Marina Lyubimova

Marina Lyubimova

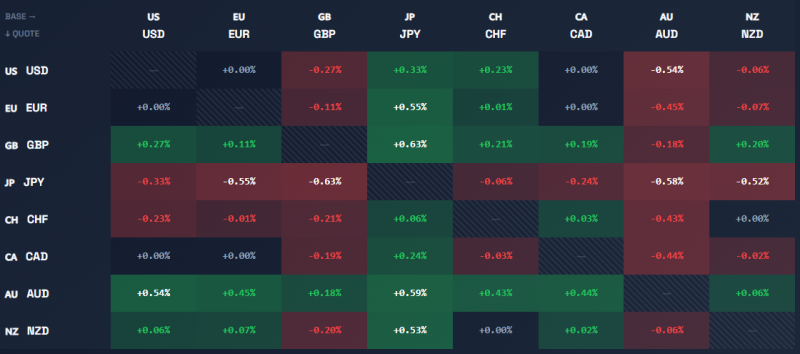

Most major FX pairs were relatively quiet today. The real story unfolded away from the U.S. dollar. The Australian dollar led gains across the currency market, rising 0.54% against USD, 0.45% against EUR, 0.44% against CAD, and 0.43% against CHF. At the same time, the Japanese yen ranked as the weakest major currency, falling against every peer in the heatmap.

The strongest moves were concentrated in yen crosses. GBP/JPY gained 0.63%, AUD/JPY rose 0.59%, EUR/JPY advanced 0.55%, and NZD/JPY added 0.53%. Even against the U.S. dollar, the yen lost 0.33%.

The breadth of the move is significant. Rather than reacting to a single economic release or central bank headline, traders were selling JPY across the board while accumulating higher-beta currencies such as AUD and NZD. That pattern is typically associated with improving risk sentiment and greater demand for growth-linked assets.

Price action confirms the shift. AUD/JPY has climbed to approximately 113.4, extending a rally that began after the pair rebounded from its April lows near 86. Since then, AUD/JPY has gained more than 30%, making it one of the strongest trends among major currency crosses.

The latest advance has pushed the pair above previous swing highs and into fresh multi-month territory. Momentum remains firmly positive, with buyers continuing to support the trend despite periodic pullbacks.

AUD/JPY is closely watched because it combines two currencies that often sit on opposite sides of the risk spectrum. The Australian dollar tends to benefit from stronger commodity demand, expanding global trade, and improving economic expectations. The yen, by contrast, is widely used as a defensive currency during periods of uncertainty and market stress.

Today's heatmap suggests investors are favoring the former over the latter. Notably, the U.S. dollar was not the primary driver of the move. Several major dollar pairs remained close to unchanged, indicating that traders were repositioning within the broader FX market rather than making a directional bet on Federal Reserve policy.

Marina Lyubimova

Marina Lyubimova