Victoria Bazir

Victoria Bazir

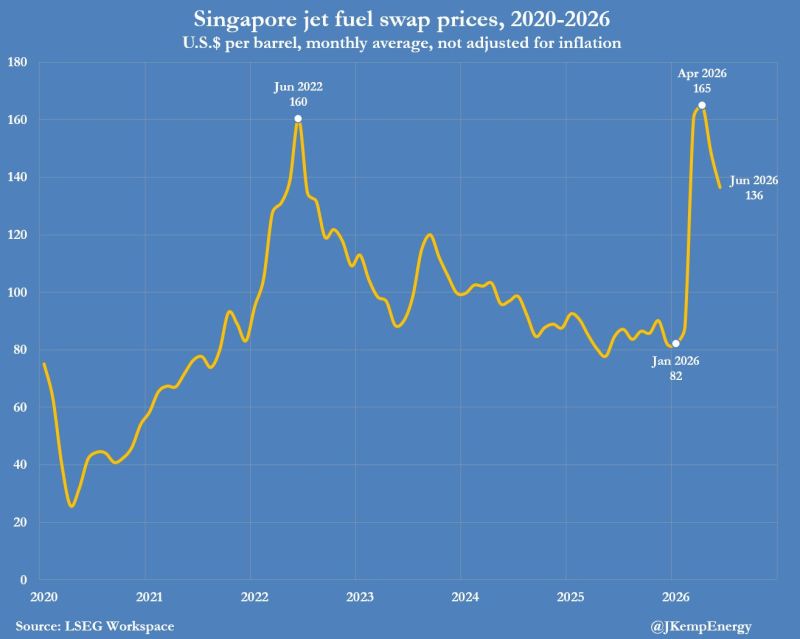

Jet fuel has become one of the fastest-moving corners of the energy market in 2026. Singapore jet fuel swap prices surged from roughly $82 per barrel in January to a peak of $165 in April before retreating toward $136 by June. At the same time, jet fuel crack spreads in North West Europe climbed above $121 per barrel, far above historical norms and nearly four times higher than levels seen before the latest Middle East disruptions.

For airlines, the move represents a sharp increase in operating costs. For investors, it offers a useful lesson: jet fuel does not always follow crude oil. Understanding why helps explain what is happening in the market today - and where risks may emerge next.

Singapore jet fuel swap prices climbed from $82 per barrel in January 2026 to a peak of $165 in April before easing to $136 by June. Despite the pullback, prices remain well above their level at the start of the year.

Start With Refining Margins

Most investors instinctively look at oil when fuel prices rise. That approach works only part of the time. Jet fuel is not a raw commodity. Before it reaches an aircraft, crude oil must be refined, stored, transported, and distributed. As a result, aviation fuel can experience shortages even when oil markets remain relatively balanced.

One reason investors are paying attention today is the behavior of crack spreads - the difference between the value of refined fuel and the cost of the crude used to produce it.

In March, jet fuel crack spreads in North West Europe exceeded $121 per barrel, compared with roughly $30 before the latest supply disruptions. The move suggests the shortage was concentrated in refined fuel rather than crude oil itself.

Three Signals That a Jet Fuel Rally Is About Refining, Not Oil

- Jet fuel prices are rising significantly faster than Brent crude.

- Crack spreads are widening sharply.

- Refining outages, export restrictions, or shipping disruptions dominate market headlines.

This distinction matters because refiners and airlines can experience very different outcomes during the same fuel rally.

Follow the Trade Flows

The latest supply shock is exposing how dependent major aviation markets remain on imported fuel. Many of the world's largest aviation hubs consume far more jet fuel than they produce domestically, leaving them vulnerable to disruptions far beyond their borders.

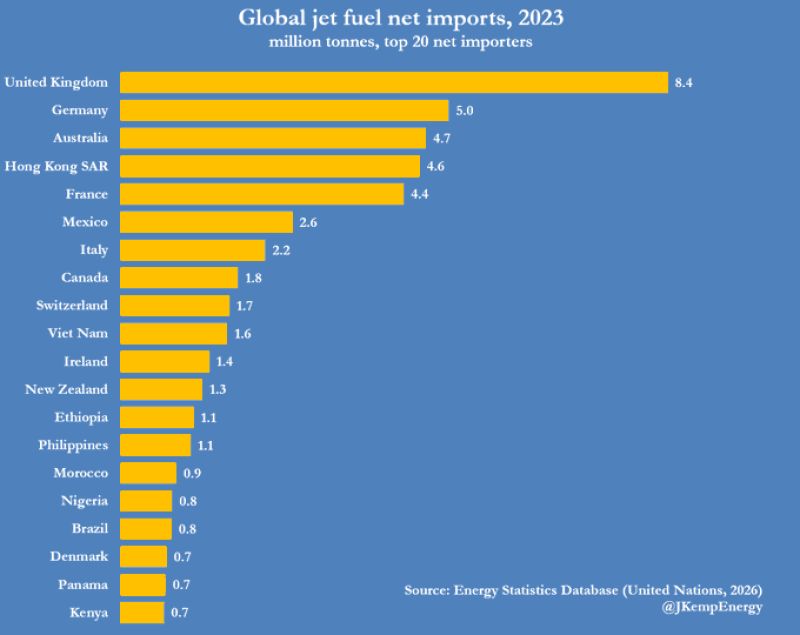

The United Kingdom imported approximately 8.4 million tonnes of jet fuel in 2023, making it the world's largest net importer. Germany followed with 5.0 million tonnes, while Australia, Hong Kong, and France imported between 4.4 and 4.7 million tonnes each.

The U.K. imported more jet fuel than any other country in 2023, highlighting how major aviation markets remain dependent on external suppliers.

The Most Import-Dependent Jet Fuel Markets

- United Kingdom — 8.4 million tonnes

- Germany — 5.0 million tonnes

- Australia — 4.7 million tonnes

- Hong Kong — 4.6 million tonnes

- France — 4.4 million tonnes

Large aviation markets often depend on imported fuel, making them vulnerable to refinery outages, shipping disruptions, and export restrictions. When supply chains tighten, fuel prices can rise sharply even if global crude production remains relatively stable.

Watch the Chokepoints

Aviation fuel relies on a limited number of refining hubs and shipping corridors. That makes the market particularly sensitive to disruptions in regions such as the Middle East, where a significant share of global jet fuel exports originates. Concerns surrounding shipments through the Strait of Hormuz have once again highlighted how quickly transportation bottlenecks can ripple through global fuel markets.

Why Aviation Is Different

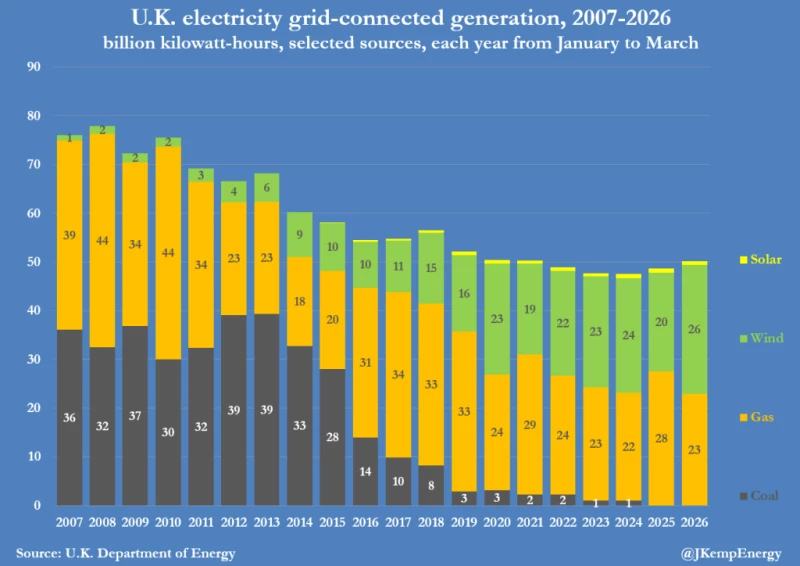

Many industries have spent the past two decades reducing their dependence on fossil fuels. The electricity sector provides a useful comparison.

In the United Kingdom, coal generated roughly 36 billion kilowatt-hours of electricity during the first quarter of 2007. By 2026, coal generation had effectively fallen to zero. Over the same period, wind generation increased from about 1 billion kilowatt-hours to roughly 26 billion kilowatt-hours.

Coal generation in the U.K. has nearly disappeared over the past two decades, while wind power has become a major source of electricity. Aviation has yet to undergo a comparable transition.

Commercial aviation still relies overwhelmingly on liquid fuels. Sustainable aviation fuel remains a small share of global consumption, while battery-powered commercial aviation is not yet a viable alternative for most routes. That leaves airlines more exposed to fuel-market volatility than many other sectors of the economy.

Four Questions to Ask During Any Jet Fuel Rally

A fuel chart becomes far more useful when viewed as a diagnostic tool rather than a price indicator.

Four Questions Investors Should Ask

- Is jet fuel rising faster than crude oil?

- Are crack spreads widening?

- Which regions depend most on imports?

- Can airlines pass higher costs to passengers?

Strong travel demand may allow carriers to raise fares. Weak demand usually means higher fuel costs translate directly into pressure on margins.

What the Market Is Really Telling You

The jump from $82 to $165 per barrel was not simply an oil story. It reflected tightening refining margins, concentrated trade flows, growing concern around critical shipping routes, and an industry that still lacks viable alternatives to liquid fuels.

Whether the latest rally proves temporary or not, it has already exposed one of aviation's enduring vulnerabilities: fuel markets can change airline economics far faster than passenger demand.

The lesson is straightforward. The next major shift in airline profitability may come not from oil itself, but from the refining and supply chains that sit between crude production and an aircraft's fuel tank.

Victoria Bazir

Victoria Bazir