Eseandre Mordi

Eseandre Mordi

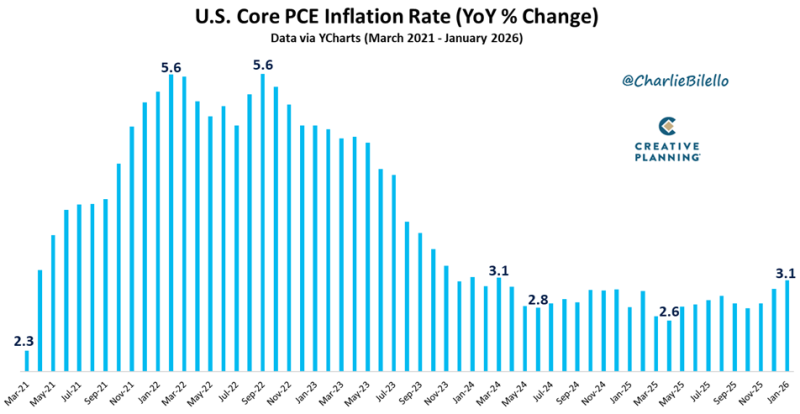

Inflation in the United States is back in focus. The Core Personal Consumption Expenditures (Core PCE) price index climbed to 3.1% year over year in January 2026, its highest level in 22 months. As the Federal Reserve's preferred inflation measure, Core PCE sits at the center of U.S. monetary policy decisions and the latest print makes clear that the path back to 2% is far from smooth.

59 Consecutive Months Above the Fed's 2% Target

The January reading extends a streak that has now lasted nearly five years. U.S. Core PCE has remained above the Fed's 2% target for 59 consecutive months, a stretch that began during the post-pandemic inflation surge when the measure peaked at roughly 5.6% in 2022. That run underscores just how stubborn underlying price pressures have proven to be, even as headline figures moderated through 2023 and into 2024.

Inflation Stalls, Rate Cut Hopes Fade

The renewed uptick is significant because it complicates the Fed's timeline. Inflation has held above the Fed target as both CPI and PCE remain flat rather than continuing to decline. With price pressures still embedded in service categories and shelter costs, policymakers have little room to pivot toward cuts anytime soon. Markets have been quick to adjust rate-cut expectations in response, and broader financial conditions are feeling the weight.

After falling toward roughly 2.6% during 2025, the measure moved higher again to 3.1%, suggesting the earlier disinflation trend may have stalled.

The bond market is already pricing in a more cautious Fed. U.S. 10-Year Treasury yields hit a yearly low earlier this cycle as rate cut expectations grew, but persistent Core PCE readings like January's 3.1% print are pushing that narrative back. Until inflation moves convincingly toward the 2% target, the Federal Reserve is likely to stay on hold, keeping borrowing costs elevated and leaving rate-sensitive sectors under pressure.

Eseandre Mordi

Eseandre Mordi