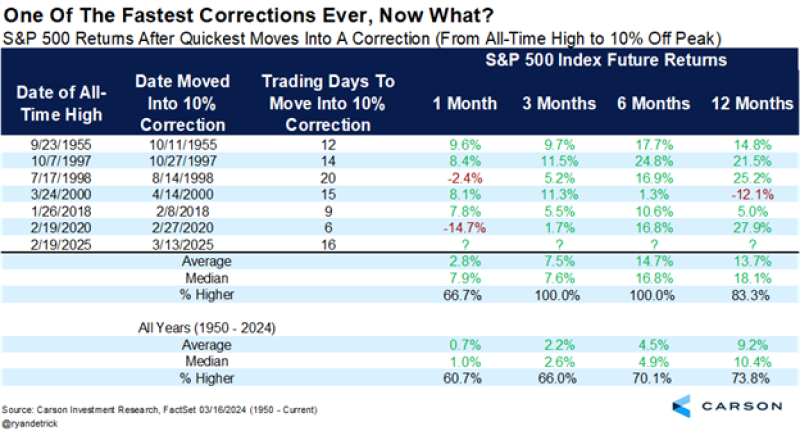

Carson Investment Research shows, there have been only a handful of occasions since 1950 when the S&P 500 fell from an all-time high into a 10% correction in less than a month. Those episodes include 1955, 1997, 1998, 2000, 2018, 2020 and now 2025.

The market's track record after those declines is difficult to ignore. Six months later, the S&P 500 delivered average gains of 14.7%. Twelve months later, the average return was 13.7%. Stocks finished higher one year later in 83.3% of cases.

Rapid corrections have historically been followed by strong forward returns. The S&P 500 finished higher 12 months later in more than four out of five cases.

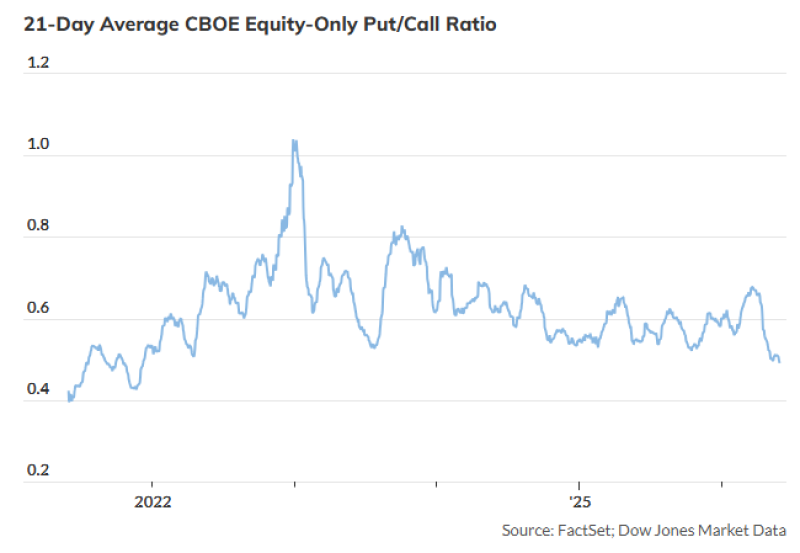

The market has largely embraced that message. Options traders certainly have. The 21-day CBOE equity-only put/call ratio has dropped below 0.50, placing it near the lower end of its range over the past several years. Investors are buying fewer puts, carrying less downside protection and showing greater willingness to position for further gains.

The 21-day put/call ratio has moved toward multi-year lows, signaling declining demand for downside hedges.

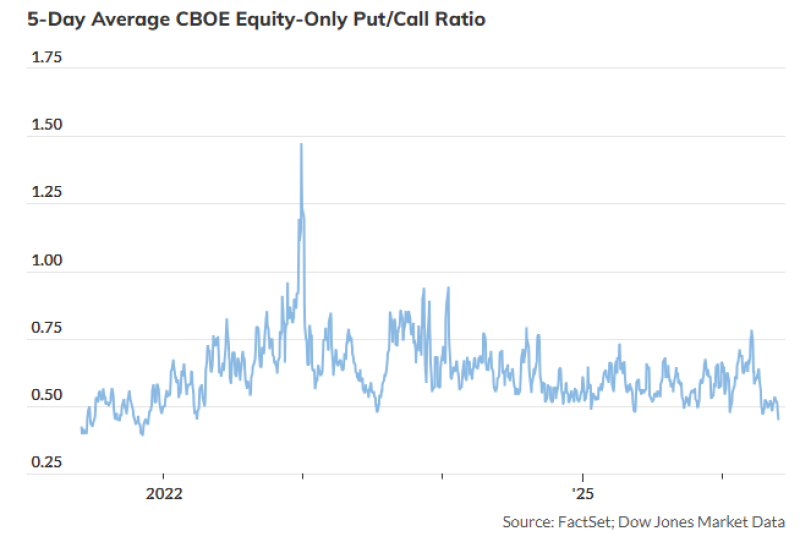

The shorter-term picture points in the same direction. The 5-day put/call ratio has fallen sharply as traders rotate back into call buying. Not because uncertainty has disappeared, but because the correction failed to produce lasting damage.

Short-term options activity shows traders increasingly favoring bullish exposure over protective positioning.

That shift matters because the rally is no longer being driven by fear. Back in March, investors were worried about slowing growth, tariffs, earnings pressure and stretched valuations. Most of those concerns still exist. What changed was the market itself.

Stocks recovered. Bullish investors could point to defensive positioning as fuel for higher prices. Underinvested funds eventually have to add exposure. Hedging positions eventually get unwound. Short sellers eventually buy back stock.

That fuel is gradually being consumed. The lower put/call ratios fall, the less future buying power remains hidden inside defensive positioning. This does not mean the rally is close to ending. The Carson data argues the opposite. Historically, rapid corrections have often marked the beginning of a new advance rather than the end of the previous one. But the backdrop is no longer the same as it was a few months ago. Three months ago, investors were paying for protection.

Today, they are paying for upside. That is usually where the market's next challenge begins. Bull markets rarely run out of buyers overnight. What changes first is the balance between caution and confidence. Earlier this year, fear created opportunities. Now optimism is becoming part of the investment case itself. The correction may already be over.

The bigger risk is that investors are starting to believe it was never much of a threat in the first place.

Marina Lyubimova

Marina Lyubimova