Victoria Bazir

Victoria Bazir

The risk facing European industry did not emerge when oil traders started pricing geopolitical uncertainty into the market. It has existed for years. The latest energy shock is simply exposing a weakness built into Europe's power system.

The sectors named by Brussels are not random. Automotive manufacturing could account for nearly half of the projected losses, with as many as 600,000 jobs at risk. Chemicals, metals, steel, batteries, transport and solar manufacturing are also on the list. The common denominator is energy intensity.

What matters is not only how much electricity Europe generates from renewable sources. What matters is what determines the price of the next megawatt-hour.

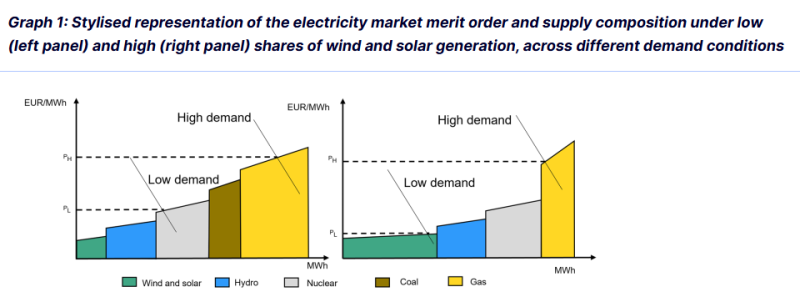

The first graph shows the pricing problem. Even when wind and solar take a larger share of supply, gas remains the marginal source during high-demand periods. In a merit-order market, that last unit of power often sets the wholesale price for everyone.

That is the uncomfortable part of Europe's transition. Renewables can expand quickly, but if gas still sets the clearing price when demand rises, industrial electricity costs remain exposed to gas shocks. Europe can look greener on the generation chart and still behave like a gas-linked power market.

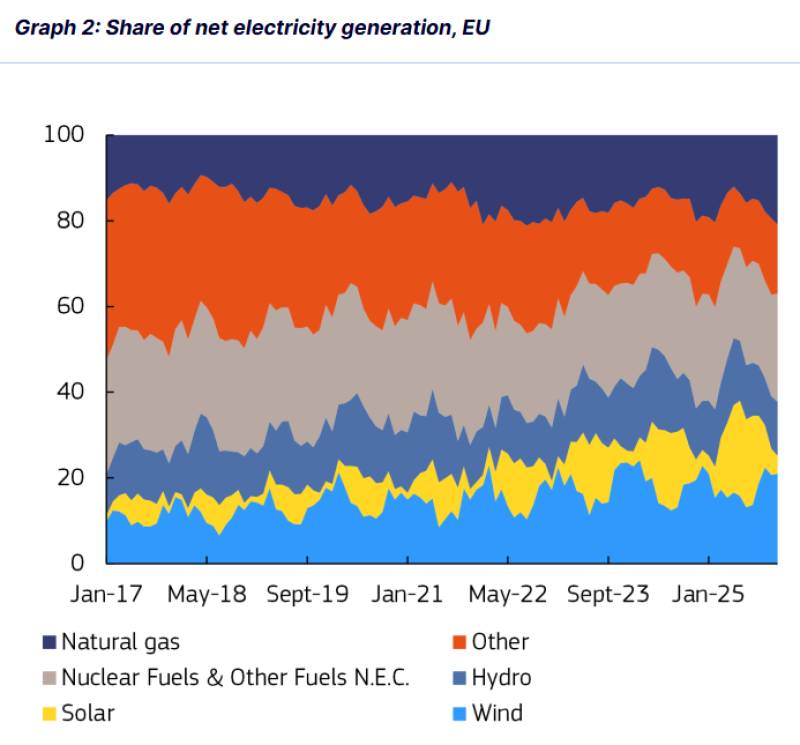

The second graph makes the contradiction visible. Since 2017, wind and solar have grown from roughly 12-15% of EU net electricity generation to around a quarter by 2025. Natural gas has moved in the opposite direction, falling from close to 40% in parts of the period to roughly 20% recently.

That is real progress. It also has limits. Gas no longer needs to dominate the generation mix to dominate the economics of electricity. It only needs to remain the balancing fuel when the system is under pressure. For a steel mill, chemical plant, battery factory or carmaker, the distinction matters. Companies do not pay for the average generation mix. They pay the market price.

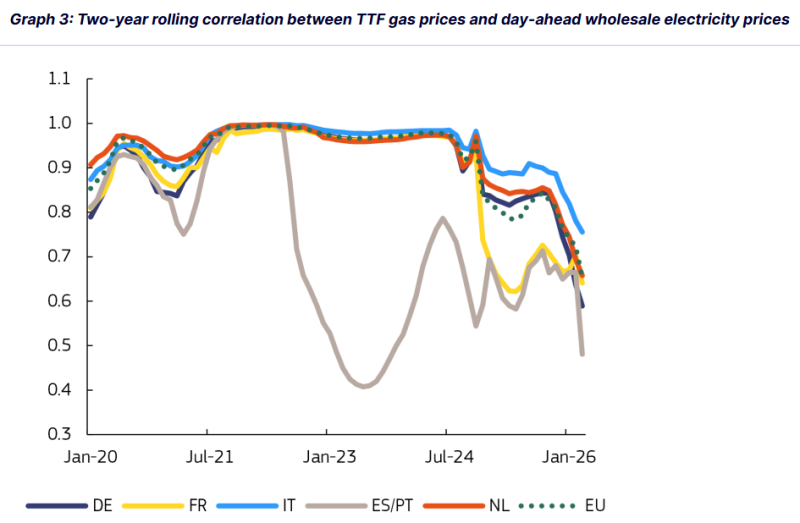

The third graph is the strongest evidence. If renewable growth had fully broken the link between gas and power markets, the correlation between TTF gas prices and wholesale electricity prices would have collapsed.

It has not. Across Germany, France, Italy, the Netherlands and the broader EU market, the two-year rolling correlation spent much of the period near 0.95-1.0. It has declined recently, but still sits around 0.65-0.80 across major markets.

That means a gas shock still behaves like an electricity shock. And an electricity shock still behaves like an industrial competitiveness shock.

This is where the jobs warning becomes more than a labor-market story. Europe has spent years trying to attract battery plants, semiconductor projects, solar manufacturing and AI infrastructure. These sectors do not just need subsidies. They need cheap, reliable and predictable electricity.

AI data centers make the problem even sharper. Training clusters and hyperscale facilities are increasingly power-location decisions. If electricity remains expensive or volatile, capital moves elsewhere.

Europe has changed where much of its electricity comes from, but not enough of what sets its price. That gap is now showing up in employment risk. It may show up next in investment flows.

The market's focus on Iran risks missing the larger issue. The vulnerability highlighted by Brussels is not primarily geopolitical. It is structural. A decade of renewable investment has reduced Europe's reliance on gas generation, but it has not fully reduced gas pricing power. Until that changes, every shock in global energy markets can still reach European factories - even in a greener grid.

Victoria Bazir

Victoria Bazir