Marina Lyubimova

Marina Lyubimova

For most of its existence, XRP has been discussed as a banking asset. But the next phase of digital payments may have less to do with banks or retail users and more to do with machines interacting autonomously. As APIs, AI agents, and automated systems begin exchanging value directly, the infrastructure requirements of payments start to change. That shift could create a very different role for XRP than the market originally expected.

The Narrative Around XRP May Be Pointing in the Wrong Direction

For years, XRP has been trapped inside the same conversation: banks, cross-border payments, SWIFT, regulation, ETFs.

Even now, most discussions around the asset assume the end user looks something like a financial institution or a retail trader. A human at a terminal. A treasury desk. A payment company moving money between countries. But software infrastructure is changing faster than crypto narratives do. And that creates a strange possibility: XRP’s next meaningful user may not be a person at all.

It may be an API.

APIs Are Starting to Behave Like Economic Actors

The idea sounds abstract until you look at how payments are evolving inside AI systems and automated services. APIs are no longer passive bridges between apps. Increasingly, they behave more like autonomous economic participants - requesting compute, accessing paid datasets, triggering workflows, purchasing inference, and coordinating between platforms without human approval at every step.

That changes the definition of a payment network.

Traditional financial rails were built around human behavior: banking hours, settlement windows, fraud checks, card authorization, regional compliance layers. Machine-driven systems prioritize something else entirely - uptime, predictable execution, low latency, and cost efficiency at scale. A payment rail for software agents does not need branding or consumer UX.

It only needs reliability.

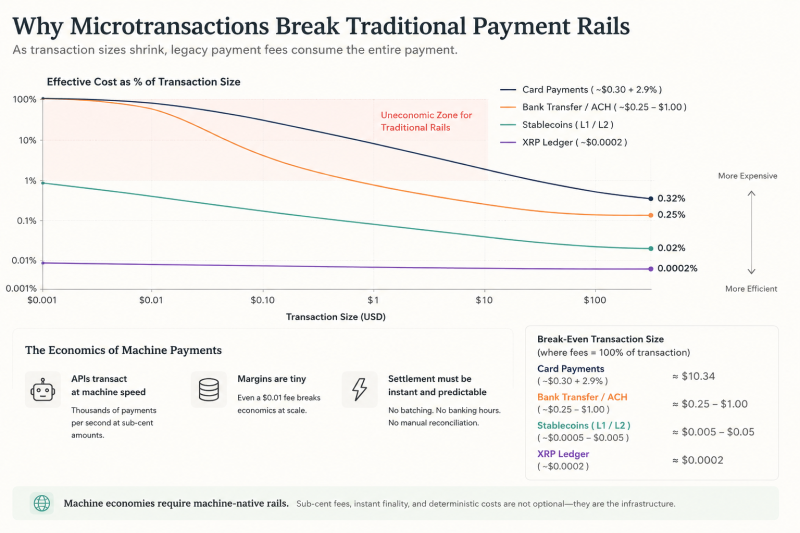

Microtransactions Break Traditional Rails

Use:

Why Microtransactions Break Traditional Payment Rails.

Directly below:

A payment rail for software agents does not need branding or consumer UX.

The Economics of Machine Payments Look Completely Different

The problem is not just transaction speed. It is transaction structure.

Card networks were never designed for APIs making thousands of tiny requests per hour. Bank transfers become inefficient at small sizes. Even stablecoins, despite their advantages, still inherit a model largely optimized for dollar-denominated settlement rather than continuous machine interaction.

That creates a growing mismatch between how humans pay and how systems may eventually transact.

| Payment System | Structural Limitation |

| Card networks | Fees become irrational for tiny payments |

| Bank transfers | Slow operational windows |

| Stablecoins | Mostly tied to fiat liquidity models |

| Traditional banking | Human approval and reconciliation layers |

This is where XRP becomes more interesting than its public narrative suggests.

Not because it is “the future of banking” a phrase that has aged poorly, but because XRP was originally optimized for movement rather than scarcity. Its architecture prioritizes settlement speed, low transaction cost, and predictable execution. Those characteristics matter more in automated systems than they do in speculative retail markets.

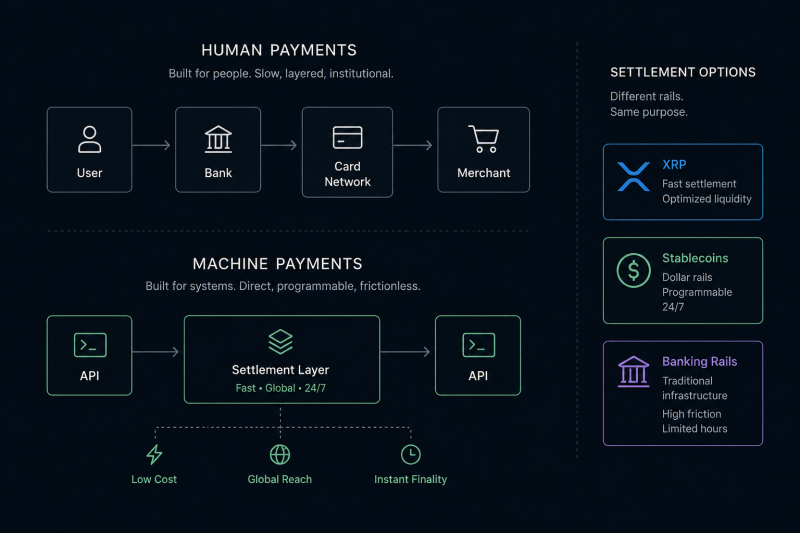

Human Payments vs Machine Payments

Use:

Human Payments vs Machine Payments Settlement Diagram.

Directly after:

Its architecture prioritizes settlement speed, low transaction cost, and predictable execution.

XRP Starts Looking Less Like a Consumer Asset

That distinction becomes more important once APIs begin interacting financially with one another.

An AI agent purchasing model access. A cloud system paying for bandwidth in real time. A marketplace charging per request. These are no longer science-fiction scenarios. Parts of the infrastructure already exist. What remains unresolved is the settlement layer underneath it. The market may eventually care less about which asset stores value best and more about which network handles machine-native value transfer most efficiently.

That is a very different competition.

| System | Weakness in Machine Economies |

| Bitcoin | Inefficient for high-frequency transactional logic |

| Ethereum | Unpredictable transaction costs |

| Card rails | Poor economics for microtransactions |

| Banking systems | Operational friction and limited hours |

In that environment, XRP stops looking like a “bank coin” and starts resembling infrastructure - closer to a routing layer than a consumer-facing asset. Invisible systems tend to scale quietly. TCP/IP became massive precisely because users stopped noticing it. Most people using the internet have no idea how packets move underneath their applications.

Financial rails may evolve the same way.

The Strange Outcome

Ironically, this could happen without retail adoption ever arriving in the form crypto investors once imagined. No global XRP super-app. No mass-market banking revolution. No dramatic consumer payments narrative. Just APIs transacting in the background because the economics make sense.

That possibility also explains why the market still struggles to price XRP coherently. Most valuation frameworks around crypto remain tied to scarcity narratives or retail adoption curves. Infrastructure assets behave differently. Their utility emerges from integration density, not cultural dominance.

And if that shift happens, the next major XRP user probably will not open a wallet, watch price prediction videos, or post on crypto social media.

It will simply send a request to another machine.

Marina Lyubimova

Marina Lyubimova