Marina Lyubimova

Marina Lyubimova

Markets have spent months debating when the Federal Reserve will begin its next easing cycle. Far less attention has been paid to another question: how much cutting would actually be good news?

The answer is not as obvious as it seems. Conventional market thinking treats lower rates as a bullish signal. Cheaper borrowing supports spending, reduces financing costs, and can boost asset valuations. But historical market performance tells a more nuanced story.

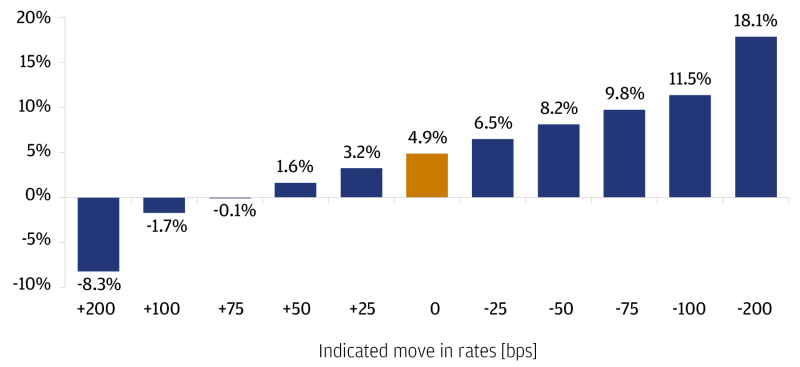

Periods associated with moderate rate cuts have generally produced positive returns for equities. Expectations of much larger cuts, however, have often appeared alongside some of the weakest stock-market environments.

Historical equity returns across different interest-rate scenarios show that moderate easing has often been associated with stronger stock performance than aggressive rate-cut expectations.

Not All Rate Cuts Mean the Same Thing

A 25- or 50-basis-point reduction usually reflects an economy that is slowing but still functioning normally. Policymakers are adjusting conditions rather than responding to a crisis.

A 100- or 200-basis-point easing cycle is different. By the time markets begin pricing moves of that magnitude, investors are usually focused on problems that extend far beyond monetary policy.

Large easing cycles are often associated with:

- Deteriorating economic growth;

- Rising unemployment;

- Stress in credit markets;

- Banking-sector instability;

- Sharp declines in corporate earnings expectations.

In these situations, the rate cut becomes a reaction to economic weakness rather than a catalyst for growth. That distinction matters. Markets are not evaluating the benefit of lower rates in isolation. They are assessing the conditions that made aggressive easing necessary.

A 200-Basis-Point Cut Is Usually Not Good News

The Global Financial Crisis remains one of the clearest examples. The Federal Reserve slashed rates aggressively, yet equities continued to fall because the central issue was not borrowing costs. Investors were confronting a financial-system breakdown, collapsing confidence, and a deep recession.

The same pattern has appeared repeatedly across major market downturns. Aggressive easing often arrives after economic conditions have already started deteriorating.

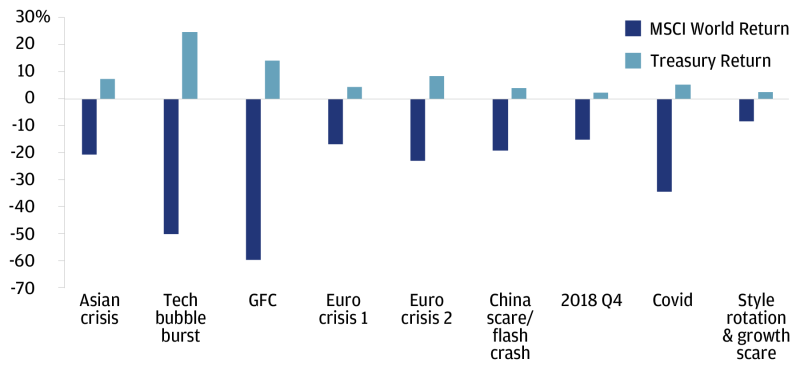

During most major market crises of the last three decades, government bonds generated positive returns while equities suffered significant losses.

This helps explain why large rate-cut expectations can coincide with weak stock-market performance. Investors are reacting to the underlying economic message rather than celebrating the policy response.

A central bank cutting rates by 25 basis points may signal confidence that inflation is easing and growth remains intact. A central bank preparing hundreds of basis points of cuts sends a very different message.

Inflation Changed the Old Playbook

For much of the last two decades, investors could rely on a simple relationship: when stocks struggled, government bonds often provided protection.

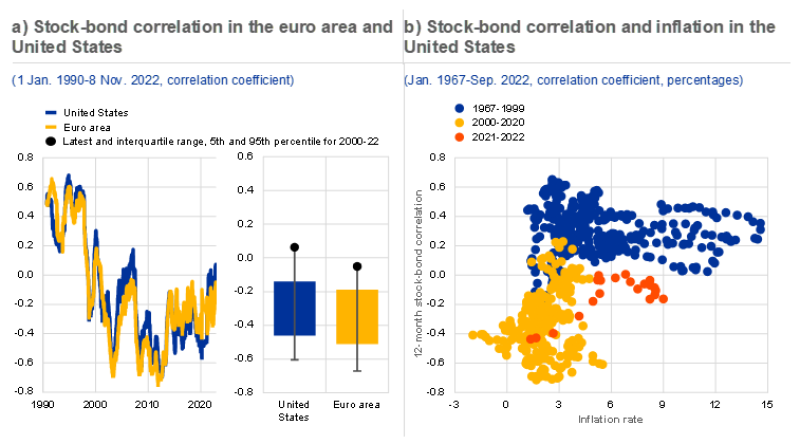

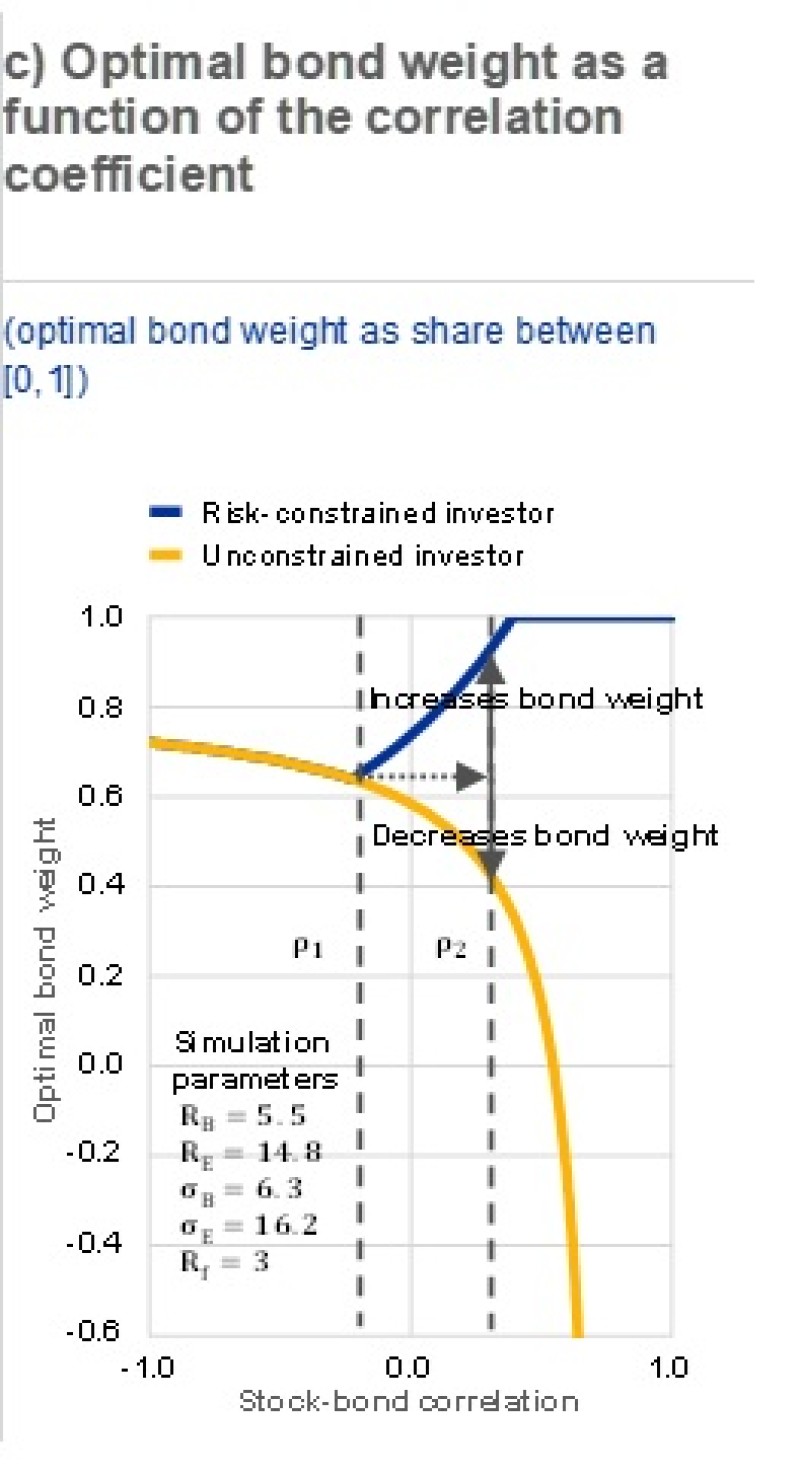

Stock-bond correlations in the United States and Europe have shifted dramatically over time, challenging assumptions behind traditional portfolio construction.

That relationship became less reliable after the inflation shock that followed the pandemic. Research from the European Central Bank shows that stock-bond correlations tend to rise as inflation moves higher. Assets that once provided diversification begin responding to the same macroeconomic forces.

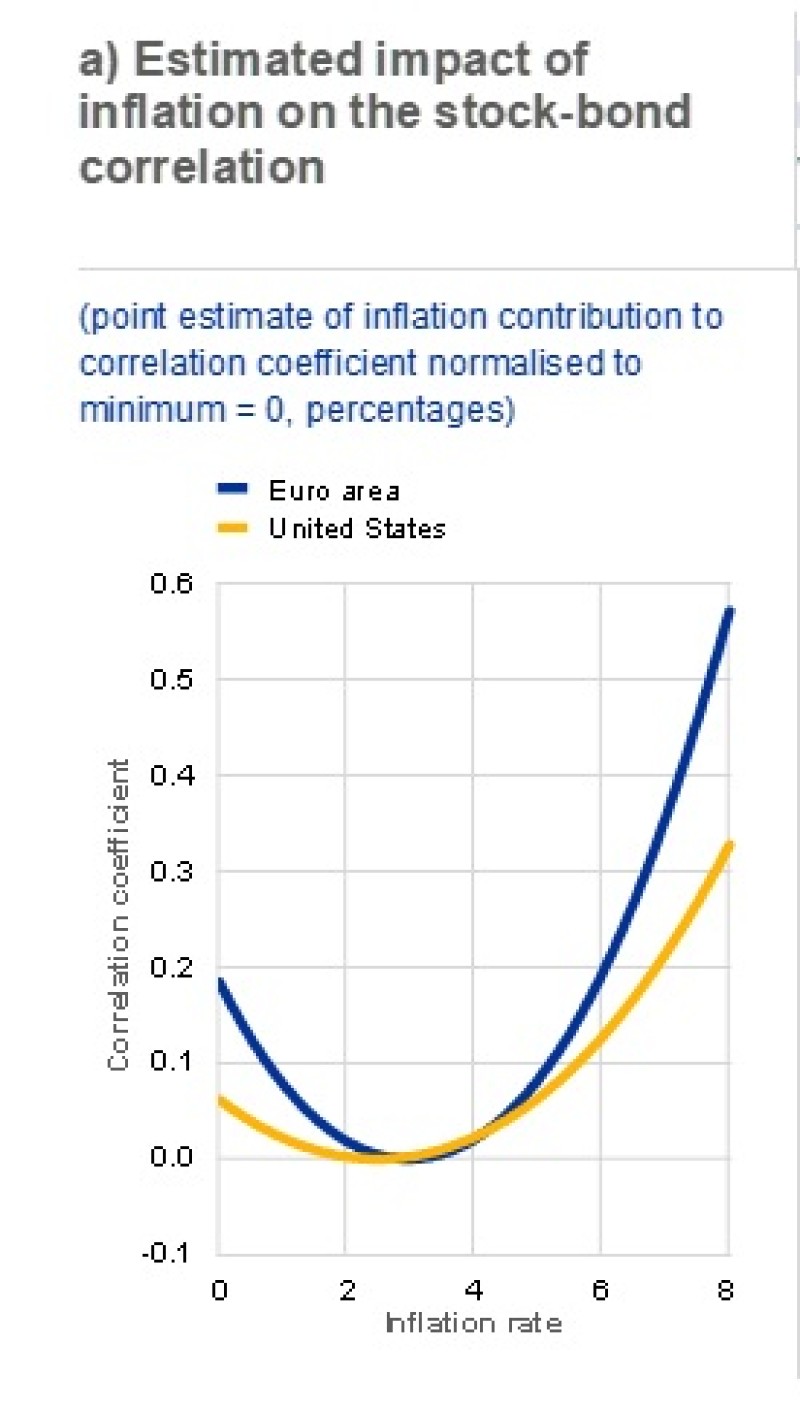

Higher inflation has historically been associated with stronger stock-bond correlations, reducing the diversification benefits of fixed-income assets.

Several structural changes have reshaped the investment landscape:

- Inflation has become a more persistent market driver;

- Government borrowing has expanded significantly;

- Fiscal policy now plays a larger role in economic growth;

- Geopolitical events influence asset prices more directly;

- Bond markets no longer offer the same diversification benefits seen during the low-inflation era.

These changes help explain why investors now scrutinize the reason behind a rate cut rather than celebrating the cut itself.

The Diversification Challenge

The classic 60/40 portfolio relied on stocks and bonds behaving differently during periods of stress. That assumption is no longer as reliable as it once was. When inflation becomes the dominant market force, both asset classes can react to the same macroeconomic shocks. The result is higher correlation and weaker diversification.

Rising stock-bond correlations can materially alter optimal portfolio allocations, according to ECB analysis.

This shift has forced investors to rethink portfolio construction. Diversification today requires more than simply mixing equities with fixed income. Understanding the drivers behind asset returns has become just as important as selecting the assets themselves.

Why Markets Care About the Reason, Not the Number

The market's reaction to monetary policy often depends less on the size of a cut and more on the circumstances surrounding it. A modest easing cycle can support risk assets when inflation is falling, labor markets remain healthy, and economic activity continues to expand.

An aggressive easing cycle often reflects a very different backdrop. Falling earnings, weakening demand, tightening credit conditions, and recession concerns can outweigh the benefits of lower borrowing costs.

That is why the largest expected rate cuts have frequently coincided with some of the weakest periods for equities. Investors are not responding to the policy tool itself. They are responding to the economic conditions that forced policymakers to use it.

A quarter-point cut can be a tailwind. A two-percentage-point rescue package is something else entirely. Markets know the difference.

Marina Lyubimova

Marina Lyubimova